Financial Operations

What is Working Capital Management? A Founder's Guide for 2026

What is working capital management? Discover key metrics & strategies to unlock cash flow & fuel sustainable business growth.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··18 min readAre your revenue goals on track, but your bank account is consistently tighter than you’d like? That isn’t just a cash flow problem; it’s a working capital problem. For founders of growing SaaS and service businesses, mastering working capital is the secret weapon to scaling without constantly chasing your next funding round or drawing on expensive credit.

Think of it as the financial lifeblood of your company—the actual cash you have on hand to hire people, run marketing campaigns, and keep the lights on. It’s what separates companies that fund growth from their own operations from those that must rely on expensive debt or equity.

This isn’t a niche concern; it’s a top priority for finance leaders. Driven by economic pressures, The Hackett Group's 2026 Key Issues Study ranked working capital optimization as the No. 1 finance objective for the year. European firms alone have a staggering €1.4 trillion tied up in excess working capital, highlighting the massive opportunity for businesses like yours to unlock cash. You can see the full findings in their 2025 Europe Working Capital Survey.

Let's break down what working capital is and how you can manage it to fuel your company's growth.

Your Hidden Growth Engine: Why Working Capital Matters

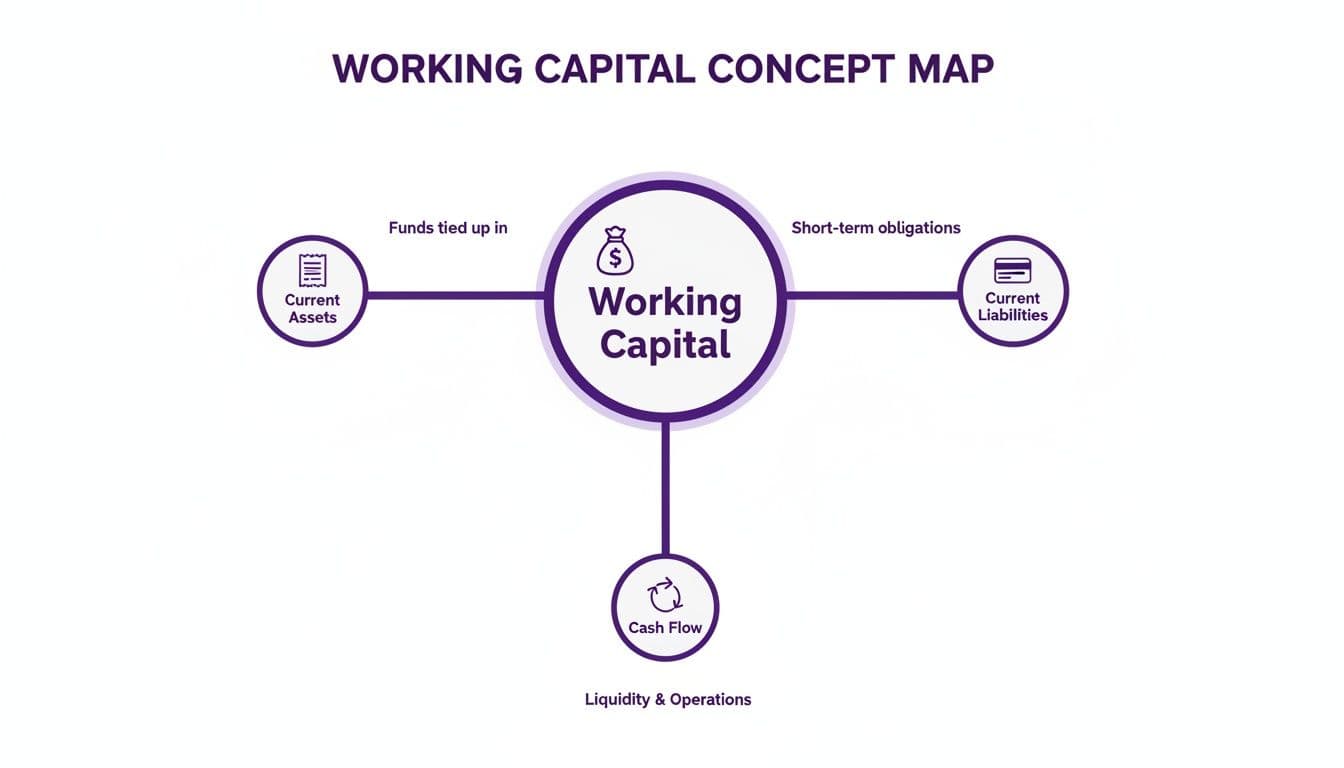

Working capital management is the process of strategically managing your short-term assets and liabilities to ensure your business has enough cash for its day-to-day operations. It's the engine that turns revenue on your P&L into real, usable cash to pay salaries, fund growth, and jump on opportunities.

