Financial Operations

What Is Accounts Receivable Aging Report: What Is Accounts

Discover what is accounts receivable aging report, how to read it, and its impact on cash flow. Essential guide for founders & CEOs.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··19 min readYour revenue looks fine. Your profit and loss statement says the business is working. Then payroll week hits, a tax payment clears, and your bank balance gets tight for no obvious reason.

That problem usually isn't revenue. It's timing. You booked the sale, sent the invoice, recognized the income, and still didn't get the cash.

If you're asking what is accounts receivable aging report, here's the blunt answer. It's the report that tells you whether your invoiced revenue is turning into cash, or whether you're funding your customers instead of your own growth. For a founder running a SaaS company, agency, or professional services firm, this report belongs in the same category as your cash balance and runway. Ignore it and you'll make bad hiring, spending, and fundraising decisions off a false sense of security.

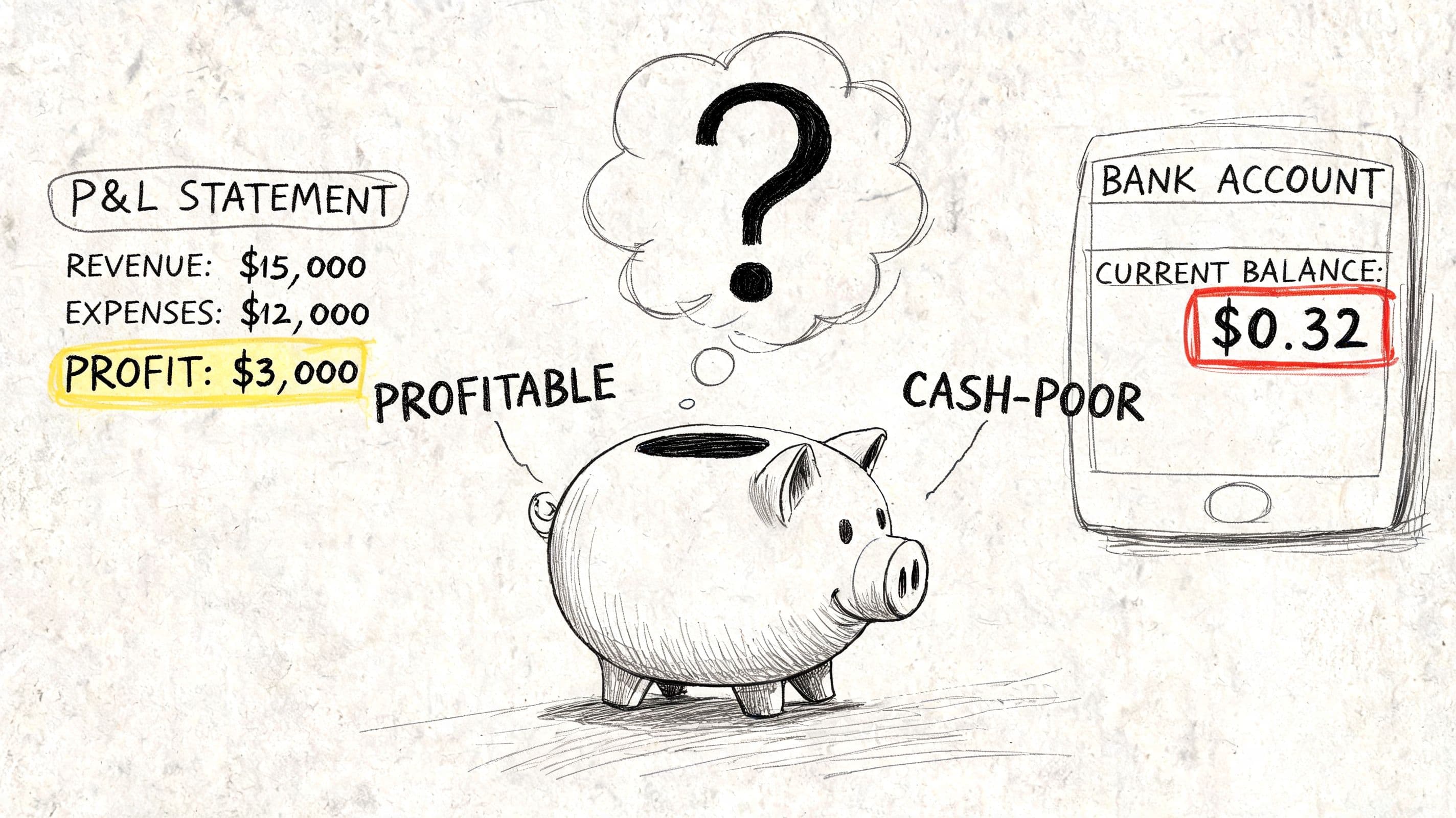

Why Your Profitable Company Is Still Cash-Poor

You close a strong month. The P&L shows profit. Then payroll hits on Friday, a quarterly tax payment clears, and you delay a hire because the bank account is thinner than it should be.

