Financial Operations

Returns and Allowances: Master Revenue & Audits

Master returns and allowances for accurate revenue, audits, and valuation. Guide for SaaS, agency, e-com leaders on ASC 606.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··22 min readNearly every founder can quote ARR. Far fewer can quantify the revenue they will have to reverse through contract cancellations, service credits, onboarding refunds, or fee concessions. In SaaS and service businesses, that gap leads to overstated revenue, weak forecasts, and ugly diligence findings.

If you sell subscriptions, implementation work, retainers, or products and you are not tracking returns and allowances with precision, your books are carrying revenue that may never convert into durable cash. Under ASC 606, credits, concessions, and cancellation rights can limit how much revenue you should recognize in the first place. I see this in practice with annual software contracts that get partially refunded after failed onboarding, agencies that issue retrospective credits to save an account, and service firms that discount invoices after a delivery dispute. The accounting entry is small. The valuation impact is not.

Founders often treat refunds as a support issue. Controllers and buyers treat them as a revenue quality issue. If your gross revenue needs repeated clean-up after close, a lender will question forecast reliability, an auditor will test your estimates harder, and an acquirer will push for a lower multiple after a quality of earnings review.

That matters because valuation models are built on expected cash flow, not invoiced optimism. If you need a refresher on discounted cash flow logic, see what is a DCF model and how it powers modern valuations. Misstated returns and allowances do not stay contained in one account. They distort net revenue retention, gross margin, deferred revenue, commissions, and board reporting.

Why Returns and Allowances Are a Hidden Risk to Your Valuation

A buyer or investor doesn’t value your business off the story you tell. They value it off the cash flow they believe will show up.

That’s why sloppy treatment of returns and allowances destroys trust fast. If your top-line revenue includes sales you later reverse, credit, discount, or refund, your reported performance is inflated. In SaaS, that often shows up as churn credits, onboarding refunds, contract cancellations, or service-level credits. In agencies, it shows up as scope concessions, fee reductions, and retrospective credits to keep a client relationship alive. In e-commerce, it’s the classic physical return or damaged-item allowance.

What founders usually miss

A return means the customer gives something back. In product businesses, inventory comes back.

An allowance means you reduce the price but the customer keeps what they bought.

That distinction sounds technical, but it changes your books. A return affects revenue and, in physical-goods businesses, inventory. An allowance affects revenue without changing inventory counts.

According to Study.com’s explanation of sales returns and allowances, if a business records $5,000 in gross sales and customers return $750, net sales are $4,250. That deduction sits in a contra-revenue account called Sales Returns and Allowances. That’s the right presentation because the original sale happened, but not all of that revenue was realized.

For founders, the valuation problem is simple:

| What you report | What diligence asks | What happens if returns are wrong |

|---|---|---|

| Gross sales growth | Net revenue quality | Revenue gets normalized downward |

| Strong gross margin | Whether credits and refunds are fully recorded | Margin gets restated |

| Predictable ARR or MRR | Whether churn-related concessions are reserved correctly | Forecast credibility drops |

| Clean financials | Whether accounting follows GAAP and ASC 606 | Buyer or investor trust erodes |

Why this hits valuation directly

If your board deck, lender package, or CIM uses revenue that later gets clawed back through credits and allowances, every downstream metric gets weaker. Gross margin looks better than it is. Retention looks cleaner than it is. Cash collections look less explainable.

That’s also why a quality of earnings review often focuses on revenue reversals and customer concessions. If you haven’t been through one, read this primer on quality of earnings and what buyers actually test in diligence. It’s where weak return accounting gets exposed.

And if you’re trying to understand how those revenue assumptions feed enterprise value, this guide on what is a DCF model and how it powers modern valuations is worth your time. A DCF doesn’t reward inflated sales. It punishes unreliable cash flow assumptions.

Practical rule: If you need to issue credits regularly to keep customers, those aren’t isolated customer success actions. They’re part of your revenue model and must be reflected that way.

