Financial Operations

Schedule G Form 1120: A Founder's Guide to Compliance

A clear guide to Schedule G (Form 1120) for founders. Learn the filing requirements, avoid common mistakes, and see a line-by-line example for your business.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··17 min readThe surprising part about schedule g form 1120 is that many filing problems don't start with tax law. They start with bad process.

The IRS has kept the same basic ownership reporting framework in place for well over a decade, with Schedule G tied to concentrated ownership and voting power disclosures through Form 1120 and Schedule K, according to the IRS Schedule G instructions and this summary of the ownership thresholds. That longevity matters. It tells you this isn't a niche attachment that slips in and out of relevance. It's a durable disclosure mechanism for who controls a corporation.

If you run a SaaS company, agency, or professional services firm with founder equity, investor ownership, or a holding company in the mix, Schedule G is less about paperwork and more about control. When it's wrong, the problem usually isn't that no one knew the rule. The problem is that your cap table, your tax software, and your return review didn't line up.

Why Schedule G Is a Hidden Risk for Your Company

Most founders assume ownership disclosure is easy because “we know who owns the business.” That assumption is exactly where mistakes start.

Schedule G is designed to identify controlling relationships, not just produce a shareholder list. The IRS uses it when a corporation must disclose entities, individuals, or estates that own, directly, 20% or more of the corporation, or own, directly or indirectly, 50% or more of the total voting power of all classes of stock entitled to vote, as described in the Schedule G ownership rules summary. If your business has a clean single-founder structure, this may be straightforward. If you have multiple entities, family ownership overlap, or investor rights, it stops being simple fast.

For founder-led companies, the risk isn't abstract. A tax return that omits a required ownership schedule tells the IRS one of two things. Either the return wasn't reviewed carefully, or the ownership structure itself wasn't understood well enough to be reported correctly.

Why growth companies miss it

In smaller and mid-market companies, ownership data usually lives in several places at once:

- The legal file holds formation documents, stock issuances, and board approvals.

- The cap table tool tracks who owns what after financings, grants, and transfers.

- The accounting system often has no ownership logic at all.

- The tax software depends on someone answering the right Schedule K questions correctly.

That's where the hidden risk sits. Your team can have accurate documents and still file an incomplete return if nobody ties those records into the tax prep workflow.

Practical rule: If ownership changed during the year, assume your Schedule G process needs a manual review, even if your tax software auto-generates forms.

What works is a controlled handoff from cap table review to tax return preparation. What doesn't work is assuming the preparer will “pick it up from the trial balance.” Ownership compliance doesn't live in the trial balance.