That happens because profit measures earnings. Cash measures survival.

An accounts receivable aging report shows which invoices are still unpaid and how overdue they are, usually in 0-30 days, 31-60 days, 61-90 days, and 91+ days past due buckets. Founders should use it as a weekly cash control tool, not just an accounting report. It tells you how much of your reported revenue is likely to convert into cash in time to fund operations.

That distinction matters even more in SaaS and agency businesses. You can recognize revenue before cash arrives. Under ASC 606, a SaaS company may spread recognized revenue across a contract term while cash comes in upfront, monthly, or late. Agencies deal with their own version of the problem when retainers, milestone billing, pass-through media costs, and client approval delays distort timing. Your income statement can look clean while collections lag badly underneath.

Profit isn't the same as liquidity

Founders get in trouble when they treat booked revenue as spendable cash. It isn't. If receivables age past your stated terms, your business starts financing customers with your own balance sheet. That cash drain usually shows up in the same places first:

- Payroll

- Tax payments

- Contractor invoices

- Ad spend

- Product investment

That is a working capital issue. If you need the broader operating framework, read working capital management for growing companies.

Here is the pattern I see all the time. A SaaS company closes annual contracts, reports solid revenue, and assumes the cash position is improving. Then a few enterprise customers pay 45 or 60 days late, commissions have already gone out, and leadership is suddenly managing around the bank balance. An agency has the same problem when client invoices sit unpaid while payroll and media vendors still need to be paid on schedule.

Practical rule: Review receivables at least as often as you review revenue. Weekly is the right cadence for any founder managing growth, hiring, or fundraising.

What this report really tells you

A good AR aging report answers operating questions fast:

- Which customers pay on time

- Which balances are slipping into risk

- Whether your payment terms are too loose for your cash cycle

- How much of your AR is concentrated in a few accounts

- Whether collections issues are isolated or systemic

That last point matters for investor readiness. Buyers, lenders, and diligence teams do not just ask whether you are growing. They ask whether revenue converts to cash, whether collections are predictable, and whether old receivables will turn into write-offs. If your aging report is messy, they will question forecast accuracy, revenue quality, and internal controls.

Modern finance teams are getting more aggressive here. They use historical payment patterns to predict which accounts will slip into the 60+ or 90+ day buckets before the invoice is old. That gives you time to change terms, escalate outreach, or adjust cash planning early. Founders do not need fancy software to start. They do need the discipline to treat aging trends as an early warning system, not a rearview report.

For a profitable company, cash problems usually start in receivables long before they show up in the bank account. The aging report helps you catch that early.

Anatomy of an AR Aging Report

Most founders overcomplicate this report at first. Don't. The structure is straightforward. Think of it as a health chart for your customer balances.

The core fields you need

A useful aging report includes invoice-level detail, not just a summary total. At minimum, you should see:

| Field | What it tells you | Why it matters |

|---|---|---|

| Customer name | Who owes you money | Helps you spot concentration and chronic late payers |

| Invoice number | Which bill is unpaid | Lets your team follow up precisely |

| Invoice date | When the invoice was issued | Helps identify billing delays |

| Due date | When payment was expected | This is the date used for aging |

| Amount due | Outstanding balance | Shows the cash still uncollected |

A decent report from QuickBooks, Xero, or NetSuite can give you all of this. If your team is still building it manually in spreadsheets, you can make it work, but you'll spend more time cleaning data than collecting cash.

