Financial Operations

How to Read a Cash Flow Statement Like a CEO: A Founder's Guide

Learn how to read a cash flow statement to understand your business's true financial health. An essential guide for founders to make smarter decisions.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··21 min readAs a founder or CEO, you're judged on growth and profitability, but you survive on cash. The most common—and dangerous—financial mistake is treating your Profit & Loss (P&L) statement as a proxy for your bank balance. It’s not. In fact, profitable companies go bankrupt with alarming frequency simply because they run out of real money.

Your P&L tracks an accounting concept; the cash flow statement tells you what’s actually in the bank to pay bills, make payroll, and fund growth. Getting this wrong is the difference between survival and failure.

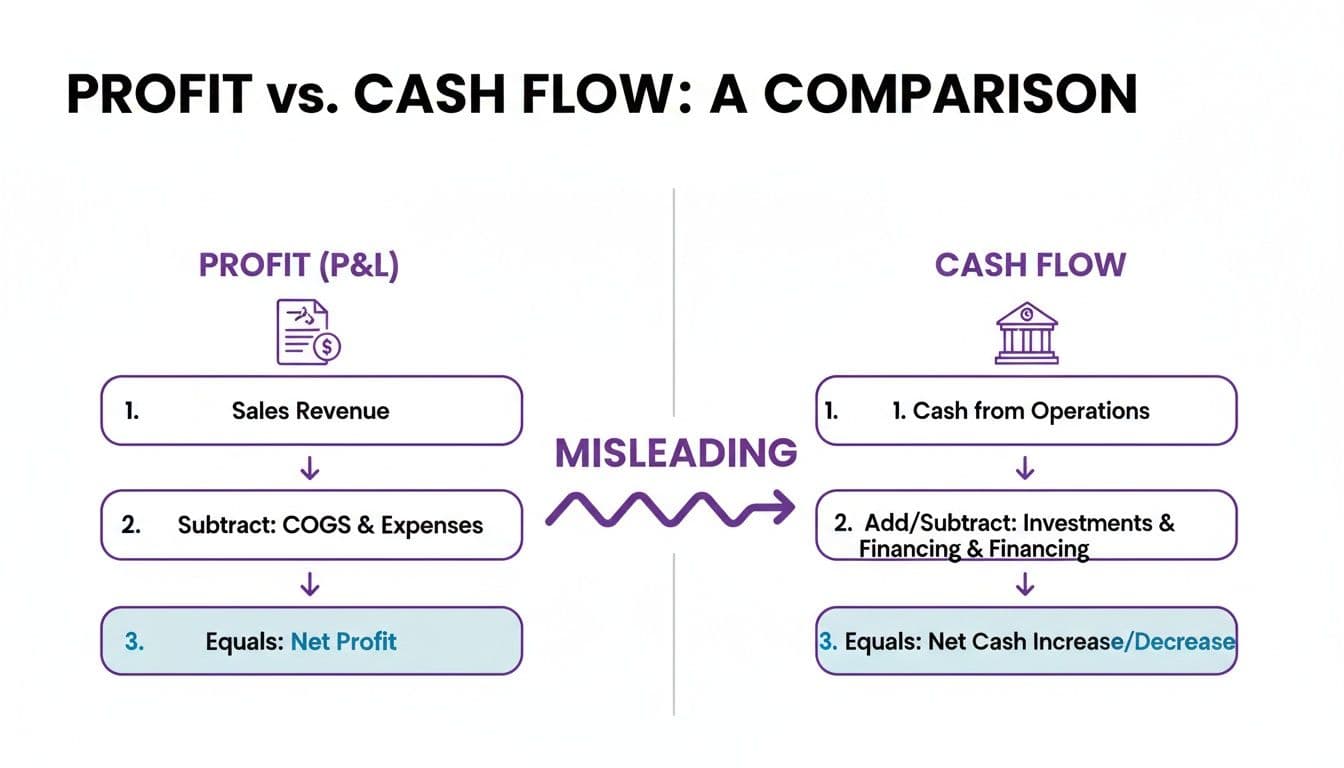

Why Your P&L Is a Misleading Indicator of Cash

The disconnect between profit and cash comes from accrual accounting, the method that powers your P&L. Accrual accounting recognizes revenue when it's earned, not when cash is collected. It also records expenses when they are incurred, not when they are paid.

