Financial Operations

Mastering Private Equity Due Diligence: Your Guide

Navigate private equity due diligence with confidence. Our guide covers key financial, legal, & operational checks + a checklist to boost valuation.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··20 min readPrivate equity deals are getting bigger, more expensive, and less forgiving. McKinsey’s Global Private Equity Report 2026 says total buyout and growth deal values increased 17%, while large deals above $500 million reached over $1 trillion, up 44%, and median purchase multiples rose from 11.3x EBITDA in 2024 to 11.8x in 2025 (McKinsey). That matters to you even if your company is far smaller.

Higher multiples don’t make diligence easier. They make buyers harsher. When assets get expensive, investors stop taking management numbers at face value. They test every assumption, every policy, every contract, and every operational weakness. If your reporting is loose, they won’t “work through it later.” They’ll cut price, add escrows, or walk.

For founders in the $500K to $20M revenue range, that’s the core issue. Most lower middle-market businesses don’t lose value because the company is bad. They lose value because the company is hard to underwrite. Messy revenue recognition, weak backlog reporting, customer concentration you can’t explain, contracts scattered across inboxes, and a close process that depends on one overworked bookkeeper. That’s what drags valuation down.

Private equity due diligence is not a paperwork exercise. It’s a stress test on whether your business is believable.

Practical rule: If a buyer has to discover your story for you, you’ve already lost leverage.

That’s why seller-side preparation matters. If you get investor-ready before the letter of intent, you don’t just survive diligence. You shape it. You control the narrative, defend EBITDA, reduce surprises, and give buyers fewer excuses to retrade.

The High-Stakes Reality of a Private Equity Deal

A 1.0x turn on EBITDA changes price fast. On a business with $2 million of EBITDA, that swing is $2 million. On a business with $5 million of EBITDA, it is $5 million. That is why diligence gets brutal when buyers are paying full prices.

Private equity firms do not forgive messy reporting in a strong market. They punish it. The higher the multiple, the more expensive every weak assumption becomes. A revenue cutoff issue, a shaky add-back, or inconsistent deferred revenue treatment can turn into a six- or seven-figure valuation hit once the buyer applies the deal multiple.

Founders usually underestimate how early this starts. Buyers begin underwriting as soon as they see your materials. They compare the teaser to the deck, the deck to the financials, and the financials to the contracts and bank activity. According to Deloitte's overview of financial due diligence, buyers typically examine historical earnings, cash flow, working capital, debt-like items, and the assumptions behind forecasts. That review reaches well beyond whether the books technically close.

Being 80 percent ready is still a problem.

If your monthly numbers do not tie to the general ledger, if bookings and revenue are mixed together, or if one employee is carrying the entire close process in their head, buyers read that as execution risk. SaaS and service firms get hit especially hard because the story depends on clean cohort data, deferred revenue schedules, utilization, backlog, and contract terms. If those pieces are loose, your growth story loses credibility.

The fallout is predictable:

- Purchase price drops: buyers reduce EBITDA for unsupported revenue, margin distortions, or owner add-backs that do not hold up.

- Deal terms get heavier: escrow, holdbacks, and working capital protections increase.

- Credibility erodes: once answers change twice, buyers widen the scope and trust management less.

- Time kills momentum: extra requests drag the process out, and slow deals give buyers more chances to retrade.

The job here is to prove quality. Growth helps, but quality gets the deal done.

You need clean revenue recognition, signed contracts that match billing, support for every adjustment, and reporting that survives scrutiny without a heroic cleanup effort. That is exactly why seller-side preparation should start before outreach, not after the LOI.

For SaaS and service businesses, an outsourced controller can move this from theory to execution. A good one cleans up the close, reconciles deferred revenue, standardizes KPI reporting, documents policies, and gets the data room in shape before buyers show up. That work does more than reduce stress. It shortens diligence, protects EBITDA, and gives buyers fewer reasons to cut price.

Buyers pay more for a business they can underwrite quickly and trust easily.