The aging buckets

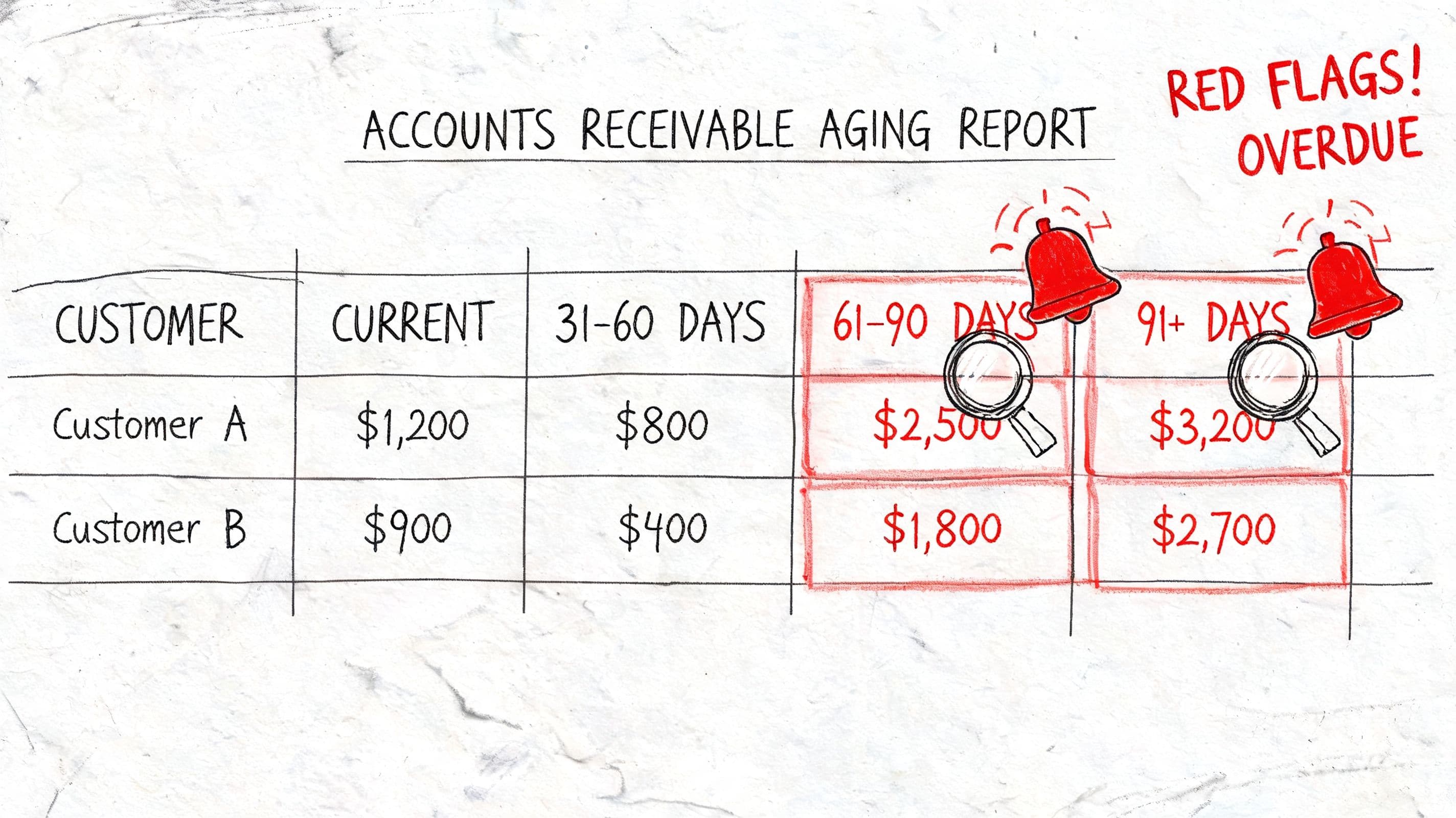

This is the heart of the report. Each unpaid invoice gets assigned to a time bucket based on the number of days between the due date and the report date.

The standard buckets are:

-

Current or 0-30 days

These invoices are not meaningfully late, or are still within normal terms. -

31-60 days In this stage, excuses start. Approval delays, missing PO claims, and “we'll pay next cycle” usually show up here.

-

61-90 days

Now you have a real collections problem. The issue is no longer administrative. It needs active owner attention. -

91+ days

This is danger territory. At this age, you're no longer managing timing. You're managing loss risk.

How the report is built

The mechanics are simple. For each invoice:

- Take the report date

- Subtract the invoice due date

- Assign the balance to the right bucket

- Sum the balances by customer and by bucket

That sounds basic because it is. The value isn't the math. The value is the visibility.