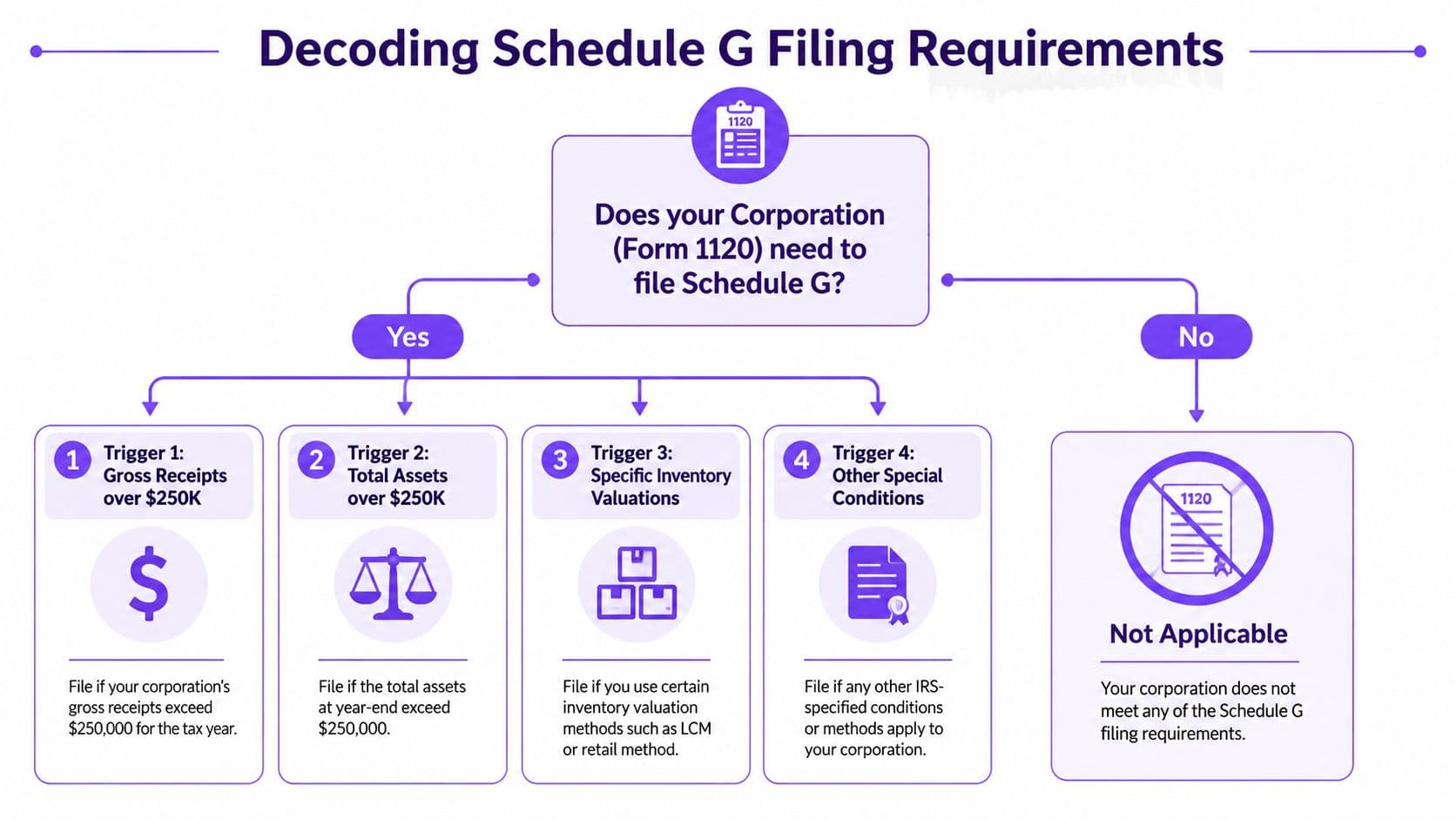

Decoding the Schedule G Filing Requirements

Schedule G gets missed for a simple reason. The filing trigger is mechanical, and it starts inside Schedule K on the corporate return.

If Questions 4a or 4b on Schedule K are answered "Yes," Schedule G belongs in the filing package. If those questions are answered incorrectly, many tax software workflows will never surface the schedule for review. That is why this issue is usually a process failure, not a technical tax knowledge problem.

If you need the broader filing context, this guide to Form 1120 for corporations covers the return itself. For Schedule G, the operational question is narrower. Did the ownership data from your cap table make it into Schedule K accurately enough to trigger the right disclosure?

The two ownership thresholds that matter

Two tests drive the analysis:

| Threshold | What it tests | Why it matters |

|---|---|---|

| 20% direct ownership | Whether an individual, estate, or entity owns at least 20% directly | This identifies significant direct owners who may need to be disclosed |

| 50% voting power, direct or indirect | Whether a person or entity controls voting power through direct ownership or attribution | This captures control relationships even when the cap table looks more fragmented |

In practice, the 20% test is usually straightforward. A founder with 25% of common stock or an investor with 30% of preferred stock gets identified quickly if the cap table is current.

The 50% voting power test causes more trouble. A CEO may hold 18% directly, another 12% through an LLC, and voting rights through a related entity or family ownership chain that pushes total control over the threshold. If nobody traces that path before the return is prepared, Schedule K can be answered incorrectly even when the legal records are sitting in plain view.

Misconceptions I see repeatedly in practice

Several misconceptions appear repeatedly in practice.

- “No one owns more than 50%, so we are fine.” Schedule G can still apply because the direct ownership test starts at 20%, and control can exist through indirect voting power.

- “We already gave the preparer the cap table.” A cap table by itself does not answer the return correctly. Someone still has to map direct ownership, indirect ownership, and voting control into Schedule K.

- “The software will catch it.” Software reflects the inputs it receives. If the Schedule K questions are answered before the ownership analysis is finished, the return can look complete while Schedule G is missing.

The real failure point is usually the handoff. Legal has the documents, finance has part of the ownership story, and tax prep relies on a yes-or-no answer inside the software.

