Financial Operations

Purpose of 1099 Form: Your 2026 Compliance Guide

Discover the true purpose of 1099 form in 2026. Master 1099-NEC, MISC, & K compliance to protect your business from costly penalties.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··18 min readThe purpose of a 1099 form is to create an IRS information trail for non-employee income so the government can verify that contractors and other recipients report what they were paid. Just as important for you, proper 1099 compliance helps protect your business from expensive worker misclassification penalties and shows that your finance operation is under control.

Most founders treat 1099s like a January paperwork nuisance. That's a mistake. If you're running a SaaS company, agency, or professional services firm in the $500K to $20M range, your 1099 process tells investors, auditors, and tax authorities whether you know who you're paying, why you're paying them, and how clean your books are.

The surprising part is how small the triggering amounts are. Service payments hit the reporting threshold at $600, while some other 1099 categories trigger at $10. That means the purpose of the 1099 form isn't just documenting big contractor relationships. It's building a reliable compliance trail across routine payments that many growing companies ignore until year-end.

Table of Contents

- Why the 1099 Form Is a Litmus Test for Your Financial Operations

- Understanding the Core Purpose of the 1099 Information Return

- Navigating the 1099 Alphabet Soup NEC MISC K and More

- A Step-by-Step 1099 Filing Checklist for Founders

- Deadlines Penalties and Costly 1099 Mistakes to Avoid

- Automate Your 1099 Compliance and Refocus on Growth

Why the 1099 Form Is a Litmus Test for Your Financial Operations

Founders often assume 1099s are just for freelancers. They aren't. A sloppy 1099 process tells the IRS that your payables controls are weak, your vendor records are incomplete, and your worker classification decisions may not hold up under scrutiny.

That matters because 1099 compliance isn't isolated. It sits at the intersection of accounts payable, contractor onboarding, legal documentation, and tax reporting. If one piece is wrong, the rest of your finance stack is usually wrong too.

The sharpest way to think about it is this: a missed 1099 is rarely a one-off clerical error. It's usually evidence that nobody owns the payment workflow end to end.

Why founders should care before tax season

When your company hires freelance developers, paid media contractors, implementation consultants, fractional execs, or outsourced creatives, you're creating a classification record whether you mean to or not. Filing the right 1099 on time helps document that the relationship was treated as non-employee compensation in your books and tax filings.

If you skip it, you lose a key piece of audit defense. You're also inviting questions that spread beyond one form. Auditors and diligence teams don't stop at "why wasn't this 1099 filed?" They ask whether the vendor was really a contractor, whether payroll was understated, and whether expenses were coded correctly.

Practical rule: If you rely on contractors to scale delivery, the purpose of the 1099 form is operational control as much as tax compliance.

This is why strong teams treat 1099s as part of finance infrastructure, not admin cleanup. If your monthly close is clean but your vendor master file is messy, your controls aren't clean. That's also why maturing companies usually tighten this process alongside broader financial operations management.

What a weak 1099 process usually signals

A weak process usually shows up in familiar ways:

- Missing onboarding documents: You paid the contractor before collecting a W-9.

- Bad vendor coding: Contractors sit in the ledger as generic software, consulting, or marketing expenses with no tax treatment review.

- No annual aggregation: You look at invoice size instead of total annual payments per payee.

- Founder dependency: One person "just knows" who should get a form, which means the system breaks when they're busy.

Clean 1099 handling tells the market something useful about your company. It says your team can support diligence, survive an audit, and scale vendor relationships without losing control of the books.