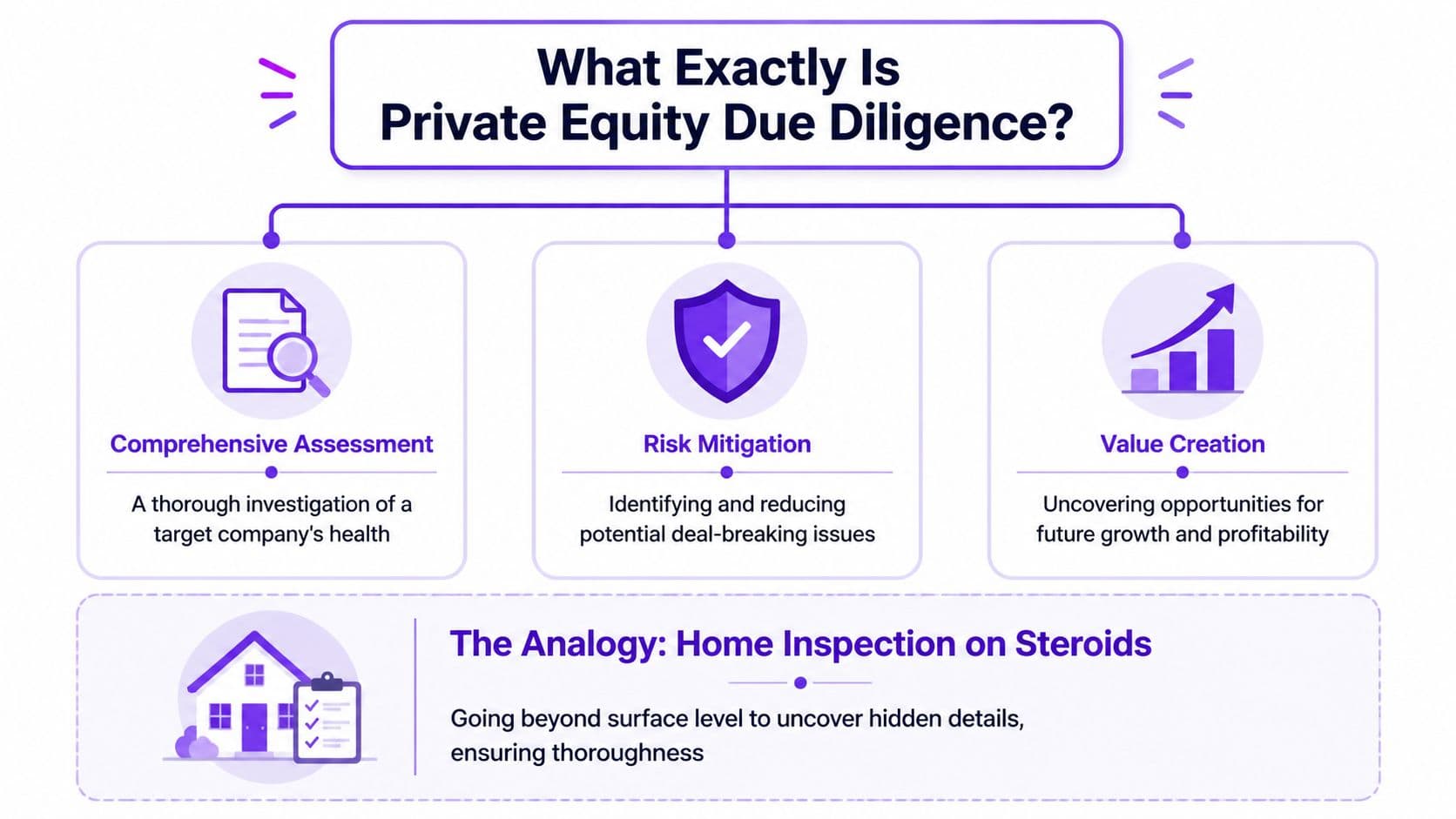

What Exactly Is Private Equity Due Diligence

Private equity due diligence answers one question: should this buyer pay your price for this business, on these terms, with confidence that the upside is real?