The Mechanics of Accounting for Returns and Allowances

Most errors happen because teams treat a return or credit as a one-line cleanup entry. It isn’t.

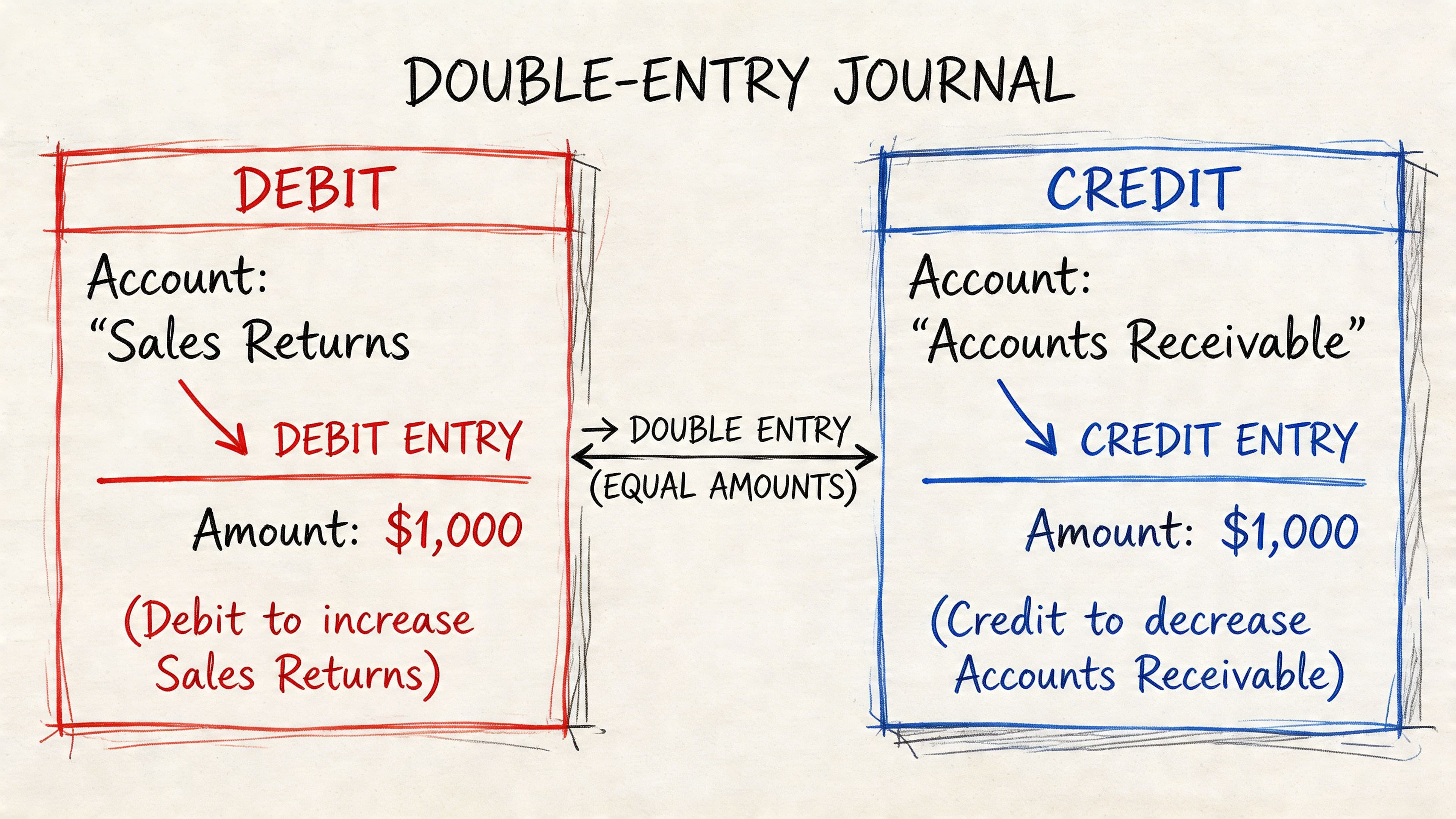

The accounting treatment follows a standard double-entry method. For a sales return, you debit Sales Returns and Allowances and credit either Cash or Accounts Receivable, depending on how the customer paid. If physical goods come back, you also debit Inventory and credit Cost of Goods Sold so the balance sheet and income statement stay aligned, as described in HubiFi’s journal entry guide for returns.