Your aging report should let you drill from total AR down to a single invoice without asking anyone to “pull backup.”

For a SaaS company, this report often exposes invoices tied to implementation fees, annual prepayments, or enterprise billing exceptions. For an agency, it reveals which retainers are clean and which project invoices are stuck in client approval loops. Same report. Different operational story.

How to Read Your Aging Report and Calculate Key Metrics

A founder sees $400,000 in accounts receivable and assumes cash is covered for payroll, ad spend, and debt service. Two weeks later, the bank balance says otherwise. The aging report explains the gap.

Read this report in the order that affects cash fastest. Start with bucket mix, then measure collection speed, then test whether your balance sheet is overstating what you will collect.

Start with the bucket mix

Total AR is a vanity number. The age of that AR tells you whether it will fund the business.

Use simple percentages for each bucket:

Bucket percent = Bucket balance / Total AR

Here is a clean benchmark set:

| KPI | Healthy range |

|---|---|

| AR Total Current Percent | 80-90% |

| 30-60 Days Percent | <10% |

| 60-90 Days Percent | <5% |

| Over 90 Days Percent | <5% |

If your current bucket is below that range, cash collection is lagging sales. If your 60+ day balances keep rising, your team is financing customers with your own operating cash.

For SaaS, I pay close attention to annual contracts, onboarding invoices, and enterprise billing exceptions. Those balances often look collectible right up until procurement stalls or a disputed implementation milestone delays payment. For agencies, the usual trap is different. Retainer invoices may stay current while project change orders and out-of-scope work slide into older buckets because nobody locked down client approval.

Calculate DSO the right way

Days Sales Outstanding, or DSO, measures how long it takes to convert invoices into cash.

The standard formula is:

DSO = (Average AR × 360) / Credit Sales

Worked example:

- Average AR = $300,000

- Credit sales for the period = $2,400,000

Calculation:

DSO = ($300,000 × 360) / $2,400,000 = 45 days

That means you collect cash in 45 days on average.

For a SaaS company billing on net-30 terms, 45 days may be manageable but not clean. For an agency with payroll every two weeks, 45 days can create real pressure if a few large clients slip at the same time. Once DSO drifts far above your stated payment terms, you have an execution problem, a contract problem, or both.

If you want a second collection-speed metric, review accounts receivable turnover and what it reveals.

One warning for investor readiness. DSO gets distorted in SaaS businesses that have annual prepayments, milestone invoices, credits, or contract modifications. Under ASC 606, revenue recognition and invoicing timing often diverge. An investor or lender will notice if booked revenue looks strong while receivables age poorly. They will ask whether the issue is collection discipline, contract structure, or revenue quality. You need that answer before the diligence request comes in.

Build an allowance for doubtful accounts

Founders hate reserves because reserves make the balance sheet look weaker. Set the reserve anyway.

An aging-based allowance forces you to estimate what part of AR will not convert to cash. It also stops you from presenting an inflated asset number to lenders, buyers, or investors.

A simple example:

- 2% on 0-30

- 10% on 31-60

- 25% on 61-90

- 50% on 91+

Example AR balance:

| Bucket | Balance | Reserve rate | Reserve |

|---|---|---|---|

| 0-30 | $100,000 | 2% | $2,000 |

| 31-60 | $40,000 | 10% | $4,000 |

| 61-90 | $20,000 | 25% | $5,000 |

| 91+ | $10,000 | 50% | $5,000 |

Total allowance for doubtful accounts = $16,000

That reserve does two things. It gives you a more honest net AR number, and it shows investors that management understands collection risk instead of hoping old invoices will somehow clear.

Turn the report into a forecast tool

Good operators set themselves apart.

Do not treat the aging report as a backward-looking collections file. Use it to forecast weekly cash receipts. If 85% of your current bucket usually pays within 30 days, but only a small share of your 61-90 bucket does, your cash forecast should reflect that pattern. SaaS finance teams are starting to use AI tools and historical payment behavior to score which invoices are likely to pay late, which accounts need executive escalation, and which customers show churn risk before they miss renewal. Agencies can do the same by tagging invoices by client, project type, account manager, and approval path.

That is how the aging report becomes more than an accounting artifact. It becomes a cash planning tool and a diligence-ready signal that your revenue operation is under control.