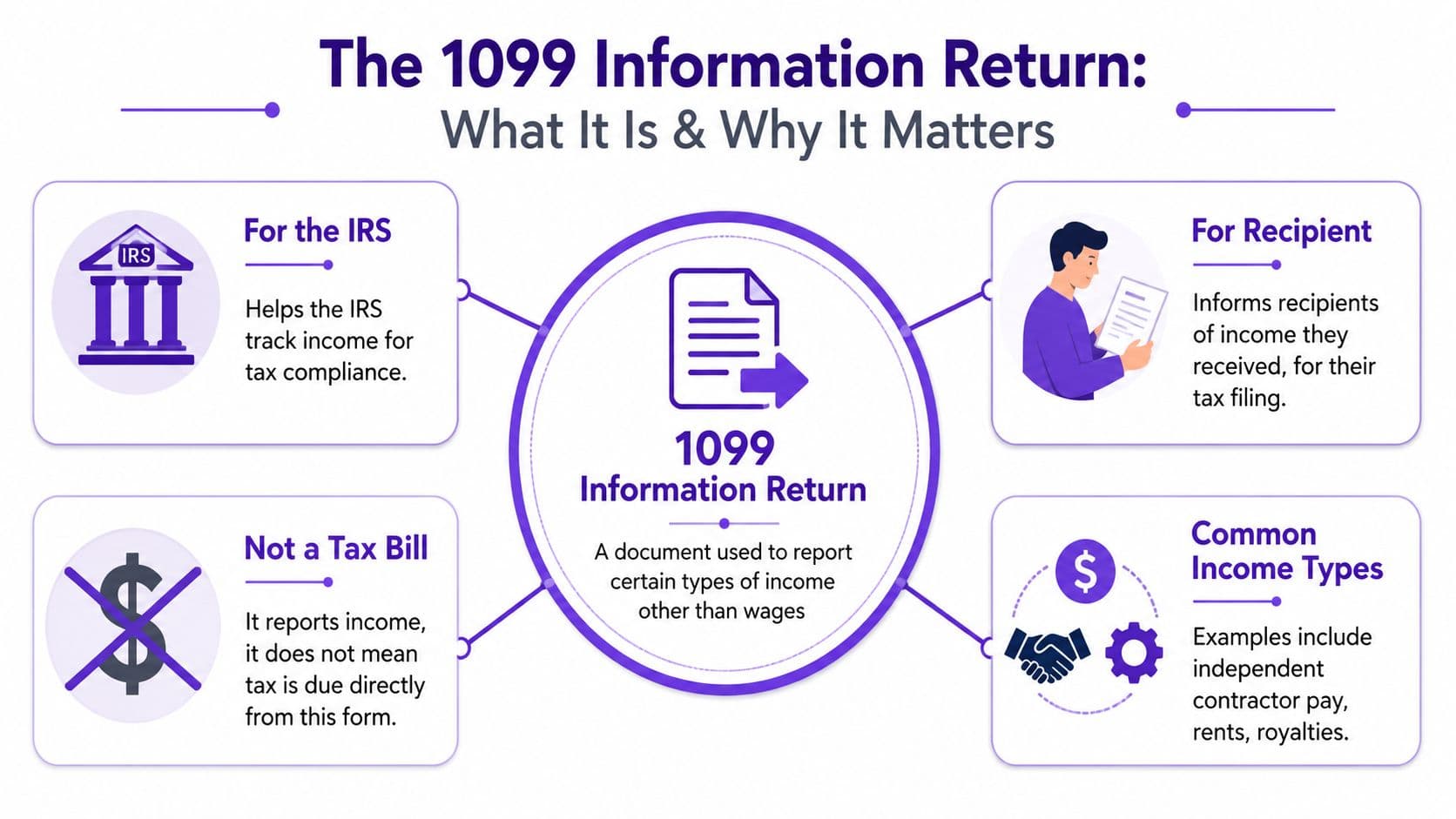

Understanding the Core Purpose of the 1099 Information Return

A 1099 is not a tax bill. It's an information return. Its job is to tell the IRS, "we paid this person or business this type of income," so the IRS can match that record against the recipient's tax return.

That's the main purpose of the 1099 form. It creates a three-way record between payer, recipient, and IRS. You report what you paid. The contractor receives the form. The IRS gets the same information and checks whether the income shows up on the recipient's return.

Think of it as a financial matching loop

If you want a simple analogy, think of the 1099 as a financial data-matching loop.

You initiate the loop when you pay a non-employee. The recipient closes their side when they file their return. The IRS compares both records. That's why the system exists. According to H&R Block's explanation of Form 1099, the primary purpose of the IRS Form 1099 series is to serve as an information return that enables the IRS to verify non-employment income, and the $600 threshold for services has been in place since the Tax Equity and Fiscal Responsibility Act of 1982.