The core logic

Sales Returns and Allowances is a contra-revenue account. It reduces gross sales to arrive at net sales. It does not sit in operating expenses.

That matters because founders often bury customer credits in “goodwill,” “customer success,” or “miscellaneous expense.” That hides the actual shape of your revenue. If you want clean reporting, the reduction belongs against revenue.

Here’s the simplest framework:

| Scenario | Debit | Credit | Extra entry needed |

|---|---|---|---|

| Customer refund on credit sale | Sales Returns and Allowances | Accounts Receivable | No, unless inventory returns |

| Customer refund paid in cash | Sales Returns and Allowances | Cash | No, unless inventory returns |

| Physical goods returned to stock | Inventory | Cost of Goods Sold | Yes, alongside the refund entry |

| Price concession where customer keeps service or product | Sales Returns and Allowances | Accounts Receivable or Cash | No inventory entry |

Worked example for an e-commerce product return

You sell a product for $500 on account. The customer returns it. Assume the item goes back into stock and its original cost was $300.

Your entries:

-

Record the revenue reversal

- Debit Sales Returns and Allowances $500

- Credit Accounts Receivable $500

-

Restore the inventory

- Debit Inventory $300

- Credit Cost of Goods Sold $300

What changes?

- Revenue falls by $500

- Accounts receivable falls by $500

- Inventory rises by $300

- Cost of goods sold falls by $300

Your gross profit effect is the original sale margin being reversed correctly.

Worked example for a SaaS service credit

A SaaS customer receives a $2,000 credit for downtime or a contractual concession. No inventory is involved because nothing physical comes back.

Your entry is usually:

- Debit Sales Returns and Allowances $2,000

- Credit Accounts Receivable $2,000

or credit Cash if you already refunded the customer

The mistake I see most often is posting this to an expense line. That makes revenue look stronger than it is and hides a service delivery issue inside overhead.

If you need a clean refresher on the revenue side of this, review the revenue recognition principle and why timing matters.

Worked example for an agency price allowance

Your agency invoices $10,000 for a project. Later, you grant a 10% allowance because part of the deliverable missed spec. The client keeps the work. There’s no return, only a reduction in price.

The entry:

- Debit Sales Returns and Allowances $1,000

- Credit Accounts Receivable $1,000

Gross sales remain $10,000 in your records. Net sales become $9,000 after the allowance. That gives you a much more honest view of realization by client, by project manager, and by service line.

If your team says, “We’ll just net it against the next invoice,” that’s an operational shortcut, not an accounting policy.

A short visual explainer can help if you need to train a bookkeeper or ops lead on the mechanics:

What works and what fails in software

What works in QuickBooks, Xero, or NetSuite:

- Create a dedicated contra-revenue account. Name it Sales Returns and Allowances.

- Map credit memos correctly. Don’t let them land in discounts or operating expense by default.

- Separate operational reason codes. Downtime credit, scope reduction, damaged goods, cancellation refund. That helps you analyze patterns later.

- Reconcile source systems monthly. Stripe, Shopify, and your accounting ledger should agree.

What fails:

- Posting all refunds to “miscellaneous.”

- Letting the sales team issue credits without finance review.

- Netting credits inside future invoices with no standalone audit trail.

- Ignoring inventory impact when physical goods come back.