It is an investment underwriting process, not a box-checking exercise. Buyers test whether revenue holds up, margins convert to cash, customer relationships last, contracts support the economics, and the business can grow without constant founder intervention. If any one of those breaks, value comes down fast.

An audit looks backward at whether the numbers were presented under accounting rules for a defined period. Due diligence looks forward and asks whether the business can produce the earnings, cash flow, and growth the buyer is underwriting.

That difference matters.

A buyer is not reviewing your company in neat departments. They are pressure-testing an investment thesis. For a SaaS company, that thesis may depend on retention, expansion, deferred revenue accuracy, and clean ARR reporting. For a services firm, it usually comes down to utilization, concentration, contract economics, and whether delivery quality survives scale.

Here are the questions buyers are really trying to answer:

- Are earnings durable? They strip out one-time wins, weak cutoff practices, aggressive revenue treatment, and add-backs that do not survive scrutiny.

- Are customers and contracts worth what management says? Concentration, renewals, termination rights, pricing terms, and billing mechanics all matter. Founders who need help with mastering contract workflows should fix that before diligence starts.

- Can the business scale without breaking? Buyers look for repeatable processes, management depth, and reporting they can trust monthly, not just at year-end.

- What can hurt value after closing? Tax exposure, compliance gaps, data security issues, employment problems, and weak internal controls all show up here.