Working Capital At A Glance

Here’s a quick summary of the core concepts and their direct impact on your business.

| Component | What It Means For You | Why It Matters To Your Growth |

|---|---|---|

| Current Assets | What you own that will become cash within a year (cash, client invoices, unbilled work). | The faster you turn these into cash, the more fuel you have for growth initiatives. |

| Current Liabilities | What you owe in the short term (vendor bills, payroll, short-term debt). | Stretching these payments smartly (without damaging relationships) keeps cash in your bank. |

| Working Capital | The difference between your current assets and current liabilities. | A positive number means you can cover your short-term bills. A negative number is a major red flag for most service businesses. |

Ultimately, a well-oiled working capital machine means you're not just profitable—you're cash-rich and ready to scale.

The Core Components of Working Capital

Managing working capital comes down to actively juggling three key areas of your balance sheet:

-

Current Assets: These are resources you expect to convert into cash within one year. This includes cash in the bank, accounts receivable (money your clients owe you), and for service firms, unbilled work-in-progress.

-

Current Liabilities: These are your short-term financial obligations due within one year. This includes accounts payable (money you owe to vendors and suppliers), payroll, and upcoming debt payments.

The goal is to strike the right balance: accelerate your cash inflows (getting paid faster) while strategically managing your outflows (paying your bills). If you get this wrong, even a profitable company can find itself completely cash-poor, paralyzing its ability to grow.

"A lot of business owners are cash-flow illiterate. They see a profit on their P&L and think they're fine, but they don't understand that profit is an opinion, and cash is a fact." - An expert on small business finance

This distinction is absolutely critical. While profit is an accounting measurement, working capital is the operational cash you can actually spend. For a deeper dive into this, check out our guide on cash flow management for small businesses.

The Three Levers Of Your Cash Conversion Cycle

To master working capital, you need to know which dials to turn. These aren't just abstract accounting terms; they're the three core drivers that control how quickly your business activities turn into actual cash in the bank. Think of them as the control panel for your company’s financial engine.

These three levers are:

- Days Sales Outstanding (DSO): How fast you collect cash from customers.

- Days Inventory Outstanding (DIO): How long your cash is tied up in unbilled work.

- Days Payable Outstanding (DPO): How long you take to pay your own bills.

Together, these metrics make up your Cash Conversion Cycle (CCC)—the total time it takes for a dollar you invest in your operations to make its way back into your pocket as cash. Let's break down each one with real-world examples for a SaaS company and a digital agency.

Lever 1: Days Sales Outstanding (DSO)

DSO answers a simple, critical question: How fast do you get paid? It measures the average number of days it takes to collect payment after you send an invoice. A high DSO means your hard-earned cash is sitting in your customers' bank accounts, not yours.

The formula is: (Accounts Receivable / Total Credit Sales) * Number of Days in Period

Let’s look at a digital agency with $50,000 in outstanding invoices (Accounts Receivable) and quarterly credit sales of $150,000 over a 90-day period.

- Calculation: ($50,000 / $150,000) * 90 Days = 30 Days DSO

This means it takes the agency an average of 30 days to get paid after invoicing. A DSO under 45 days is a strong sign of an effective collections process. But if that number creeps up to 60 or even 90 days, it puts immense strain on your cash flow, forcing you to use credit or dip into reserves just to make payroll.

If you're struggling to keep DSO low, our guide on what is accounts receivable management offers strategies you can use right away.

Lever 2: Days Inventory Outstanding (DIO)

For a SaaS or service business, "inventory" isn't what's in a warehouse. It's the value of your unbilled work-in-progress (WIP) or the costs you incur to deliver your service before you can bill for it. DIO tells you how many days your cash is locked up in work that you haven't invoiced yet.