A practical decision test

Use this review sequence before filing:

- Pull the year-end cap table and confirm every transfer, issuance, redemption, SAFE conversion, and entity-level ownership change.

- Flag every direct owner at 20% or more at any point relevant to the filing analysis.

- Review voting control separately from economics because voting rights do not always match equity percentages.

- Trace indirect ownership paths through holding companies, family relationships, and related entities where attribution may matter.

- Check how Schedule K Questions 4a and 4b were answered in the tax software.

- Confirm Schedule G is attached before e-file submission if the ownership analysis requires it.

That sequence is what closes the gap between the cap table, Schedule K, and the final Form 1120 filing. An outsourced controller usually adds the most value here by owning the workflow, reconciling records across teams, and forcing the review before the return is finalized.

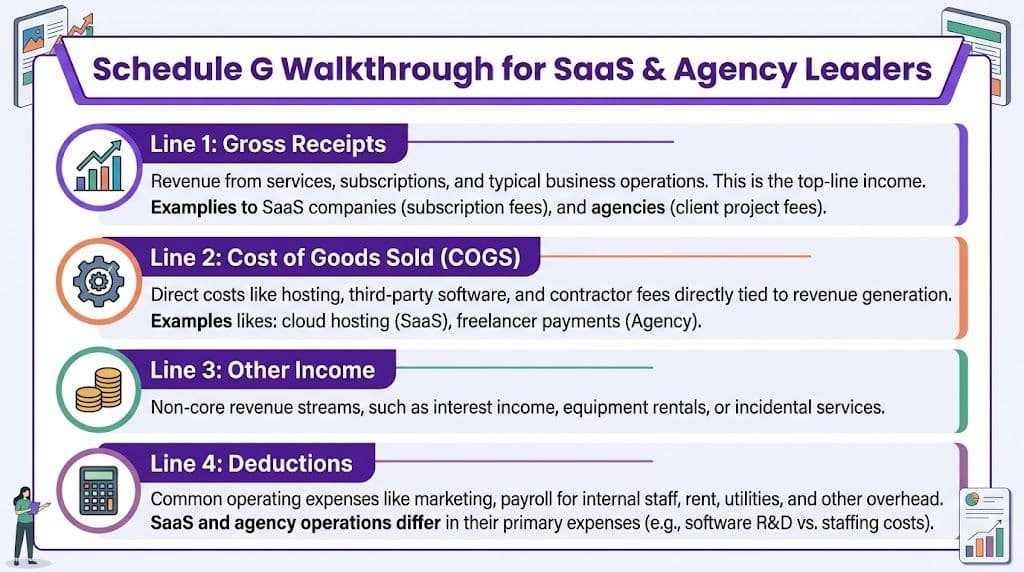

A Practical Walkthrough for SaaS and Agency Leaders

Schedule G problems usually start long before tax prep. They start when the cap table, the controller's ownership analysis, and the Schedule K answers are not reconciled into one filing decision.

Use a realistic SaaS fact pattern. Your corporation has four owners:

- Founder A owns 40% directly

- Co-founder B owns 15% directly

- A VC fund owns 30% directly

- A holding company owned by Founder A owns 15% directly

On direct ownership alone, Founder A and the VC fund are already in the reportable range. The harder issue is control. If Founder A owns the holding company, the tax analysis cannot stop at the cap table export because voting power and indirect ownership may push Founder A above the reporting threshold even though the direct line shows only 40%.

That is why this form matters more for SaaS and agency operators than many guides admit. Equity grants, SAFE conversions, secondary transfers, and holding company structures create reporting changes that accounting teams often do not see in time. If your finance stack already struggles with revenue recognition, deferred revenue, and close timing, this guide to accounting for SaaS companies is a useful companion because the same control discipline applies here.

Worked ownership analysis

Start with the direct ownership view:

| Owner | Direct ownership | Filing implication |

|---|---|---|

| Founder A | 40% | Reportable based on direct ownership |

| Co-founder B | 15% | Direct ownership alone does not trigger reporting |

| VC fund | 30% | Reportable based on direct ownership |

| Founder A holding company | 15% | Requires separate review as an entity owner |

Now test indirect control. If Founder A owns that holding company, the practical question is whether Founder A's ownership relationship to the corporation is effectively:

40% direct + 15% indirect = 55%

That result changes the filing analysis. I see teams miss this point when they export the year-end cap table, note that no individual is above a simple majority directly, and move on. Schedule G requires a closer review of who ultimately holds the reportable ownership or voting relationship after tracing the chain.