Mastering Revenue Recognition and ASC 606 Compliance

A SaaS company can hit its ARR target and still overstate revenue if it ignores cancellation rights, service credits, and contract concessions. That mistake shows up fast in diligence. Buyers recast revenue, reduce confidence in forecasts, and start asking what else finance missed.

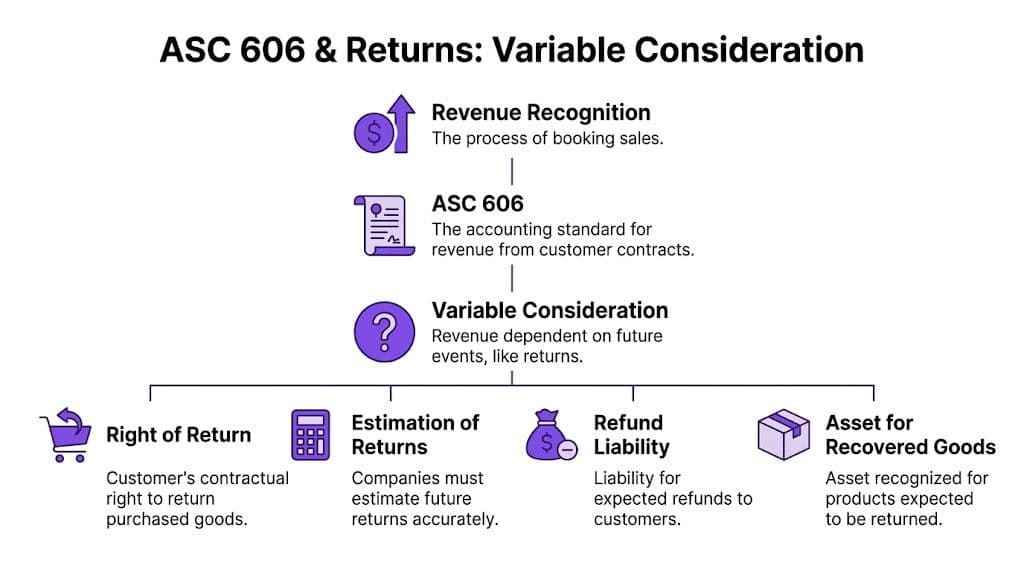

Returns and allowances under ASC 606 are broader than many founders expect. In software and services, the issue usually is not a physical product coming back. It is a customer canceling during an onboarding guarantee period, receiving uptime credits under an SLA, disputing milestone acceptance on a services contract, or negotiating a make-good after poor delivery. Those items create variable consideration, and variable consideration limits how much revenue you can recognize.

Why ASC 606 changes the accounting

ASC 606 requires revenue to be recognized only to the extent it is probable that a significant reversal will not occur. For founders, the practical point is simple. If a portion of invoiced value is likely to be refunded, credited, waived, or reduced later, that portion does not belong in current-period revenue.

I see this break down in three places:

- SaaS contracts with service-level credits that are treated as a future ops issue instead of a current revenue constraint

- Annual prepaid subscriptions with cancellation or satisfaction clauses that are ignored after billing

- Service agreements with vague acceptance terms, where finance books the full amount before delivery risk is resolved

In each case, the invoice says one number and GAAP revenue says another. That gap matters.

Variable consideration in SaaS and services

For SaaS and service businesses, returns and allowances often take these forms:

| Contract situation | What goes wrong | What finance should do |

|---|---|---|

| Annual SaaS contract with uptime credits | Book the full contract value and wait for a support ticket | Estimate expected credits from SLA history and constrain revenue |

| Subscription with early termination rights | Treat billed cash as earned revenue | Recognize revenue only for the amount expected to be retained |

| Implementation project with acceptance risk | Recognize the milestone invoice on issue date | assess whether acceptance is fixed or still uncertain before recognizing revenue |

| Agency or consulting retainer with frequent make-goods | Post credits when the account team asks for them | Reserve for expected concessions based on actual client history |

The accounting is not hard. The discipline is hard.