The formula is: (Average Inventory Cost / Cost of Goods Sold) * 365 Days

Let's take a SaaS company. It has no physical products, but it has costs to serve customers (like hosting and support staff) before their monthly subscription fee is billed. If its annual Cost of Goods Sold (COGS) is $1.2M and its average "inventory" (unbilled service costs) is $100,000, the DIO looks like this:

- Calculation: ($100,000 / $1,200,000) * 365 Days = 30.4 Days DIO

This means cash is tied up for about a month before the company can even begin the billing process. For agencies, this number often represents work done in one month that won't be invoiced until the next. Keeping DIO as low as possible is crucial.

This visual shows how working capital is the connective tissue between your assets, liabilities, and ultimately, your operational cash flow.

The key takeaway? These components are all linked. A change in one directly impacts the others and your company’s overall financial health.

Lever 3: Days Payable Outstanding (DPO)

DPO measures how long you take to pay your own suppliers and vendors. Unlike DSO and DIO, a higher DPO is often a good thing—within reason. By strategically extending your payment terms, you’re effectively using your suppliers’ money to fund your own operations.

The formula is: (Accounts Payable / Cost of Goods Sold) * 365 Days

Let's go back to our SaaS company with a $1.2M COGS. If it currently has $150,000 in Accounts Payable (bills from vendors like AWS, marketing software, etc.), its DPO is:

- Calculation: ($150,000 / $1,200,000) * 365 Days = 45.6 Days DPO

This means the company is getting an average of 46 days of interest-free financing from its suppliers. That's a powerful source of working capital.

"Working capital is often the cheapest funding source available to a business. By optimizing payment cycles with suppliers and customers, companies can fund their own growth without resorting to debt or equity." – CFO of a high-growth tech firm

But there’s a fine line to walk. Pushing your DPO too high can damage your relationships with vendors, which can lead to them imposing stricter payment terms or, in the worst case, refusing to work with you. The goal is optimization, not exploitation.

Calculating and Benchmarking Your Cash Conversion Cycle

Now that you’ve got a handle on the three levers—DSO, DIO, and DPO—it’s time to put them together. The Cash Conversion Cycle (CCC) is the ultimate scorecard for your working capital. It tells you, in days, exactly how long it takes for the cash you invest in your operations to cycle back into your bank account.

The goal is always a lower number. A short CCC means you have an efficient, self-funding business that needs less outside cash to run and grow.

How to Calculate Your CCC

The formula is surprisingly simple, pulling together the three metrics we’ve just covered.

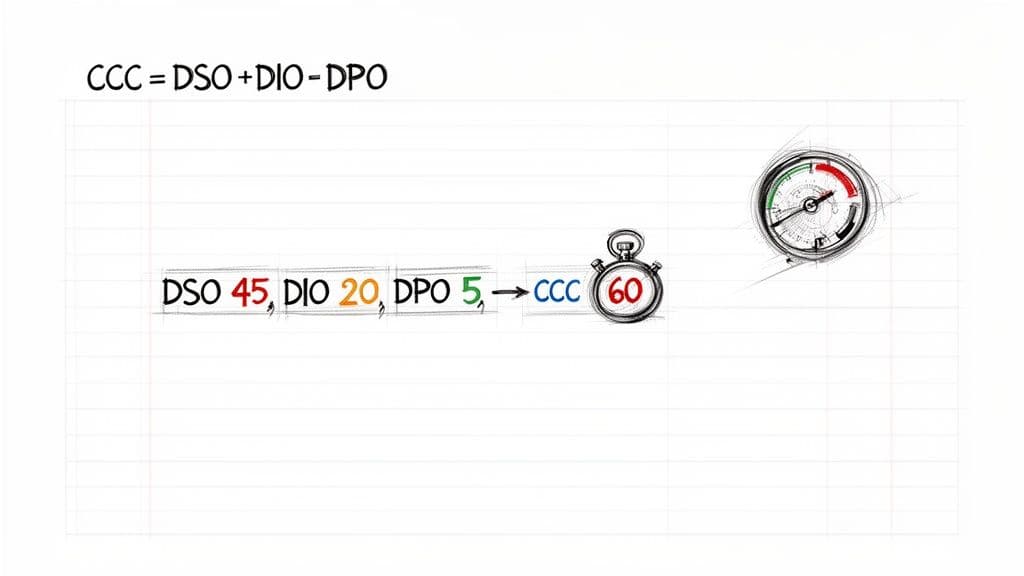

CCC = Days Sales Outstanding (DSO) + Days Inventory Outstanding (DIO) - Days Payable Outstanding (DPO)

Let’s run the numbers for a real-world scenario: a $5M ARR SaaS company. We’ll use the figures from our earlier examples to see what they tell us about the company’s financial heartbeat.