This creates timing gaps that can paint a dangerously optimistic picture of your company's health. You can learn more about the specifics in our guide to P&L management.

For SaaS and professional services firms, this problem is especially pronounced. Think about these scenarios:

- SaaS Revenue Recognition: You sign a $120,000 annual contract and collect the cash upfront. Your cash flow statement shows a massive inflow, but your P&L can only recognize $10,000 in revenue each month.

- Long Collection Cycles: Your digital agency books a $50,000 project. Your P&L shows a profitable engagement, but if the client pays on Net 60 or Net 90 terms, your bank account remains empty for months.

- Upfront Costs: You spend $20,000 in customer acquisition costs (CAC) to land a new client. That cash is gone today, but the corresponding revenue trickles in over the next 12-24 months.

These examples show exactly why relying on your P&L is a strategic error. Before we dive deeper, let's make the distinction crystal clear.

Profit vs. Cash: The Critical Differences

The biggest mistake founders make is treating all revenue equally. A dollar of recognized revenue on the P&L isn't the same as a dollar of cash in the bank. This table breaks down the fundamental differences between what your P&L shows and what your Cash Flow Statement reveals.

| Concept | Profit & Loss (P&L) View | Cash Flow Statement (CFS) View |

|---|---|---|

| Revenue | Shows revenue when earned (e.g., work completed, service delivered) | Shows cash when collected from customers |

| Expenses | Shows expenses when incurred (e.g., received a vendor bill) | Shows cash when paid to vendors, employees, or lenders |

| Non-Cash Items | Includes non-cash charges like depreciation and amortization | Excludes non-cash charges; they don't affect your bank balance |

| Capital Expenditures | Asset purchases (e.g., equipment) are capitalized, not expensed | Shows the full cash outflow when the asset is purchased |

| Financing & Investing | Loan principal payments and owner draws do not appear on the P&L | Shows cash inflows from loans and outflows for repayments |

| Core Question | "Is my business model profitable?" | "Do I have enough cash to operate?" |

Ultimately, your P&L measures an accounting concept; your cash flow statement tracks the fuel your business actually burns to operate.

"A profitable business can easily run out of cash. Revenue is recognized on the P&L, but if you haven’t collected it, you can’t spend it. The cash flow statement bridges that gap and shows you the real story." - Tony Molina, CPA, Founder of Jumpstart Partners

Mastering your cash flow statement isn’t just a task for your finance team. It's your primary tool for strategic leadership, enabling you to see past accounting profits and manage the lifeblood of your business—cash. Without this clarity, you're flying blind.

Decoding Cash From Operations: Your Business Engine

If your business can't generate consistent cash from its core operations, you don’t have a sustainable model. This is where you move beyond the accounting theory of the P&L and get to the ground truth of your company's health—the Cash from Operations (CFO) section of your cash flow statement.

CFO is the single most important measure of your business's viability. It tells you if your primary activities—selling software, providing services, managing projects—are actually producing the cash needed to pay salaries, fund marketing, and keep the lights on. It’s the engine of your business.

This infographic shows the dangerous disconnect between accounting profit and actual cash.

The key takeaway is that relying on profit alone is misleading. We'll focus on the indirect method for calculating CFO, which is the standard for virtually all private companies because it clearly reconciles net income to cash.

From Net Income to True Cash Flow

The indirect method starts with Net Income from your P&L and then systematically adjusts it for two main categories: non-cash items and changes in working capital. This process strips out the accrual-based assumptions to arrive at the actual cash impact.

- Non-Cash Expenses: These are expenses on your P&L that didn't involve an actual cash outlay. The most common is Depreciation and Amortization. You add these back to net income because, while they reduced your profit, they didn't drain your bank account.

- Changes in Working Capital: This is where the real story unfolds. Working capital accounts—like Accounts Receivable, Accounts Payable, and Deferred Revenue—represent the timing gap between booking a transaction and seeing the cash.

Understanding the dynamics of receivables and payables is crucial to accurately interpreting your operating cash flow. You can learn more about how to Master Your Cash Flow with Receivables and Payables.