A founder usually wants the highest defensible revenue number. An experienced buyer wants the most repeatable one. If your books show $4.0 million of ARR but service credits and contract concessions regularly cut realized revenue by 3%, the buyer is already thinking about quality of revenue, forecast reliability, and whether deferred revenue and refund liabilities are understated.

Refund liability is part of the job

If expected refunds or credits exist at the time revenue is recognized, record a refund liability. Do not wait until the credit memo is issued.

A simple SaaS example: a company bills $120,000 for 12 annual contracts at $10,000 each. Based on prior onboarding failures and SLA credits, finance expects $6,000 of concessions. Recognized revenue should reflect that estimate, and the balance sheet should carry the related liability until the credits are used or the estimate changes. If the company books the full $120,000 and fixes it later, monthly revenue is overstated, gross margin is overstated, and board reporting becomes harder to trust.

That is how small policy gaps turn into valuation discounts.

For a clearer breakdown of the rule set, this guide to ASC 606 revenue recognition for growing companies is a useful reference.

Why finance teams get this wrong

The usual problem is not lack of effort. It is bad system design and weak contract handoff.

Sales knows the customer has a 60-day opt-out. Customer success knows the client is owed credits for missed uptime. Delivery knows a milestone will probably be reworked. Finance never gets that information in time, so revenue is recognized as if the contract were fixed and clean.

That is why process matters as much as technical accounting. Contract metadata has to flow from CRM and billing into the ledger. Credit reasons need standard codes. Approval thresholds need to be clear. Teams using efficient returns management systems usually get better visibility into credits and reversals, even if the original use case started in product or support rather than accounting.

MRR and ARR need the same discipline

Founders often separate GAAP revenue from operating metrics and assume the problem stays in the financial statements. It does not.

If MRR includes revenue that is routinely offset by service credits, cancellation concessions, or implementation refunds, MRR becomes a gross billing metric. The board may still use it, but investors will adjust it. I have seen diligence teams rebuild ARR from invoice data, credit memos, support logs, and churn files because management reporting overstated what the company retained.

Strong finance teams do four things consistently:

- Track billings, recognized revenue, and credits as separate measures

- Review contract terms for variable consideration before month-end close

- Record and update refund liabilities monthly

- Reconcile board metrics back to the general ledger

That work protects credibility. Credibility protects valuation.

How to Accurately Estimate and Track Returns

The right estimate is the one you can defend, repeat, and reconcile. Not the one that makes the month look better.

For many businesses, returns and allowances aren’t random. They follow patterns by customer cohort, contract type, channel, product line, implementation team, or season. Your job is to turn those patterns into a monthly estimate that matches reality closely enough to support GAAP reporting and management decisions.

Comparison of return estimation methods

| Method | How It Works | Best For | Pros | Cons |

|---|---|---|---|---|

| Historical percentage of sales | Apply a consistent rate based on prior returns and allowances against current sales | Stable businesses with repeat patterns | Simple to run monthly, easy to explain | Too blunt if products, pricing, or contract terms changed |

| Cohort analysis | Group customers by start date, plan, service line, or sales channel and track later refunds or credits | SaaS, agencies, and businesses with different customer behaviors | More accurate when return behavior varies by cohort | More setup work and cleaner source data required |

| Contract-specific review | Estimate likely credits or reversals based on known contracts and disputes | Larger accounts, enterprise SaaS, custom agency projects | High precision for material accounts | Hard to scale across a broad customer base |

| Hybrid method | Use a baseline rate, then layer in adjustments for known issues or risky cohorts | Growing businesses with mixed revenue streams | Balanced and practical | Requires discipline so adjustments don’t become arbitrary |

What I recommend for most businesses

If you’re between early-stage bookkeeping and full finance maturity, start with a historical percentage and then pressure-test it using cohort behavior.

For example, a SaaS company can look at Stripe refund history, cancellation credits, and churn-related concessions by contract type. An agency can review write-downs by account manager or service line. An e-commerce brand can use Shopify return history by SKU, channel, or campaign.