How this maps into the return

The form becomes manageable once the ownership review is finished before tax prep starts.

Part I for entities

Entity owners belong in the entity reporting section. In this example, the VC fund at 30% is the obvious case. The holding company may also need to be reported depending on the final ownership analysis and how the corporation applies the instructions to the structure.

Have these records ready:

- Legal entity name

- Address

- Tax identification number if required

- Ownership percentage

- Whether the interest is direct, indirect, or both

Part II for individuals or estates

Individuals who meet the reporting threshold belong in the individual section. Founder A belongs here based on the direct 40% interest alone, and the indirect relationship may affect how that ownership is disclosed.

Prepare:

- Legal name

- Address

- Taxpayer identification information as required

- Citizenship information if requested by the form

- Ownership percentage and ownership type

The real calculation problem

The challenge is not entering names into software. The challenge is determining the correct ownership percentage after changes during the year and making sure that conclusion reaches the preparer before Schedule K is finalized.

Consider a common agency or SaaS sequence. A founder starts the year at 55%, raises capital, and ends at 40% direct ownership. Separately, that founder owns an entity that still holds another 15%. A legal file may show all of this. The tax return can still be wrong if finance answers the software questions from the ending direct percentage only.

This is a process failure, not a knowledge failure.

I usually want one person, often an outsourced controller, to own the handoff from cap table to tax workpapers. That person does not need to prepare the return. They need to reconcile legal records, investor documents, and the ownership analysis so the preparer is not guessing from partial data. For founder-heavy companies that also manage contractor complexity, tools such as the Xpenses paycheck calculator for independent contractors can help keep worker-payment workflows organized, but Schedule G still requires a separate ownership-control review.

A review process that works

Use this operating sequence before the return goes out:

-

Freeze the ownership record used for tax

Tie the filing analysis to a specific cap table version and include transfers, issuances, repurchases, SAFE conversions, and entity ownership changes. -

Run the direct owner test

Identify every person or entity at or above 20% direct ownership. -

Run the indirect and control test

Trace holding companies and other ownership paths to determine whether anyone crosses the voting power threshold. -

Build the reporting list before software input

Decide which owners belong in the entity section and which belong in the individual section before answering the Schedule K trigger questions. -

Reconcile the final list to the return

Confirm the Schedule G names, percentages, and owner types match the completed ownership memo.

That workflow closes the gap that causes missed filings. The tax rule is usually not the part that breaks. The breakdown happens when legal has the documents, finance has a spreadsheet, tax has software prompts, and no one owns the reconciliation.

Common Mistakes That Put Your Business at Risk

The most common Schedule G failure isn't misunderstanding the rule. It's assuming one system already captured it.

Tax software support materials show that Schedule G is triggered from Form 1120 Schedule K, questions 4a and 4b, and that creates a process-control problem: your team has to reconcile cap-table data with software logic so the return is complete before filing, as explained in this tax software support note on Schedule G triggering. That's an operations issue disguised as a tax issue.

Red flags that deserve immediate review

| Warning sign | Why it matters |

|---|---|

| Cap table changed after financing or equity grants | Schedule K inputs may now be stale |

| Ownership is tracked in spreadsheets and legal PDFs only | Tax prep software won't infer reportable owners |

| One person reviews the return without cap table support | Indirect ownership is easy to miss |

| Foreign or entity owners appear in the structure | Identification details often come in incomplete |

Four mistakes I see repeatedly

-

Treating the cap table as a legal document only

Legal may maintain the records, but tax reporting needs a finance-ready ownership summary. If your preparer receives PDFs without a reconciled ownership schedule, errors multiply. -

Ignoring indirect ownership paths

Founders often focus on direct stock certificates and ignore ownership held through another entity. That's where the control analysis breaks. -

Letting payroll and owner data drift apart

In smaller firms, the same person often appears as shareholder, officer, contractor, or all three over time. When teams are already cleaning up owner compensation, contractor status, and withholdings, tools like the Xpenses paycheck calculator for independent contractors can help validate related compensation assumptions, but they do not solve ownership reporting. Keep those workflows separate and reconciled. -

Reviewing the return too late

If Schedule G gets considered only during partner signoff, everyone is working backward from a nearly finished return. By then, the issue is harder to fix cleanly.