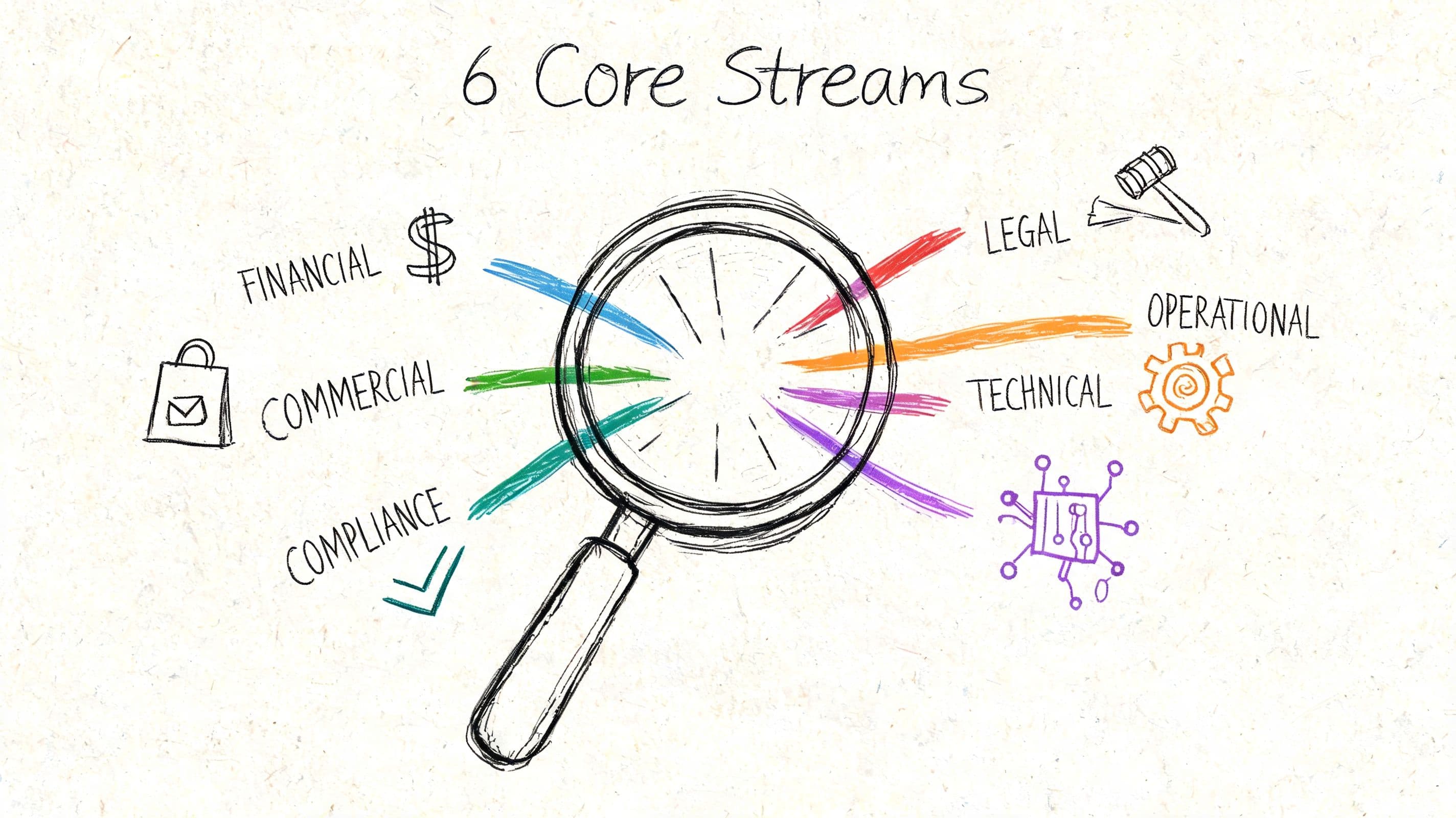

For sellers, the practical way to think about diligence is six streams:

| Stream | What the buyer wants to learn |

|---|---|

| Financial | Whether EBITDA, revenue quality, cash flow, and working capital are credible |

| Commercial | Whether the market, customer base, and positioning support growth |

| Legal | Whether contracts, IP, compliance, and corporate records hold up |

| Operational | Whether delivery, staffing, and internal processes can support scale |

| IT | Whether systems, security, and reporting infrastructure are dependable |

| Tax | Whether filings, structure, and exposures are clean |

These streams connect fast. A legal issue in customer contracts can reduce recognized revenue. Weak project tracking can distort margins. Poor payroll setup can become a tax problem. Buyers follow those links immediately.

That is why seller preparation has to start in finance operations, not in the data room. Clean monthly closes, reconciled balance sheet accounts, documented policies, and KPI reporting that ties to the general ledger make the whole process easier to underwrite. If your back office is still patched together, fix it early with stronger financial operations management systems and controls.

For SaaS and service firms, an outsourced controller often gives you the fastest path to readiness. A good one gets deferred revenue schedules right, cleans up revenue recognition, standardizes reporting, reconciles backlog or unbilleds, and documents how the business runs. That work does not just help you survive diligence. It helps you defend EBITDA, shorten buyer questions, and protect valuation.

A Deep Dive into the 6 Core Diligence Streams

Six workstreams decide whether a buyer keeps confidence in your story or starts cutting price. In practice, they do not sit in separate boxes. A miss in one area usually spills into two others, and that is how a clean deal gets expensive.

Buyers have seen every version of “we’ll clean it up after LOI.” They assume the opposite. If reporting is messy, contracts are scattered, or tax filings need explaining, they mark down value and widen the working capital peg.

Financial diligence

Financial diligence sets the tone for the whole process. Buyers test revenue quality, margin consistency, cash conversion, working capital behavior, backlog, deferred revenue, bad debt, and whether your forecast has any relationship to actual results.

For SaaS, expect scrutiny on ASC 606, deferred revenue roll-forwards, bookings versus billings, and whether ARR ties back to the general ledger. For service firms, expect questions on utilization, project margins, unbilled receivables, write-offs, and cutoff accuracy at month-end.

Here is the standard founders should hold themselves to. If your board deck says $8.4 million ARR and the ledger supports $7.9 million, you do not have a metric problem. You have a credibility problem.

An outsourced controller earns their keep for sellers. They clean up revenue recognition, tighten the monthly close, reconcile KPIs to the books, and document the logic behind the numbers. If your finance stack is still stitched together, fix it early with better financial operations management practices.