If your team is evaluating operational process design too, this guide to efficient returns management systems is useful because the accounting estimate is only as good as the return data flowing into it.

How to implement this in QuickBooks or Xero

You don’t need a complex ERP to start doing this properly. You do need a clean chart of accounts and a monthly process.

Set up these accounts:

- Sales Returns and Allowances as a contra-revenue account

- Refund Liability as a balance sheet liability account

- Customer credit reason codes in your source systems or reporting layer

- Separate memo classes if you need reporting by product, service line, or team

Then build a month-end routine:

- Pull actual returns, credits, and allowances from Stripe, Shopify, and your CRM.

- Compare current activity with historical patterns.

- Calculate the estimated refund liability.

- Book the month-end entry.

- Reconcile actual credits issued against the reserve in the next close.

The process only works if it’s part of close discipline. This checklist on month-end close best practices for growing companies is the standard I’d use.

A simple operating model

Here’s the practical version finance teams can live with:

- Weekly: review large credits, cancellations, and unusual customer concessions

- Monthly: true up the reserve and reconcile source systems to the ledger

- Quarterly: revisit the estimation method itself, especially after pricing changes, product issues, or service delivery problems

Controller’s note: If your allowance estimate changes every month because leadership wants a better story, you don’t have a model. You have manual earnings management.

Common objection from founders

“We’re too small for this.”

You’re not too small if investors, lenders, or acquirers expect your revenue to tie out. You’re also not too small if customer credits are frequent enough to change net sales, margin, or cash expectations. The smaller the company, the easier it is for one misclassified contract or one batch of unbooked credits to distort the entire month.