That threshold isn't random. The IRS uses it as the line where service payments become large enough to require mandatory reporting. Other 1099 categories go even lower. Interest, dividends, and retirement distributions can trigger reporting at $10 in the right context, which shows how broad this information system really is.

Why payor and payee roles matter

A lot of filing mistakes happen because businesses don't clearly separate who owes the reporting duty from who receives the form. If your AP team or founder office gets fuzzy on that point, errors multiply fast. A useful primer on understanding payor and payee roles can help clarify responsibility before year-end cleanup starts.

The 1099 doesn't create income. It documents income that already happened.

That's why I push founders to stop thinking of 1099s as forms and start thinking of them as a control system. If you're missing recipient tax IDs, entity types, or payment categories, you don't just have a filing problem. You have a vendor governance problem.

What this means for your finance stack

Your accounting system should answer four questions without detective work:

| Question | What your system should show |

|---|---|

| Who did you pay | Legal name and tax classification |

| Why did you pay them | Clear service or payment category |

| How much did you pay | Total annual amount by payee |

| What form applies | Correct 1099 type or exemption status |

If your books can't answer those questions, year-end 1099 prep turns into manual reconstruction. That's preventable. A qualified tax pro can help, but only if the underlying bookkeeping is solid. That's where understanding what a tax accountant actually handles becomes useful for founders who are still blending bookkeeping, AP, and tax prep into one messy function.

Navigating the 1099 Alphabet Soup NEC MISC K and More

Most founders don't need to memorize every 1099 variant. You do need to know the handful that affect your business. For most SaaS companies, digital agencies, and services firms, the important forms are 1099-NEC, 1099-MISC, and 1099-K. In some cases, you'll also run into 1099-INT and 1099-DA.

The cleanest way to understand them is by economic activity. The IRS splits the 1099 family into separate forms because different payment types map to different tax treatments. According to IRS forms and publications guidance, Form 1099-NEC is for nonemployee compensation, while Form 1099-MISC covers rents, royalties, and attorney payments. That split, introduced in 2020, separated labor payments from other miscellaneous income for clearer audit trails.

Comparison of Common 1099 Forms

| Form | What It Reports | 2026 Reporting Threshold | Common Use Case for Your Business |

|---|---|---|---|

| 1099-NEC | Nonemployee compensation | $600 for service payments in the verified guidance used here | You hired a freelance developer, paid ads specialist, or implementation consultant directly |

| 1099-MISC | Miscellaneous income such as rents, royalties, and attorney payments | $600 for many common business categories, $10 for royalties, $5,000 for direct sales of consumer products for resale outside a permanent retail establishment | You paid office rent, royalties, or legal fees that fall under MISC reporting |

| 1099-K | Payment card and third-party network transactions | Processor reporting can apply at $600 in gross payments under the verified guidance provided here | Stripe, PayPal, or another payment processor reports gross receipts processed for your business |

| 1099-INT | Interest income | $10 | Your business paid reportable interest in a qualifying situation |

| 1099-DA | Digital asset proceeds from broker transactions | Reporting depends on the digital asset rules and exceptions in effect | A business involved in reportable digital asset transactions may encounter this form |

The forms founders misuse most

Let's make this practical.

1099-NEC is the form for contractor labor. If you pay a freelance engineer, copywriter, RevOps consultant, or fractional designer for services, this is the form you're usually evaluating.

1099-MISC is where founders get tripped up. It isn't the old catch-all for contractor services anymore. It's for specific categories like rents, royalties, and attorney payments. One common mistake is assuming incorporated law firms are exempt. They often aren't for this purpose. If you paid an attorney $600, you may still need a 1099-MISC even if the firm is incorporated.

1099-K confuses people in e-commerce and agency businesses because the processor often files it, not you. If your company receives payments through platforms like Stripe or PayPal, the processor's reporting can create an IRS record of your gross receipts that needs to reconcile to your books and tax return.

Real founder scenarios

- Freelance developer: You paid a contractor for app development. Start with 1099-NEC.