A missing Schedule G often signals that no one owned the handoff between equity records and tax preparation.

If your year-end process already includes audit support, a stronger close-and-review checklist like this auditor preparation checklist helps because it forces ownership documentation into the broader compliance workflow instead of leaving it as a last-minute tax attachment.

Your Schedule G Documentation Checklist

You can make Schedule G far less painful by building the file before tax prep starts. Most delays come from missing ownership support, not from the form itself.

If you keep records under a formal retention policy, align this package with your broader business records retention process so the same documents are easy to retrieve each year.

Schedule G preparation checklist

| Information / Document | Purpose | Where to Find It |

|---|---|---|

| Current cap table | Identifies direct owners and ownership percentages | Cap table software, legal records, board files |

| Prior-year cap table | Shows ownership changes during the year | Prior legal or finance archives |

| Stock purchase agreements | Supports who acquired shares and when | Legal counsel files, deal folders |

| Shareholder or investor agreements | Clarifies voting rights and restrictions | Legal data room |

| Entity formation documents for owner entities | Helps trace indirect ownership through holding companies or funds | Secretary of state records, legal counsel |

| Board consents and equity approvals | Confirms issuances, transfers, and option exercises | Corporate minute book |

| Owner identification details | Needed for completing reportable owner information | W-9 files, onboarding records, legal files |

| Addresses for owners | Supports complete form preparation | AP vendor file, legal records, owner questionnaires |

| Tax identification information where required | Supports required owner disclosures | W-9s, tax organizer responses |

| Voting rights summary | Distinguishes economic ownership from control | Charter, bylaws, investor docs |

| Ownership attribution memo or internal summary | Documents indirect ownership reasoning | Tax preparer workpapers, controller review file |

| Final Schedule K answers | Confirms the software trigger is set correctly | Tax software output, preparer draft |

What to hand your CPA

Don't send a folder full of raw PDFs and expect a clean result. Send:

- A reconciled ownership summary

- A list of reportable individuals and entities

- A note on indirect ownership conclusions

- Any changes that occurred during the year

That package reduces back-and-forth and gives the preparer something they can test against the return.

How to Automate Compliance and Eliminate Errors

The fix for Schedule G problems is not “be more careful next April.” The fix is building a repeatable ownership-control process.

A strong process starts with one source of truth for equity records, then pushes that data into tax prep review instead of leaving the preparer to reconstruct ownership from scattered documents. That's especially important when founders, investors, and affiliated entities all appear in the same structure.

What automation should actually do

Automation isn't about letting software decide ownership law. It's about reducing manual failure points.

A workable setup usually includes:

| Process area | What good looks like | What fails |

|---|---|---|

| Ownership records | One maintained cap table with dated changes | Multiple spreadsheets and stale PDFs |

| Document collection | Standard owner packet collected before tax prep | Last-minute email chase for IDs and agreements |

| Tax prep handoff | Schedule K answers reviewed against ownership memo | Software defaults accepted without challenge |

| Final review | Return checked against cap table and voting analysis | Return reviewed only for math and signatures |

Useful tools, used the right way

Many finance teams now use document extraction to reduce manual rekeying from legal PDFs and tax support files. If your ownership support lives in scanned agreements or board packets, tools that extract text and data with OkraPDF can help standardize data capture. That's useful for speed. It does not replace judgment on attribution or voting control.

What works is combining automation with a named reviewer. Usually that's a controller, outsourced controller, or tax manager who owns the reconciliation between cap table, supporting documents, and the return draft.

Good compliance systems don't rely on memory. They force the ownership review to happen before the return is considered final.

If you're tightening your close process more broadly, this guide to financial reporting automation is a good companion because Schedule G errors often trace back to the same broken handoffs that affect month-end reporting.

The practical next steps are simple:

- Pull your current cap table and year-end ownership documents

- Identify all direct owners above the reporting threshold

- Map any indirect ownership through related entities

- Review the Schedule K answers in your tax software

- Confirm Schedule G is attached before filing

- Assign one person to own this review every year

For a founder or CEO, that last step matters most. If no one owns the process, the process fails.

If your team wants help tightening the ownership-to-tax workflow behind Schedule G, Jumpstart Partners can help you build a cleaner controller process around cap table reconciliation, tax prep support, and year-end review so this filing is handled correctly every year.