SaaS Company Worked Example

Let’s walk through a practical example for a SaaS company with $100,000 in Net Income for the quarter. You'll quickly see how a "profitable" company can have less cash than its P&L suggests.

| Line Item | Amount | Impact on Cash |

|---|---|---|

| Net Income | $100,000 | Starting Point (from P&L) |

| Add: Depreciation | +$15,000 | A non-cash expense is added back. |

| Subtract: Increase in Accounts Receivable | -$40,000 | You booked new sales, but customers haven't paid yet. This is revenue without the cash. |

| Add: Increase in Accounts Payable | +$10,000 | You received vendor bills but haven't paid them, preserving your cash for now. |

| Add: Increase in Deferred Revenue | +$25,000 | You collected cash upfront for annual subscriptions but haven't recognized it as revenue yet. A huge cash boost. |

| Cash from Operations (CFO) | $110,000 | Actual cash generated from core business. |

In this case, your CFO of $110,000 is higher than your net income. The cash injection from deferred revenue was partially offset by a significant increase in accounts receivable. This reconciliation is vital; without it, you'd only see the $100,000 profit and miss the underlying cash movements.

For a deeper dive into the nuances of this metric, you can explore our complete guide on what is operating cash flow.

Red Flags in Your Operating Cash Flow

Your CFO section is a goldmine for spotting operational problems before they become crises. You just need to know what to look for.

| Red Flag | What It Looks Like | Why It's a Problem |

|---|---|---|

| Growing Profit, Shrinking Cash | Net Income is rising quarter-over-quarter, but Cash from Operations is flat or declining. | This is the classic warning sign. It means you're aggressively booking sales (increasing Accounts Receivable) but struggling to collect cash. Your growth is an illusion. |

| Surging Accounts Receivable | Your A/R balance grows faster than your revenue (e.g., A/R up 30% YoY, but revenue only up 15%). | This signals a serious collections problem or overly generous payment terms. Each dollar tied up in A/R is a dollar drained from your operating cash. |

| Heavy Reliance on Stretching Payables | A consistent, significant increase in Accounts Payable is a major contributor to your operating cash flow. | You're using your vendors as a line of credit. While it can be a short-term tactic to preserve cash, it's unsustainable and damages critical supplier relationships. |

For SaaS companies, the Operating Cash Flow (OCF) Margin is a critical benchmark. It’s calculated as (Cash From Operations / Revenue). According to the 2024 OpenView SaaS Benchmarks, top-quartile companies boast OCF margins of 20% or more, while the median sits around 5%. If your margin is consistently negative, your business model is fundamentally leaking cash.

Analyzing Investing Activities: Where You Place Your Bets

If the operating section shows the health of your business engine, the investing section reveals where you’re pointing that firepower. It answers the one question every founder has to get right: Are your investments fueling sustainable growth, or are you just burning cash?

This is where your capital allocation strategy gets real. The numbers here track the cash you spend buying or selling long-term assets. For a SaaS, agency, or service firm, the story is more about your bets on the future.

Decoding Your Capital Expenditures (CapEx)

The most common cash outflow you'll see here is for Capital Expenditures (CapEx). These are your big-ticket purchases for physical assets expected to provide value for more than one year.

For a tech or service business, this usually means:

- Hardware and Equipment: New servers, high-performance laptops for your dev team, or video gear for your agency's content studio.

- Office Build-Outs: Investing in a new office or renovating your current space.

But here’s a line item that trips up many founders: capitalized software development costs. When you spend engineering hours building a new platform or feature that will generate future revenue, accounting rules allow you to treat those payroll costs as an asset rather than an immediate expense. That cash outflow shows up right here in the investing section, not in operations.

A Worked Example: The Digital Agency Investment

Let’s say your digital agency invests $75,000 in a new video production studio to launch a high-margin service offering. That same quarter, you sell off $10,000 worth of old office furniture after a downsizing.

| Investing Activity | Amount | Impact on Cash |

|---|---|---|

| Purchase of Video Equipment (CapEx) | -$75,000 | Direct cash outflow for a long-term asset. |

| Sale of Old Office Furniture | +$10,000 | Minor cash inflow from selling outdated assets. |

| Net Cash Used in Investing | -$65,000 | Total cash deployed for future growth. |

Seeing a negative -$65,000 here isn't a red flag on its own. For a scaling company, it’s a sign of healthy ambition. The real story comes from connecting this to the operating section—this investment needs to be funded by strong operating cash flow, not by draining your emergency fund or taking on bad debt.