Key KPIs and Internal Controls to Prevent Surprises

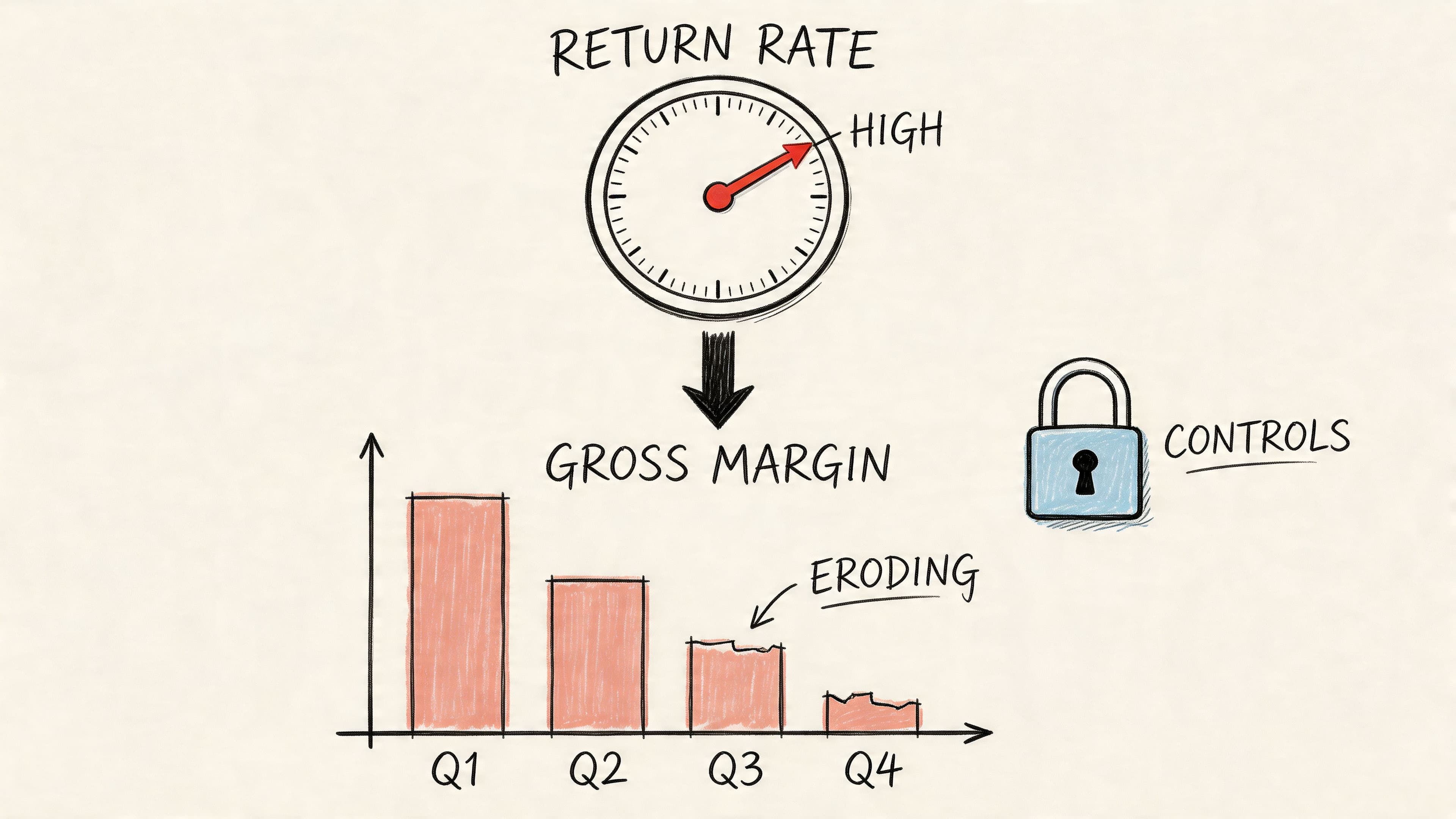

A 2 percent to 5 percent gross margin overstatement is enough to change how a buyer values the business. That range was cited in analysis discussed in this YouTube video, and I have seen the same pattern in diligence when credits, cancellations, and concessions sit outside the revenue process.

Poor handling of returns and allowances shows up fast in SaaS and service businesses because the givebacks are less visible than a physical product return. The problem is not just refunds. It is contract cancellations after invoicing, service credits for missed SLAs, implementation fee reversals, make-goods promised by customer success, and post-sale price concessions that never hit contra revenue. Under ASC 606, those items can constrain revenue long before cash leaves the bank.

The KPIs that get distorted first

Founders usually start with top-line revenue. Buyers, lenders, and diligence teams go straight to the metrics underneath it.

| KPI | What gets distorted when tracking is weak |

|---|---|

| Gross margin | Margin looks better because revenue is not reduced for credits, cancellations, or service failures |

| Net revenue retention | Expansion can look healthy even when the account is being held together with concessions |

| LTV | Lifetime value gets overstated if a meaningful share of billed revenue is later reversed |

| Cash flow forecasts | Expected refunds, credit notes, and contract givebacks are missing from the model |

| Revenue by customer or service line | Unprofitable customers and service packages look acceptable because the givebacks are buried elsewhere |

A SaaS company that books annual billings as if they will all stick can report strong NRR while customer success is issuing free months to prevent churn. A services firm that hides make-goods in payroll or subcontractor expense will not know which clients are profitable. Those errors matter in a sale process. Buyers often run a quality-of-earnings review that traces credits from the CRM, billing system, support desk, and general ledger. If those systems disagree, they lower confidence in the whole revenue number. Use a financial due diligence checklist for founders and you will see how quickly this becomes a valuation issue.

Warning signs your process is broken

A weak process leaves fingerprints.

- Credits cannot be explained by customer, reason, and approver. Sales, finance, and customer success each have a different version of the story.

- Gross margin improves without an operating reason. No pricing change, no vendor savings, no product mix shift. The common cause is missed contra-revenue activity.

- Cash collections lag the P&L every month. The gap often comes from untracked refunds, partial write-downs, or invoices that were never collectible at the stated amount.