- DSO: 30 Days (It takes a month to get paid by customers)

- DIO: 30.4 Days (Cash is tied up delivering the service for about a month before it can be billed)

- DPO: 45.6 Days (The company is getting about 46 days of free financing from its vendors)

Plugging these into the CCC formula gives us:

CCC = 30 Days (DSO) + 30.4 Days (DIO) - 45.6 Days (DPO) = 14.8 Days

This is an excellent result. It means this SaaS company has a cash gap of only 15 days. For just two weeks, the business has to fund its own operations—like payroll and software subscriptions—before cash from customer payments replenishes the account. A cycle this short makes a business incredibly resilient and scalable.

Getting this number is the first step in diagnosing your cash flow health, a skill you can build on by learning how to read a cash flow statement.

Benchmarking Your Performance Against The Industry

Knowing your CCC is one thing. Knowing how it stacks up against the competition is where the real power lies. This context tells you whether your 15-day CCC is truly world-class or just average for your industry.

Broader market trends show working capital is getting squeezed. Recent analysis from KPMG reveals the average cash conversion cycle for US public companies is climbing, from 83 days in 2021 to a projected 89 days in 2025.

But for your business, industry-specific benchmarks are what matter.

SaaS And Agency Working Capital Benchmarks (2026)

Compare your key working capital metrics against these industry standards from OpenView's 2024 SaaS Benchmarks and our own proprietary data for agencies to identify your strengths and weaknesses.

| Metric | SaaS (Median) | Digital Agency (Median) | Top Quartile Goal |

|---|---|---|---|

| DSO | 55 Days | 48 Days | < 30 Days |

| CCC | 65 Days | 40 Days | < 20 Days |

Source: OpenView 2024 SaaS Benchmarks & Jumpstart Partners proprietary data

Looking at this table, our example SaaS company's CCC of 15 days is easily in the top quartile—a clear sign of exceptional financial management. An agency with a 60-day CCC, on the other hand, is lagging behind. This isn't just a number; it's a bright red flag pointing to a clear opportunity to overhaul its invoicing and collections process. Use these benchmarks to set aggressive but realistic targets for your own operations.

Actionable Strategies To Optimize Your Working Capital

Knowing your numbers is the diagnosis. Now it’s time to write the prescription. Here is a playbook of battle-tested strategies to pull the three main levers of working capital. These are practical moves you can make today to unlock cash, fund growth from your own operations, and build a more resilient business.

| Strategy | Goal | Actionable Next Steps |

|---|---|---|

| Shorten Your DSO | Get paid faster | 1. Automate Invoicing & Reminders: Use your accounting software to send invoices and follow-ups automatically. 2. Offer Early Payment Discounts: Use "2/10, net 30" terms to incentivize quick payment. 3. Establish a Collections Process: Create a clear escalation path for overdue invoices (email -> personal email -> phone call). |

| Optimize Your DPO | Keep cash longer | 1. Negotiate Better Terms: Ask new vendors for Net 45 or Net 60 terms from the start. 2. Use a Corporate Card: Pay vendors with a card to get an extra 30-day float before the cash leaves your bank. 3. Schedule Payments for the Due Date: Use AP automation to pay bills exactly on time, not early. |

| Reduce WIP/DIO | Bill for work sooner | 1. Bill Upfront: For retainers and subscriptions, invoice at the beginning of the service period, not the end. 2. Use Milestone Billing: For large projects, bill upon completion of key phases (e.g., 25% at kickoff, 50% at midpoint). 3. Require Deposits: Secure a deposit before starting any new project work. |

These aren't just niche strategies; they're a global trend. According to Visa's 2025-2026 Growth Corporates Working Capital Index, 81% of CFOs now use working capital solutions, and 68% of high-growth firms are using it to fund growth.