Investing Red Flags to Watch For

A negative number here shows ambition. A chronically negative number without a corresponding lift in revenue or efficiency signals a problem. When you're learning how to read a cash flow statement, watch for these specific warning signs.

- High CapEx, Stagnant Growth: You’re consistently pouring cash into assets, but revenue isn’t budging. This is a classic symptom of inefficient capital allocation—a major red flag for investors who will immediately question your decision-making. Are you even measuring the return on these investments? To dig deeper, you can learn more about metrics like the asset turnover ratio.

- Selling Assets to Fund Operations: A positive cash flow from investing is rare, and it's usually a bad sign. If you’re selling off core assets to generate cash just to make payroll, your business model is fundamentally broken.

- Investing Outflows Exceeding Operating Inflows: This is a direct flight to a cash crunch. If your investments are consistently larger than the cash your core business generates, you're on an unsustainable path that will force you to raise dilutive capital or take on debt just to keep the lights on.

When you're prepping for fundraising, this section reveals whether your growth is real or just smoke and mirrors. You can discover more insights on how investors scrutinize these trends by watching this analysis of S&P 500 firms.

Understanding Financing Activities: How You Fuel Growth

If operating activities show whether your core business can sustain itself and investing activities show your bets on the future, then the financing section is your company’s funding scorecard. It answers a blunt question: where is the external cash coming from to fuel your growth?

This part of your cash flow statement tracks every dollar exchanged with your owners and lenders. It's where you see the real cash impact of raising a funding round, taking on debt, or paying it back. Getting this right is how you capitalize the business without losing control or taking on obligations you can't sustain.

Common Financing Inflows and Outflows

For any CEO of a growing business, the financing section is a log of how you're using other people's money. Here are the most common transactions you'll see:

- Issuance of Stock: When you close a funding round (Seed, Series A, etc.), the cash injection from investors appears here as a positive inflow.

- Proceeds from Debt: This is cash you receive from a bank loan, a line of credit, or venture debt. It’s a cash inflow.

- Repayment of Debt: As you make principal payments on your loans, the cash leaving your bank account shows up here as an outflow. Note: Interest payments are almost always found in the operating section.

- Payment of Dividends or Owner Draws: If you distribute profits to shareholders or owners, that cash outflow is a financing activity.

- Share Repurchases: Buying back stock from investors or employees is also a cash outflow.

Every single one of these transactions involves a strategic trade-off. A big cash inflow from issuing stock pads your bank account but dilutes ownership. An inflow from debt adds firepower without dilution, but it comes with interest payments and covenants that can restrict your decisions.

A Worked Example of Financing Activities

Let’s imagine your digital agency secures a $200,000 term loan to fund an expansion. In the same period, you also make a quarterly $15,000 principal payment on an existing loan.

| Financing Activity | Amount | Impact on Cash |

|---|---|---|

| Proceeds from New Term Loan | +$200,000 | Inflow of cash to be used for strategic growth. |

| Repayment of Existing Loan (Principal) | -$15,000 | Outflow of cash to reduce long-term debt. |

| Net Cash from Financing Activities | +$185,000 | Total net cash gained from funding decisions. |

This positive $185,000 shows you’ve successfully brought in new capital. When an investor scans this, their eyes immediately jump to the investing section. They want to see if this cash was put toward a smart growth initiative, like acquiring a smaller competitor. You can learn more about how this capital can be deployed by reading our guide on what is growth capital.

Red Flags in Your Financing Activities

More than any other section, this is where VCs and lenders look for signs of desperation. While external capital is essential for scaling, a company that constantly relies on it just to survive is on a dangerous path.

"When we're doing due diligence, the financing section tells us a story about a company's dependency. We want to see financing cash used for disciplined, strategic investments—not to plug holes in a leaky operational boat." - Seasoned VC Investor

The biggest red flag of all is consistently positive cash from financing used to cover negative cash from operations. It means you're raising money or taking on debt just to make payroll and keep the lights on. This is a classic symptom of a broken business model. You can explore more about these financial statement trends and their implications in this CFO Selections analysis.

Your Cash Flow Playbook: From Insight to Action

Knowing how to read a cash flow statement is one thing. Acting on it is everything. A financial statement sitting in a folder is useless; the real value comes when you turn those numbers into decisions that protect and grow your cash.