- Credit memos live in Slack, email, HubSpot, or a PSA tool. If the ledger only gets part of the picture, revenue is wrong.

- Enterprise accounts get custom concessions. Those are usually the largest exposures and the least standardized.

- Board decks focus on gross billings. That can hide churn credits, SLA penalties, and cancellation refunds.

Controls that actually work

The right controls are boring. That is the point.

- Approval thresholds by dollar amount and type. A $500 goodwill credit should not follow the same path as a $50,000 contract reversal. Set approval rules inside Stripe, Chargebee, NetSuite, or your PSA so people cannot bypass them.

- Reason codes tied to accounting treatment. “Retention,” “implementation failure,” “SLA miss,” “pricing concession,” and “scope dispute” should not all post the same way. Reason codes let finance separate an operating issue from a sales discount.

- Source-to-ledger reconciliation. Match credits and cancellations from Stripe, Chargebee, HubSpot, Salesforce, Zendesk, or your contract system to QuickBooks, Xero, or NetSuite every month.

- Contract review for nonstandard terms. Early termination rights, acceptance clauses, and service-level penalties affect variable consideration and revenue recognition.

- Reserve-to-actual analysis. Compare booked allowance estimates to actual credits issued by cohort, product, and customer segment.

- Segregation of duties. The person who approves a credit should not also post it and clear the reconciliation.

One control matters more than founders expect. Finance needs direct visibility into service credits and commercial concessions before month-end close, not after. If customer success resolves a complaint with a free month and accounting hears about it next quarter, your reported revenue was wrong when it mattered most.

Where valuation gets hit

Investors do not just haircut current-period revenue. They question whether your forecast is dependable. If credits rise with account size, if cancellations spike after implementation, or if service-level penalties are recurring, a buyer will treat that as evidence of weaker retention, weaker pricing power, and weaker controls.

I have seen founders argue that these are “one-off” adjustments. That argument fails when the same pattern shows up in three quarters, across multiple large accounts, with no documented approval trail. At that point, returns and allowances are no longer a cleanup item. They are a revenue quality problem.

Your Action Plan for Bulletproof Financials

You don’t fix this by asking your team to “track refunds better.” You fix it by building a repeatable accounting process that captures every return, allowance, credit, and expected reversal.

The founder checklist

-

Identify every form of revenue giveback

List physical returns, partial refunds, service credits, cancellation refunds, make-goods, write-downs, and post-invoice fee reductions. -

Create the right accounts in your ledger

Set up Sales Returns and Allowances as a contra-revenue account. Add a Refund Liability account if your business needs estimated allowances under GAAP. -

Review how credits are posted today

If credits are landing in operating expenses, discounts, or uncategorized adjustments, rework the mapping. -

Tie source systems to accounting

Pull returns and credit data from Stripe, Shopify, QuickBooks, Xero, NetSuite, or your CRM and make sure the ledger reflects what happened operationally. -

Build a monthly estimate process

Use historical data, cohort behavior, and known contract risk to estimate what revenue you won’t keep. -

Make this part of close

Don’t wait for year-end. Review the reserve and actual returns every month. -

Document the policy

Define what counts as a return, what counts as an allowance, who approves credits, and how entries are posted.

If you’re preparing for fundraising, a lender review, or an acquisition process, run this against a broader financial due diligence checklist for growth-stage companies. Returns and allowances are one of those issues that look small until they unwind your revenue story.

Bottom line: If your financials don’t show the revenue you actually keep, they aren’t investor-ready.

The businesses that get through diligence cleanly aren’t the ones with no credits or refunds. They’re the ones that record them correctly, estimate them responsibly, and explain them without scrambling.

If you want a team that can clean this up, implement the right controls, and deliver investor-ready financials without dragging out your close, talk to Jumpstart Partners. They work with SaaS, agencies, and other growing businesses that need controller-grade accuracy before diligence, not during damage control.