- Law firm bill: You paid outside counsel for business legal work. Review 1099-MISC treatment, even if the firm is incorporated.

- Reseller arrangement: If your agency pays $5,200 in direct sales of consumer products to a buyer for resale outside a permanent retail establishment, a 1099-MISC is required. If the total were $4,900, it wouldn't be.

- Processor receipts: Your Shopify or Stripe flows may trigger a 1099-K from the processor, which means your reported revenue needs to tie back cleanly.

If you can't explain why a payment belongs on NEC versus MISC, your chart of accounts is probably doing too much and your vendor setup is doing too little.

A simple classification test

Use this decision lens before you pay:

- Was this payment for services performed by a non-employee? Review NEC.

- Was it rent, royalties, legal payment, or another miscellaneous category? Review MISC.

- Was the income processed through a third-party network? Expect K reporting from the processor.

- Was it interest or a specialized financial transaction? Check the specific 1099 variant.

You don't need a tax department to get this right. You need clear vendor onboarding, consistent coding in QuickBooks or Xero, and one owner of the decision.

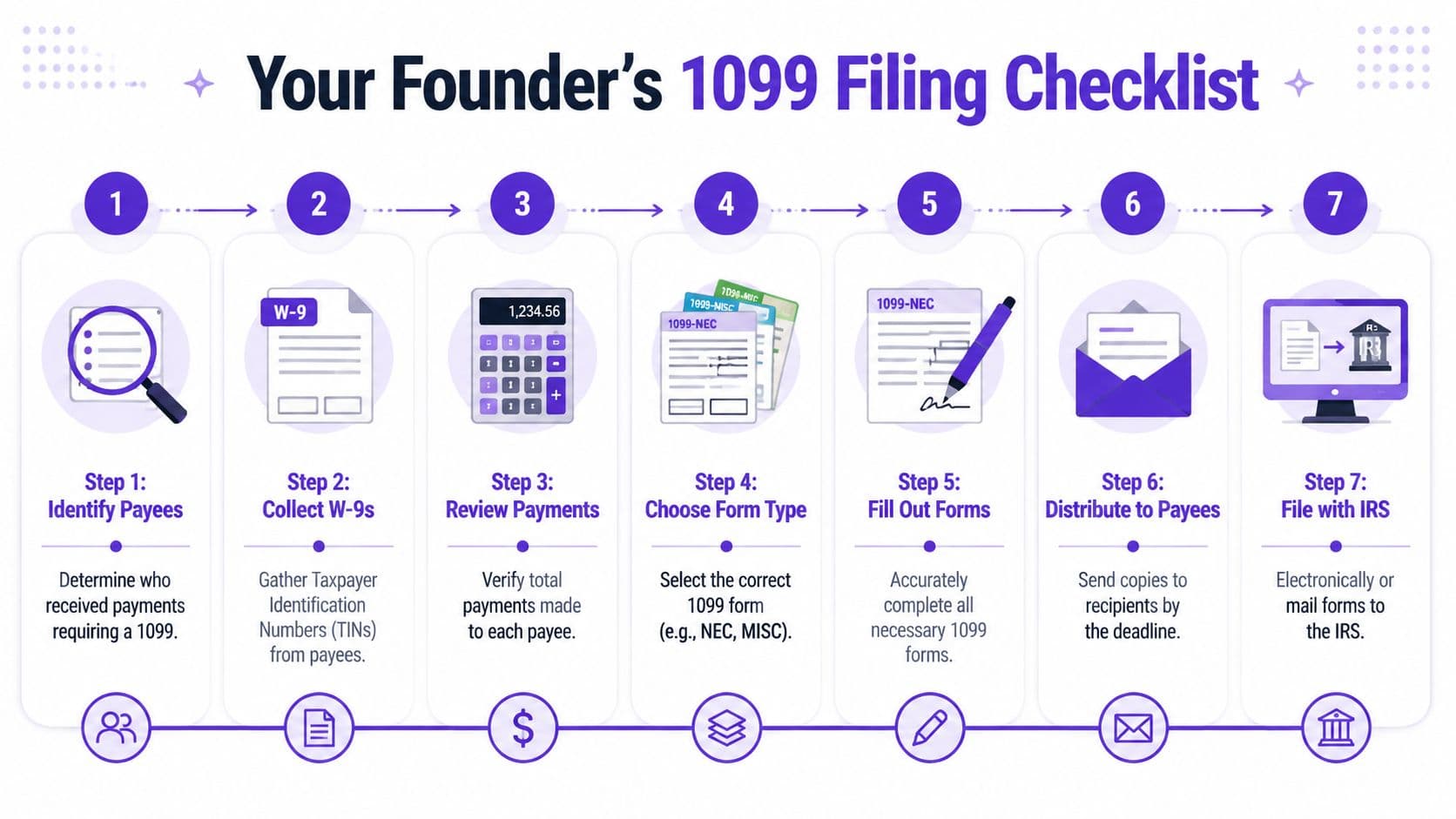

A Step-by-Step 1099 Filing Checklist for Founders

A workable 1099 process starts before the first invoice is paid. If you're chasing tax IDs in January, you're already late operationally. The right process begins at vendor onboarding and runs through filing confirmation.

The seven-step checklist

- Collect the W-9 first. Don't pay a new contractor until you have their legal name, tax classification, and taxpayer ID on file.

- Flag 1099 eligibility in your accounting system. In QuickBooks or Xero, mark vendors that may require reporting.

- Code bills consistently. Put contractor labor, legal fees, rent, and royalties in separate accounts so reporting isn't a cleanup project later.

- Aggregate payments by payee. Look at annual totals per vendor, not invoice size.

- Match the payment to the form type. NEC, MISC, or another variant.

- Distribute recipient copies on time. This is not optional.

- File with the IRS and confirm submission. If you have enough information returns, file electronically.