This is how you shift from being a founder who’s constantly reacting to cash crunches to a leader who’s strategically steering the ship. It’s about implementing a few key disciplines that give you control over your company's financial future.

The first and most important step is to stop looking backward and start looking forward.

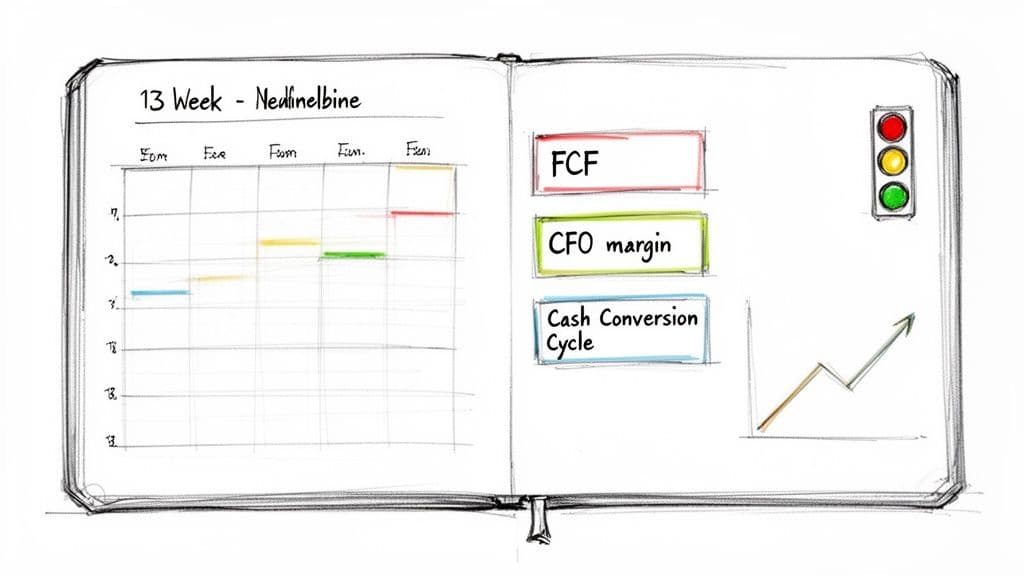

Action Item 1: Build a 13-Week Cash Flow Forecast

A 13-week cash flow forecast is the single most powerful tool for managing liquidity. A quarter is the perfect timeframe—long enough to spot meaningful trends and short enough to act on them decisively. It's non-negotiable for making confident calls on hiring, spending, and investment.

This isn’t some massive, complex model. It’s a simple, rolling weekly projection of cash coming in and cash going out.

- Start with your opening cash balance. What’s actually in the bank today?

- Project your weekly cash inflows. This includes all customer payments you realistically expect to collect. Base your projections on your actual collection cycles and be conservative.

- List all your weekly cash outflows. Get everything down: payroll, rent, software bills, vendor payments, loan repayments, and taxes. Don't forget the one-off expenses that always pop up.

- Calculate your net cash flow each week (Inflows - Outflows) and project your ending cash balance for the next 13 weeks.

This exercise forces you to confront the reality of your cash cycle. It will immediately spotlight future shortfalls, giving you weeks—not days—to find a solution. To get started, you can use our proven cash flow statement template in Excel to build out your forecast.

Action Item 2: Bust the “Healthy Bank Balance” Myth

One of the most dangerous traps for a founder is seeing a big number in the company bank account and assuming the business is healthy. It's a classic misconception. A large cash balance can easily mask deep operational problems that are about to blow up.

Imagine this scenario:

- You just collected $250,000 from two enterprise clients who paid their annual contracts upfront. The bank account looks fantastic.

- But your 13-week forecast shows that after two payroll cycles and a huge vendor bill, that balance is going to drop off a cliff.

- At the same time, your cash from operations has been negative for two straight months because new sales have slowed and your other clients are paying late.

That $250,000 isn't profit; it's a liability (deferred revenue) you have to service for the next 12 months. Without a forecast, you might approve a major new hire or a big marketing spend, only to face a cash crisis in 60 days.