Commercial diligence

Commercial diligence answers one blunt question. Will this company keep growing after the founder steps back and a buyer takes over?

Buyers look at customer concentration, retention, pricing power, pipeline quality, win rates, market position, and the underlying reason customers buy from you. “We have loyal clients” is not evidence. Show renewal patterns, expansion history, customer cohorts, average contract value trends, and where gross retention ultimately lands when you strip out one-off noise.

For SaaS, weak net revenue retention gets punished fast. For service firms, low visibility into booked work and thin account-level margins do the same.

Legal diligence

Legal diligence checks whether the rights behind the revenue are real and transferable. Buyers review your cap table, corporate records, IP ownership, employment agreements, contractor arrangements, customer contracts, vendor terms, and any pending disputes.

Small legal messes create large deal problems. An unsigned MSA, missing invention assignment, or change-of-control clause can hold up closing over a contract worth less than 5 percent of revenue. That sounds irrational until you remember what the buyer is asking: can this cash flow survive ownership change?

Contract organization is usually the fastest fix. If your agreements live across inboxes, shared drives, and half-signed PDFs, tighten the process now. This guide to mastering contract workflows is a practical starting point because version control and approval discipline are two things buyers inspect immediately.

Operational diligence

Operational diligence tests whether the business runs on repeatable process or founder heroics. Buyers want to know how work gets delivered, how quality is maintained, where bottlenecks sit, and which people the model depends on.

In service firms, the usual pressure points are founder-led delivery, weak capacity planning, poor project accounting, and account management that exists mostly in someone’s head. In SaaS, buyers focus on implementation, onboarding, support load, product release discipline, and whether growth adds margin or drags it down.

If one delivery leader manages 40 percent of revenue personally, that is not a strength. It is concentration risk wearing an operations badge.

IT diligence

IT diligence checks whether your systems can support reporting, security, and scale without constant manual repair. Buyers review your ERP, CRM, billing platform, integrations, access controls, backups, incident response, and the reliability of the data flowing through each system.

Spreadsheet-driven reporting is a red flag because it creates avoidable errors and slows every buyer request. If billing data, customer data, and general ledger balances do not reconcile cleanly, the issue stops being “just IT” and becomes a financial diligence fight.

SaaS sellers also get hard questions on permissions, security policies, and how customer data is handled. Service firms get pressed on time tracking, project systems, and the handoff between operations and accounting.

Tax diligence

Tax diligence is where old shortcuts get exposed. Buyers review federal, state, local, and international filings, nexus issues, sales tax or VAT treatment, payroll tax compliance, contractor classification, and legal entity structure.

This stream can turn into real dollars fast. A company that missed sales tax registration in several states, or treated long-term contractors like employees for years, can end up defending liabilities that directly reduce proceeds. Founders often miss this because the P&L still looks fine. Buyers do not.

The smart move is simple. Fix what you can before diligence starts, document what you cannot, and make sure your controller can explain every open item in plain English. That is how sellers keep momentum and protect valuation.

The Quality of Earnings Report Explained

If you remember one document in private equity due diligence, make it the Quality of Earnings report, usually called the QoE. This is the document that tries to determine the true recurring earnings power of your business.

A QoE is not a standard audit. It doesn’t stop at whether the statements were prepared correctly. It asks whether the reported EBITDA is durable, normalized, and useful for valuation.

What the QoE is really doing

Alexander Group notes that financial due diligence often dissects 3 to 5 years of statements to validate projections and uncover discrepancies that could erode EBITDA by 10% to 30% (Alexander Group). That’s why the QoE matters so much. It strips out noise.