Later in the workflow, tools like Gusto, QuickBooks, Xero, and Stripe can reduce manual error by centralizing vendor data and payment history. They don't replace review, but they make review faster and cleaner.

For teams closing out the year, a formal year-end close checklist helps keep 1099 prep tied to your broader accounting process instead of leaving it in a separate spreadsheet.

Worked example for a SaaS founder

The IRS example that matters most for growing companies is simple. According to IRS Publication 1220, if your SaaS company pays four independent contractors $1,200 each, you must file a Form 1099-NEC for each contractor.

Here's the math:

| Contractor | Total Paid | 1099-NEC Required |

|---|---|---|

| Developer A | $1,200 | Yes |

| Developer B | $1,200 | Yes |

| Designer C | $1,200 | Yes |

| Consultant D | $1,200 | Yes |

Your total contractor spend is $4,800, but the rule applies per person, not on the combined total.

Now compare that with this scenario:

| Contractor | Total Paid | 1099-NEC Required |

|---|---|---|

| Contractor 1 | $500 | No |

| Contractor 2 | $500 | No |

| Contractor 3 | $500 | No |

| Contractor 4 | $500 | No |

| Contractor 5 | $500 | No |

You paid $2,500 combined, but no individual payee crossed $600, so no 1099-NECs are required in that example.

That's the operational lesson. Your AP process has to summarize total annual payments by vendor. If you're eyeballing single invoices, you're using the wrong lens.

How to use your stack without overcomplicating it

Use the tools you already have:

- QuickBooks or Xero: Maintain vendor profiles, annual totals, and expense coding.

- Gusto: Keep payroll separate from contractor payments so you don't blur W-2 and 1099 treatment.

- Stripe: Reconcile processor inflows to reported gross receipts.

- AP software: Route approvals so somebody reviews vendor type before payment goes out.

To support your team visually, this walkthrough is a useful reference:

Operator's view: The easiest 1099 season is the one you build in February, not the one you scramble through in January.

Deadlines Penalties and Costly 1099 Mistakes to Avoid

The most expensive 1099 mistakes aren't technical. They're procedural. You knew the vendor should probably be reviewed, nobody collected the W-9, January got busy, and now the filing is late.