Red Flags That Signal a Cash Flow Crisis

Friday afternoon. You approve payroll, your controller says revenue was strong, and your bank balance still looks wrong. That gap usually shows up in the aging report first.

A healthy book usually keeps 80% to 90% of receivables in the current bucket. Once more than 10% sits in 90+ days, cash risk is real. If that older bucket keeps climbing, stop calling those invoices “near-term cash.” They are turning into a financing problem.

That distinction matters more in SaaS and agencies than founders admit. In SaaS, annual prepay, implementation fees, usage true-ups, and ASC 606 timing can make the P&L look cleaner than the cash picture. In agencies, change orders, client approval chains, and out-of-scope disputes push invoices into older buckets fast. Investors and lenders will look past recognized revenue and ask a simpler question: how much of AR converts to cash on time?

Warning signs that need action now

A bad aging report rarely starts with one giant write-off. It starts with a pattern.

-

Current receivables are shrinking month after month

Your billing cycle is slow, your invoice delivery is sloppy, or customers have learned they can pay late without consequence. -

The 61 to 90 bucket is getting crowded

This usually points to unresolved disputes, missing purchase orders, weak follow-up, or account managers protecting client relationships instead of pushing for payment. -

The 91+ bucket is growing faster than new billings

Now you have a collections issue and a credibility issue. Older AR distorts your cash forecast and inflates working capital on paper. -

One client accounts for a large share of overdue balances

Concentration risk can choke an otherwise profitable agency. In SaaS, one late enterprise customer can throw off hiring plans if you counted on a renewal or expansion invoice landing this month. -

Invoices keep rolling forward into older buckets

That tells you the process is failing. Reminder emails are not enough. Somebody needs ownership, escalation rules, and authority to pause work or tighten terms.

What each red flag usually means

| Red flag | Likely root cause | Business consequence |

|---|---|---|

| Weak current bucket | Billing delays, poor invoice accuracy, weak follow-up | Erratic weekly cash and avoidable borrowing |

| Large 61 to 90 balances | Disputes, approval bottlenecks, unowned collections | Forecast misses and slower month-end close |

| Large 91+ balances | Loose credit policy or refusal to escalate | Higher bad debt risk and lower net AR quality |

| Overdue AR concentrated in one account | Customer concentration risk | One payer can disrupt payroll, vendor payments, or tax deposits |

| Rising overdue balances despite revenue growth | Revenue quality is weaker than reported growth suggests | Lower investor confidence during diligence |

For investor readiness, this section matters because diligence teams do not stop at top-line growth. They test whether booked revenue turns into cash predictably. If your SaaS company recognizes revenue over the contract term under ASC 606 but collections lag because implementation was disputed or procurement stalled, the aging report exposes the operational problem. If your agency books a strong month but two large clients sit at 75 days outstanding, the quality of earnings story weakens fast.

Use the report before you approve hiring, bonuses, owner distributions, or ad spend. If you need a practical framework for that, review these cash flow improvement strategies for growing service and SaaS businesses.

This walkthrough is useful if you want to see the report mechanics in action:

One more point. A static aging report is already behind. Strong finance teams now score invoices by payment history, customer behavior, contract type, and dispute patterns so they can predict which balances will slip before they become 90+ day problems. That matters in board meetings and fundraising because predictive collections discipline looks very different from “we are following up.”

If old balances keep aging forward, treat that as an operating failure. Then fix it with tighter contracts, cleaner invoicing, and a documented escalation path for collecting business invoices.

Your Action Plan for Unpaid Invoices

You don't fix aging by “keeping an eye on it.” You fix it with a collections process that escalates by invoice age and assigns ownership.

Use a tiered response, not random follow-up

Here is a practical playbook you can put in place now.

| Aging Bucket | Recommended Action | Goal |

|---|---|---|

| Current | Send automated reminder before and at due date. Confirm invoice receipt and payment method. | Prevent avoidable lateness |

| 1-30 days | Send a polite follow-up email with invoice copy and due date reference. | Get paid without friction |

| 31-60 days | Move from email to direct outreach. Call the client, identify dispute or approval blocker, and document next step. | Resolve the actual reason payment is stuck |

| 61-90 days | Escalate internally and with the client. Pause new work or tighten terms where appropriate. | Stop the balance from aging into probable loss |

| 91+ days | Send a final demand notice, evaluate outside support, and decide whether to place account on credit hold or move toward write-off review. | Recover cash or contain damage |

What founders should require from the team

A proper collections process is operational, not emotional. It should include:

-

Named ownership

Every overdue balance needs a person responsible for follow-up. -

Documented dispute reasons

“Client hasn't paid” is not a reason. Missing PO, scope disagreement, billing contact left, and payment system issue are reasons. -

A no-surprises escalation path

Sales, account management, and finance should know when overdue invoices trigger a hold on new work. -

Weekly review cadence

Review overdue AR every week. Monthly is too slow for a growing business.