The QoE usually adjusts for things like:

- Owner-specific expenses: personal travel, discretionary spending, above-market compensation

- One-time items: legal settlements, unusual recruiting costs, nonrecurring software implementation

- Accounting cleanup: revenue cutoff errors, accrual issues, missed liabilities

- Non-core activity: revenue or costs that won’t continue after the transaction

A worked EBITDA normalization example

Here’s a simple example using real arithmetic.

| Item | Amount |

|---|---|

| Reported EBITDA | $2,000,000 |

| Add back one-time legal expense | $75,000 |

| Add back nonrecurring systems migration cost | $50,000 |

| Deduct under-accrued payroll liability | ($60,000) |

| Deduct revenue recognized too early | ($40,000) |

| Adjusted EBITDA | $2,025,000 |

That $25,000 improvement looks small until valuation gets applied.

If the buyer values your company at 11.8x EBITDA, which was the median purchase multiple cited by McKinsey for 2025 in the report referenced earlier, then:

- Reported value = $2,000,000 × 11.8 = $23,600,000

- Adjusted value = $2,025,000 × 11.8 = $23,895,000

That difference is $295,000.

Same business. Same buyer. Better earnings normalization.

Now flip the direction. If the QoE finds overstatement instead of support, valuation moves against you just as fast.

The QoE doesn’t create value out of thin air. It proves which value is real.

If your source files are messy, this work gets slower and riskier. Teams often waste time pulling tables out of bank statements, contract PDFs, and board materials. Tools built around Mintline’s approach to PDF table extraction can speed up raw data collection, but they don’t replace accounting judgment. The judgment is the whole game.

For a deeper look at how seller-side prep affects this process, review this guide on quality of earnings preparation.