By applying these targeted strategies, you move from passively watching metrics to actively shaping your company’s financial destiny. For a deeper dive, check out our guide on how to improve working capital.

Common Working Capital Pitfalls And Red Flags

Smart working capital management is as much about dodging bullets as it is about hitting targets. Recognizing the warning signs early is how you spot a weakness in your financial operations before it turns into a full-blown crisis.

The Myth of Revenue Equaling Cash

This is the single most dangerous misconception for founders: believing that strong revenue growth automatically means a healthy bank balance. It doesn't. You can close a record-breaking quarter, but if your clients take 90 days to pay, you won’t have the cash to make payroll next month. This is the gap where working capital problems are born—smack in the middle of booked revenue and actual cash.

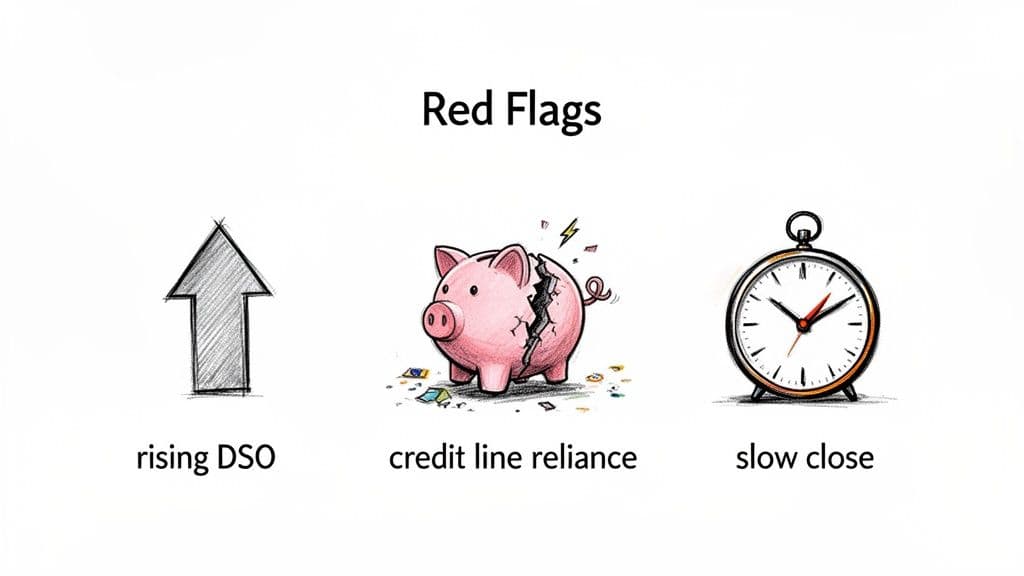

A Checklist of Working Capital Red Flags

Do any of these sound familiar? If you answer "yes" to even one, it’s time for a deep dive into your financial operations.

-

Your DSO is climbing quarter-over-quarter. This is the #1 signal that your collections process is broken. A DSO creeping from 35 to 50 days means your cash is sitting in your clients' bank accounts instead of yours.

-

You rely on a credit line to make payroll. Using debt for predictable operational expenses like payroll is a symptom of a systemic cash flow problem, not a one-off tight month. It means your cash conversion cycle is dangerously long.

-

It takes weeks to close the books. A slow month-end close means you’re making critical decisions with outdated information. Top-performing finance teams close their books in five days. Period.

-

You aggressively stretch vendor payments. While optimizing DPO is a valid strategy, pushing it too far torches relationships. If vendors start demanding upfront payment or cutting you off, you've destroyed a valuable source of short-term financing.

-

You don’t have a 13-week cash flow forecast. Without a rolling forecast, you're flying blind. You have zero visibility into upcoming cash shortfalls and no time to proactively adjust spending or chase down receivables.

Operational issues can also sideswipe you. Proactively managing common platform issues, like avoiding Shopify holds, is crucial for preventing major disruptions to your cash inflows.