If your team needs a legal overview of collecting business invoices, that resource is worth reading before you formalize final-demand and escalation language.

Common objection from founders

The usual pushback is, “We don't want to annoy good clients.”

That's the wrong frame. Professional collections don't damage strong relationships. Sloppy billing, unclear scope, and inconsistent follow-up do.

Founder rule: The client who values your work won't be offended by a clear invoice process. The client who resists every follow-up is already telling you something about credit risk.

If overdue invoices are putting pressure on payroll timing or growth decisions, don't wait for month-end. Tighten terms, shorten feedback loops, and connect AR review to cash flow improvement planning.

Advanced AR Management for Modern Business Models

A generic AR process isn't enough once your business gets more complex. SaaS, agencies, and hybrid service models each create different aging problems.

SaaS needs AR tied to ASC 606

For SaaS companies, one major failure point is treating the aging report like a basic billing list when the contract structure is more complicated. Multi-year deals, implementation fees, credits, and proration create messy balances fast.

According to Allianz Trade's article citing a 2025 Deloitte survey, 62% of SaaS firms struggle to align AR aging with ASC 606, inflating DSO by 15-20% because of proration errors on multi-year contracts.

That matters in diligence. If your aging report doesn't clearly separate collectible billed amounts from deferred or misclassified revenue components, your financials won't hold up under investor scrutiny.

Agencies and services firms need client-level discipline

Agencies usually don't fail because they lack invoicing software. They fail because invoice disputes start upstream.

Aging reports in agencies often reveal:

- Scope creep that never got approved

- Project invoices sent without the right backup

- Retainers that are current while project overages sit unpaid

- Client concentration in overdue buckets

When you see repeated lateness from the same account, don't treat it as isolated AR noise. Review statement of work language, approval flow, and who owns collection conversations.

Build better reporting in your systems

In QuickBooks Online, use the Accounts Receivable Aging Summary and customize buckets if you need a deeper delinquency view. In NetSuite, save a custom A/R aging report with filters by customer, entity, or currency. In either tool, the goal is the same. Make the report visible enough that your team acts on it weekly.

For businesses building a tighter short-term liquidity process, connect AR review to a 13-week cash flow forecast. That's where overdue invoices stop being accounting history and start affecting real operating decisions.

Why predictive AR matters now

Static aging tells you what is already late. Modern finance teams also want to know what is likely to become late.

If you're exploring the future of AI in finance, pay attention to how invoicing and risk scoring tools are evolving. The practical shift is simple. Instead of reacting once invoices hit older buckets, teams can flag payment-risk patterns earlier and adjust collection effort before balances slide.

That's especially useful in subscription businesses, where a delinquent account can distort both cash planning and customer health signals.

From Reactive Collections to Strategic Cash Management

When you use the aging report properly, collections stop being a back-office chore. They become a management system for liquidity, forecasting, and investor readiness.

That shift matters because old receivables don't just threaten cash. They distort planning. You hire too early, spend too aggressively, and walk into board meetings with numbers that look cleaner than they really are. A disciplined AR process fixes that by forcing you to measure what is collectible, not just what has been invoiced.

There is also a practical upside to getting this right with expert support. According to Jumpstart Partners, businesses that implement aging-driven workflows and automated reconciliations see an average 40% improvement in cash flow, with over $47,000 in financial errors detected and corrected, supported by a SOC 2 Type II security framework.

If your finance team is still reacting to late payments after they become painful, you're already behind. The goal is to move from chasing old invoices to controlling the cash conversion cycle.

For a broader view of that operating discipline, review accounts receivable management for growing businesses.

The companies that stay in control don't just close the books. They know which invoices are collectible, which accounts need escalation, and how that affects the next quarter's cash.

If you want help building an AR process that improves cash flow, talk to Jumpstart Partners. Their team works with SaaS, agencies, and services businesses to clean up receivables, tighten reporting, and produce investor-ready financials without adding full-time overhead.