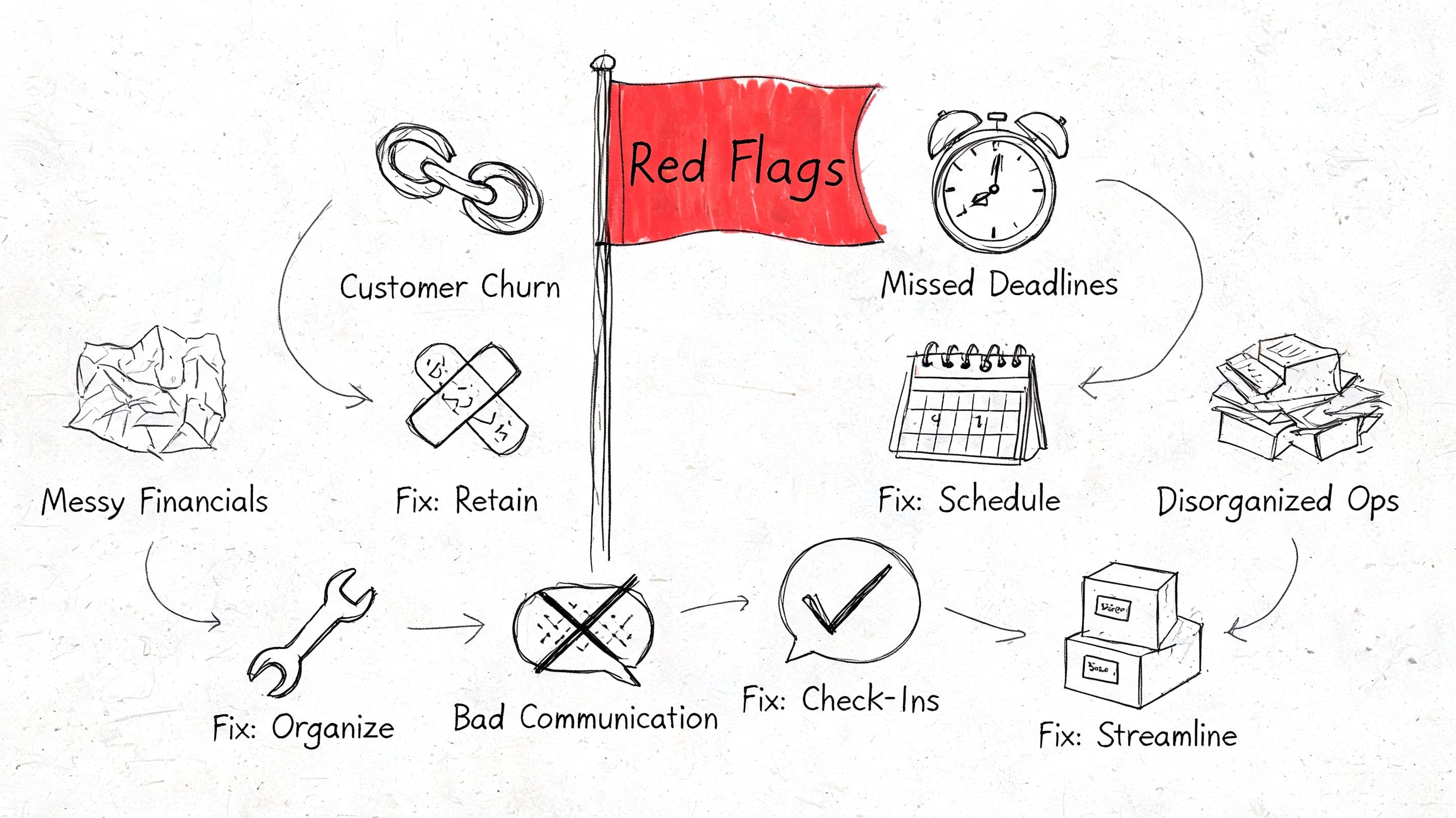

Common Red Flags That Kill Deals and How to Fix Them

Most deals don’t blow up because of one dramatic scandal. They die from a pile of smaller issues that tell the buyer your business is harder to own than it looked.

Accenture’s 2025 findings, as summarized by E78 Partners, say a majority of PE leaders view high-quality diligence as a value driver through tech-enabled market, operational, and people alignment. The same summary flags unchallenged theses and weak ESG scrutiny as common pitfalls (E78 Partners). That’s the broader pattern. Good diligence isn’t just defensive. It exposes where your story is thin.

Five red flags buyers hammer

| Red flag | Why buyers care | What to do now |

|---|---|---|

| Messy financials | They can’t trust EBITDA or working capital | Reconcile monthly, lock close checklists, document policies |

| Customer concentration | One account can blow up the thesis | Build an account diversification plan and show pipeline quality |

| Revenue recognition errors | Reported growth may not be real | Clean up ASC 606 or project-based recognition before outreach |

| Weak contract management | Revenue and legal claims become harder to verify | Centralize signed agreements and track amendments |

| Tech debt and weak controls | Scaling risk rises after close | Map systems, permissions, backups, and reporting dependencies |

The fixes need to be operational, not verbal

Founders love to explain away problems. Buyers don’t buy explanations. They buy evidence.

If customer concentration is high, don’t say “we’re working on diversification.” Show the top accounts, renewal dates, margin by client, active pipeline, and how sales capacity is changing mix over time.

If the books are messy, don’t promise a cleanup. Finish it. A buyer will always prefer a business with documented close procedures over a business with a compelling apology.

Here’s a useful primer if your accounting base needs work before diligence starts: QuickBooks cleanup services for investor-ready books.

A short walkthrough helps make these issues concrete:

One misconception that hurts founders

A lot of founders think red flags only matter if they’re fatal. That’s wrong. Most red flags don’t kill the deal outright. They just weaken your negotiating position.

Advisor view: A fixable issue discovered early becomes a discussion point. The same issue discovered late becomes a price cut.

That’s why pre-diligence work pays. You’re not trying to look perfect. You’re trying to look governable.

Your Seller-Ready Checklist and Data Room Index

A serious buyer expects a clean virtual data room, not a scavenger hunt. If your files are complete, organized, and consistent, diligence speeds up. If they’re fragmented, every request spawns three more.

Use the structure below as your baseline. If you want a more detailed financial prep list, this financial due diligence checklist is a solid companion.