"A healthy bank balance is the most misleading metric in your business. It tells you nothing about future obligations or the underlying health of your operations. True financial visibility comes from a forward-looking forecast, not a historical bank statement." - Jumpstart Financial Expert

Action Item 3: Create a Weekly Cash Flow Dashboard

To stay in control, you need a simple dashboard with a handful of critical metrics. Don't drown yourself in data. Track these three numbers weekly to know exactly where you stand.

-

Free Cash Flow (FCF): This is your Cash from Operations - Capital Expenditures. It’s the cash left over to repay debt, pay dividends, or reinvest in the business after you’ve funded both operations and long-term investments. This is your true "discretionary" cash.

-

Cash Conversion Cycle (CCC): Calculated as Days Inventory Outstanding + Days Sales Outstanding - Days Payables Outstanding, this metric measures how long it takes to turn your investments in resources back into cash. For SaaS and service firms, it's primarily DSO - DPO. A shorter cycle means you get your cash faster.

-

Operating Cash Flow Margin: This is your (Cash from Operations / Revenue) x 100. It shows how much cash you generate for every dollar of revenue. According to OpenView's 2024 SaaS Benchmarks, a 20%+ margin is considered best-in-class for established SaaS companies.

Analyzing these metrics turns your cash flow statement from a static, historical document into a dynamic management tool. It moves the conversation from "what happened?" to "what are we going to do next?"

From Fire-Fighting to Proactive Strategy

Reading a cash flow statement is the first step. Building forecasts and tracking metrics is the next. But truly mastering your cash requires a system that delivers real-time, investor-grade financials every month—not just once a quarter when you're preparing for a board meeting.

This is where many founders hit a wall. You're busy running the business, not reconciling accounts. This financial chaos—fueled by delayed reporting and inaccurate data—leads to constant fire-fighting. You're scrambling to make payroll or putting key hires on ice because you just don't have confidence in the numbers.

At Jumpstart, we deliver the real-time visibility you need to lead with confidence. Our team of US-based, CPA-certified experts delivers a fast 5-day month-end close and a 13-week cash flow forecast, so you’re always ahead of the curve. We move you from fighting fires to making proactive, strategic decisions.

If you’re ready to gain full control over your cash flow and build a more resilient business, book a free consultation with our finance experts today.

Common Cash Flow Statement Questions, Answered

Even after you know the basics, the cash flow statement can be tricky. Here are the questions that trip up founders most often, with straight answers.

Why Isn't My Net Income the Same as My Cash Flow?

This is the big one. Profit is not cash. Your Profit & Loss statement runs on accrual accounting, meaning it records revenue when you earn it and expenses when you incur them—not when money actually changes hands. A client invoice boosts your profit today, but the cash flow statement only shows the money when the client actually pays. The cash flow statement is your reality check.

Which Is More Important: Operating, Investing, or Financing Cash Flow?

Cash from Operations (CFO) is the heart of your business. It's the undisputed champion. It tells you if your core business model—selling your product or service—is actually generating cash.

Consistently positive CFO is a sign of a healthy, sustainable company. Negative cash from investing is often a good thing (it means you’re buying assets for growth), and financing cash flow is just how you fund the business. But if your operating cash flow is chronically negative, you have a fundamental problem with your business model that no amount of fundraising can fix long-term.

What Is Free Cash Flow and Why Does It Matter So Much?

Free Cash Flow (FCF) is the cash your company generates after paying for everything it needs to support operations and maintain its assets. Think of it as the "true" profit.

The classic formula is: Cash from Operations - Capital Expenditures = Free Cash Flow

This is the money you have left over to pursue strategic moves—repay debt, hire a key executive, or acquire a competitor. It’s the ultimate metric for financial strength and flexibility, and it's the number investors and potential buyers obsess over.

"A profitable business can be cash-poor if it's not generating free cash flow. FCF is the true discretionary cash that leadership can use for strategic moves. It’s what separates a company that’s just surviving from one that’s built to win." - Jumpstart Financial Expert

For a deeper look into the nuts and bolts of putting one of these together, this guide on how to prepare a cash flow statement can be a useful resource.

Gaining control over your cash flow is the difference between reactive fire-fighting and proactive leadership. At Jumpstart Partners, we provide the real-time visibility you need to make confident, strategic decisions. Our experts deliver a 5-day month-end close and a forward-looking 13-week cash flow forecast, so you’re always ahead of the curve.

Book a free consultation with our finance experts today to see how we can help you build a more resilient and valuable business.