When to Get Expert Help With Your Financial Operations

As a founder, you wear every hat. But there comes a point where wearing the "finance hat" goes from a necessary chore to a strategic liability. Chasing down invoices and wrestling with spreadsheets isn't just a distraction—it's a high-risk activity when your company starts to scale. The question isn't if you'll need expert financial help, but when.

The Triggers That Signal It's Time For a Change

If you find yourself nodding along to any of these scenarios, your current financial operations aren't just slowing you down; they're actively holding your business back.

-

You're Preparing for a Fundraise: Investors demand pristine, accurate, and defensible financials. A messy P&L or an un-reconciled balance sheet is the fastest way to get a "no." An expert partner ensures you're "due diligence ready" at all times.

-

Your Month-End Close is Slow and Painful: If it takes more than a week to close your books, you're making decisions based on old news. This is a symptom of broken processes and manual work.

-

You Lack a Reliable Cash Flow Forecast: Making confident decisions about hiring or marketing spend without a forward-looking cash forecast is like driving at night with the headlights off. A 13-week cash flow forecast is the absolute minimum you need.

These aren't just minor inconveniences. They are strategic disadvantages that prevent you from seeing opportunities, mitigating risks, and using your financials as a tool to drive strategy.

The Strategic Advantage of an Outsourced Finance Partner

Bringing on an outsourced finance team isn't about offloading bookkeeping. It’s about gaining a strategic partner who installs a professional-grade finance function into your business—delivering a level of insight and control that’s impossible to achieve with a part-time bookkeeper or a junior accountant.

"Many founders believe that a strong product and sales team are enough. But without a robust financial engine to manage working capital and provide clear insights, growth is unsustainable. It's like trying to win a race with a flat tire." – Matt Wolf, Head of Finance at Jumpstart Partners

A dedicated partner moves your finance function from reactive fire-fighting to proactive, strategic management, helping you implement critical systems like ASC 606 revenue recognition and delivering investor-ready financials.

For founders who are ready to scale, it’s crucial to understand the different levels of outsourced financial support. To learn more about how a finance partner provides this level of strategic guidance, explore the role of a fractional CFO for startups in our detailed guide.

If these challenges sound painfully familiar, it's time to stop managing your finances from the rearview mirror. Your next stage of growth depends on transforming your finance function from an administrative burden into your most powerful strategic weapon.

Frequently Asked Questions About Working Capital

We've walked through the mechanics of managing working capital. Here are the common questions we hear from founders and finance leaders as they start turning these concepts into action.

What Is a Good Cash Conversion Cycle?

The right question is, "What is a good CCC for my industry?" A median CCC for SaaS companies hovers around 65 days, while for digital agencies it’s closer to 40 days. Top-quartile performers in both industries get this number below 20 days. If your CCC is high for your sector, don't panic. Recognize it as a massive, flashing sign that there’s cash trapped in your operations waiting to be released.

Can a Business Have Negative Working Capital and Still Be Healthy?

Yes, and for some business models, it's the holy grail. Negative working capital happens when your current liabilities are greater than your current assets, common in businesses that collect cash from customers long before they have to pay their suppliers (e.g., annual SaaS subscriptions). For example, a customer pays a $12,000 annual fee on January 1st. You have the cash, but you also have a huge liability (unearned revenue) to work off over 12 months. This creates negative working capital while being incredibly cash-flow positive. The danger? This model depends on a constant flow of new sales. If growth stalls, you won't have the new cash coming in to cover the operational costs of serving existing customers.

How Often Should I Review My Working Capital Metrics?

You need a steady rhythm for reviewing your working capital. A two-tiered approach is best.

-

Weekly Pulse Check: A non-negotiable, quick look at your core cash drivers: current cash balance, accounts receivable aging, and accounts payable aging. This is about having a real-time feel for your liquidity. No surprises.

-

Monthly Deep Dive: During your month-end close, calculate and track trends for your core KPIs—DSO, DPO, and CCC. You’re comparing this month to last month and the same month last year, looking for patterns and identifying the specific levers you need to pull.

If you're tired of wrestling with spreadsheets and ready for investor-ready financials that give you this level of clarity, Jumpstart Partners can help. Our team of US-based, CPA-certified experts delivers a fast 5-day month-end close and the cash flow visibility you need to make confident decisions.

Book a free consultation today to see how we can transform your finance function into a strategic advantage.