Seller-Ready Virtual Data Room VDR Index

| Folder Name | Description | Key Documents |

|---|---|---|

| Corporate Governance | Legal existence and authority to transact | Certificate of incorporation, bylaws or operating agreement, board consents, cap table, equity grants |

| Historical Financials | Core financial record for diligence | Monthly financial statements, annual statements, trial balances, general ledger, chart of accounts |

| Revenue and Customers | Support for revenue quality and concentration analysis | Customer list, signed contracts, amendments, pricing schedules, renewal dates, churn analysis, backlog |

| Accounting Policies | Evidence that reporting is consistent and defensible | Revenue recognition memo, close checklist, capitalization policy, bad debt policy, expense policies |

| Forecast and KPI Reporting | Forward-looking operating picture | Budget, forecast, board deck, ARR or MRR reports, utilization reports, pipeline reports |

| Working Capital | Short-term balance sheet support | AR aging, AP aging, deferred revenue roll-forward, accrued liabilities, inventory reports if applicable |

| Tax | Filing history and exposure review | Federal and state returns, sales tax filings, payroll tax filings, nexus analysis, correspondence with authorities |

| Legal Contracts | Risk transfer and obligations | Vendor contracts, partner agreements, leases, loan documents, insurance policies, settlement agreements |

| People and HR | Team structure and employment obligations | Org chart, employee census, offer letters, contractor agreements, bonus plans, handbook |

| Product and IP | Ownership and defensibility of core assets | Trademark filings, patent filings, copyright assignments, software ownership docs, open-source policy |

| IT and Security | Systems integrity and resilience | System architecture, software list, admin access map, backup policy, incident log, security policies |

| Compliance and ESG | Regulated areas and governance discipline | Permits, privacy policies, compliance training records, customer security questionnaires, ESG policies if relevant |

What a clean room signals to buyers

A good data room tells the buyer three things fast:

- You know your numbers

- You run a disciplined operation

- You won’t become chaos after closing

That signal matters. Discerning buyers read organization as management quality.

The standard most founders should aim for

Don’t upload everything you’ve ever had. Curate it. Every file should be current, named consistently, and traceable to your reported numbers or legal obligations.

Use plain file names. Keep final signed versions separate from drafts. Include read-me notes where context matters, especially for unusual accounting treatments, customer disputes, or contract exceptions.

If you do this before the first buyer deep dive, you’ll save time, avoid confusion, and keep momentum where it belongs, on price and terms.

How to Accelerate Your Deal Readiness

Most founders don’t need more advice. They need capacity.

Preparing for private equity due diligence is a project on top of your day job. You still have to sell, deliver, hire, and manage cash while someone asks for three years of reconciled financials, contract support, tax records, KPI logic, and explanations for every variance. That’s why diligence prep stalls. Not because leaders don’t care, but because nobody owns the work full time.

What actually speeds this up

The fastest path is usually operational discipline, not fancier software.

Focus on these moves first:

- Shorten your close: monthly reporting needs to land fast and consistently

- Clean historical periods: if prior months don’t tie, future reports won’t be trusted

- Document accounting policy: especially revenue recognition, accruals, and owner adjustments

- Build KPI reconciliation: your board deck and your general ledger need to agree

- Pre-build the financial data room: don’t wait for the buyer request list

If your internal team can do that well, great. If not, bring in outside help before the process starts.

Where an outsourced controller fits

For SaaS, agencies, and services firms in the lower middle market, an outsourced controller is often the cleanest answer. The role bridges bookkeeping, finance leadership, and diligence execution.

The point isn’t outsourcing for its own sake. The point is removing friction before buyers see it.

You don’t win diligence by working harder during the deal. You win by fixing the business before the buyer starts asking questions.

If you’re even thinking about a transaction in the next planning cycle, start now. Get the books clean. Lock your policies. Build the room. Reconcile the KPIs. Then talk to buyers from a position of control.

If you want a practical outside view on how prepared your business really is, Jumpstart Partners can help you assess your financial readiness, clean up reporting issues, and organize the materials buyers will ask for. For founders planning a raise, recap, or exit, that’s often the difference between a smooth process and a painful retrade.