That sequence is common, but it's still costly. According to the IRS instructions for information returns, if you miss the January 31 deadline for a $10,000 contractor payment reported on Form 1099-NEC, penalties start at $60 per form if you file within 30 days, rise to $120 per form after 30 days but before August 1, and can reach $330 per form after August 1. If you pay 10 contractors late at that top penalty level, that's $3,300.

Penalty math founders should look at directly

| Late filing scenario | Penalty per form | Cost for 1 form | Cost for 5 forms | Cost for 10 forms |

|---|---|---|---|---|

| Filed within 30 days | $60 | $60 | $300 | $600 |

| Filed after 30 days but before August 1 | $120 | $120 | $600 | $1,200 |

| Filed after August 1 or not filed | $330 | $330 | $1,650 | $3,300 |

For a growing company, those numbers aren't catastrophic by themselves. What's worse is what they reveal. Late or missing 1099s usually come with poor documentation, weak vendor controls, and inconsistent books.

Red flags that usually lead to 1099 trouble

- You paid before collecting a W-9: That forces year-end outreach when vendors are least responsive.

- You review invoice amounts instead of annual totals: The rule is based on what each payee received over the year.

- You assume all corporations are exempt: Attorney payments are a common exception under MISC rules.

- You ignore the e-filing rule: If your business files 10 or more information returns, the IRS requires electronic filing under the tax year 2023 rule framework noted in the verified guidance.

- You can't reproduce support quickly: If someone asks for invoices, contracts, and payment history, you shouldn't need a week to assemble them.

One deadline people mix up constantly

Form 1099-NEC has the strictest practical deadline for most founders. Recipient copies and IRS filing are due by January 31. Form 1099-MISC works differently in many cases. Recipient copies are due by January 31, but IRS filing deadlines can differ depending on paper or electronic filing.

The most common 1099 mistake isn't using the wrong form. It's waiting until year-end to figure out who your contractors actually are.

That is why record retention matters. If you don't have contracts, W-9s, invoices, and proof of payment organized, you'll struggle to defend the filing decisions you made. A disciplined business record retention process makes those reviews much easier.

Automate Your 1099 Compliance and Refocus on Growth

Once your company starts using multiple contractors, processors, and outside service providers, DIY 1099 handling stops being efficient. It becomes executive drag. The founder shouldn't be the fallback system for vendor classification, tax form tracking, and late-January cleanup.

The mature move is to automate the parts that software handles well and standardize the parts that require judgment. Use your accounting platform to flag eligible vendors. Use AP workflows to block payment until onboarding documents are complete. Use recurring close procedures to review vendor totals before year-end.

What automation should actually do for you

Automation should do three things well:

| Goal | What good automation looks like |

|---|---|

| Prevent missing data | Vendor setup requires tax and entity information before payment |

| Reduce coding errors | Payment categories map cleanly to contractor labor, legal, rent, and other reportable buckets |

| Speed up filing review | Annual totals and draft forms are easy to review before submission |

This is also where legal process and finance process need to connect. If you're formalizing contractor relationships at scale, tools that help you generate legal contracts with AI can reduce bottlenecks on the front end, as long as legal review stays disciplined and contract terms still match how the person is engaged.

Clear next steps for the next 30 days

If your 1099 process is loose, fix it in this order:

- Audit your vendor list. Identify every non-employee you paid this year.

- Collect missing W-9s now. Waiting only makes response rates worse.

- Review account coding. Separate contractor labor from legal, rent, and other miscellaneous payments.

- Check annual totals by payee. Don't rely on individual invoice amounts.

- Confirm your filing method. If you're over the IRS threshold for information returns, prepare to e-file.

- Tighten AP workflows. A documented process for onboarding and approval saves you next year.

If your payables workflow is still heavily manual, stronger AP automation practices usually fix the root cause faster than another year-end patch.

The purpose of the 1099 form isn't paperwork for paperwork's sake. It's proof that your company can document non-employee payments, defend classification decisions, and keep its books investor-ready while it grows.

If your team is spending too much time untangling contractor payments, late filings, and year-end cleanup, it's time to hand the process to specialists. Jumpstart Partners helps growing SaaS, agency, and services businesses build audit-ready books, cleaner AP workflows, and reliable compliance systems so you can focus on growth instead of form-chasing.