Financial Operations

What Is Inventory Accounting? a Founder's Guide to Profit

What is inventory accounting and how does it impact your profit and taxes? A guide for founders on FIFO, LIFO, costing methods, and financial reporting.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··17 min readMost founders think inventory accounting is a manufacturing problem. That's wrong. If you run a SaaS company that ships hardware, an agency that prepays media or software licenses, or an e-commerce brand carrying fast-moving SKUs, inventory accounting directly affects profit, cash flow, and how credible your numbers look to investors and lenders.

It also gets expensive fast. For businesses in the $500K to $20M revenue range, improper inventory capitalization and reconciliation can produce $47K+ in errors per client during audits, according to Harris & Ward's ASC 606 guide. That isn't bookkeeping trivia. That's margin leakage, bad pricing decisions, messy tax filings, and balance sheets you can't trust.

If you're asking what is inventory accounting, the practical answer is simple. It's the discipline of deciding what counts as inventory, what it costs, when it becomes an expense, and how those decisions flow into your financial statements.

Table of Contents

- Why Poor Inventory Accounting Is a Silent Profit Killer

- The Core Principles of Inventory Accounting

- Choosing Your Inventory Costing Method FIFO vs LIFO

- From Journal Entry to Financial Statement Impact

- Inventory Rules for SaaS E-commerce and Agencies

- Common Errors and Inventory Management Best Practices

- When to Outsource Your Inventory Accounting

Why Poor Inventory Accounting Is a Silent Profit Killer

Inventory isn't just product. It's cash that hasn't turned back into cash yet.

When you account for it badly, you overstate assets, understate expenses, distort gross margin, and make weak operating decisions with false confidence. Founders often think the issue is operational. It's financial first. If your inventory numbers are wrong, your pricing, profitability by SKU, and cash planning are wrong too.

"Founders think inventory is just stuff on a shelf. In reality, it's cash tied up in a warehouse. How you account for it determines your reported profit, your tax bill, and whether you can get that next round of funding."

That quote is blunt, and it should be. Investors don't reward enthusiasm. They reward numbers they can trust.

Where the damage shows up

| Business area | What bad inventory accounting does |

|---|---|

| Profitability | Hides unprofitable products or contracts because COGS isn't matched correctly |

| Cash flow | Encourages overbuying and leaves cash stranded in stock or prepaid assets |

| Tax | Pushes taxable income in the wrong direction because expenses are recognized at the wrong time |

| Valuation | Weakens diligence quality when buyers or investors see inconsistent gross margin logic |

A lot of founders obsess over top-line growth while ignoring the line that determines whether growth is worth funding. If your COGS is off, your gross margin is fiction. If you need a cleaner framework for that connection, start with this guide on how to calculate COGS.

The mistake I see most often

You treat inventory as an admin task delegated to operations, then expect finance to clean it up at month-end. That doesn't work. Inventory accounting is where operations and finance meet. If those teams don't agree on quantity, cost, and timing, your close will drag and your reporting will stay unreliable.

Practical rule: If inventory affects delivery, fulfillment, or client setup, it also affects your margin. Finance has to own the accounting logic, even if operations owns the physical process.

The Core Principles of Inventory Accounting

Inventory accounting starts with one formula, and if your team can't explain it clearly, your books aren't ready for scale.

The formula that drives gross profit

Beginning Inventory + Purchases – Ending Inventory = Cost of Goods Sold (COGS). Cornell's inventory accounting guidance uses a simple example: if inventory available for sale totals $6,400 and the closing inventory count is valued at $2,800, the resulting COGS is $3,600, which is then recognized on the income statement through expense recognition under Cornell's inventory accounting framework.

That single calculation determines how much cost stays on your balance sheet and how much moves into expense.

Here's the same logic in a simple operating example:

| Item | Amount |

|---|---|

| Beginning inventory | $2,000 |

| Purchases during period | $4,400 |

| Inventory available for sale | $6,400 |

| Ending inventory | $2,800 |

| COGS | $3,600 |

If you overstate ending inventory, COGS falls and profit looks better than reality. If you understate ending inventory, COGS jumps and profit looks worse. Either way, management decisions get distorted.

The three inventory buckets you need to track

Not all inventory sits in the same state. You need to separate:

- Raw Materials. Inputs you haven't used yet.

- Work in Progress. Items partially completed.

- Finished Goods. Items ready for sale.

Extensiv's overview makes this point clearly and also notes that these categories are treated as current assets, that valuation methods should be applied consistently, and that physical counts should be controlled with at least two people counting and a third spot-checking under its inventory accounting guidance.

A coffee roaster is an easy analogy. Green beans are raw materials. Beans being roasted and packaged are work in progress. Sealed bags ready to ship are finished goods. The same thinking applies to modern businesses. A hardware kit waiting to ship with a SaaS subscription is finished goods. Preconfigured units still being assembled are work in progress.

What belongs in inventory cost

Inventory isn't valued at some hopeful future selling price. It sits at historical cost, including acquisition-related costs such as purchase price and relevant transportation or handling costs. That matters because founders often bury parts of fulfillment cost in operating expense when they should be capitalized into inventory, or they capitalize things that should have been expensed already.

If your records don't tie back cleanly to a count and a valuation method, fix that before you talk about dashboards or forecasting. Start with the mechanics of inventory reconciliation.

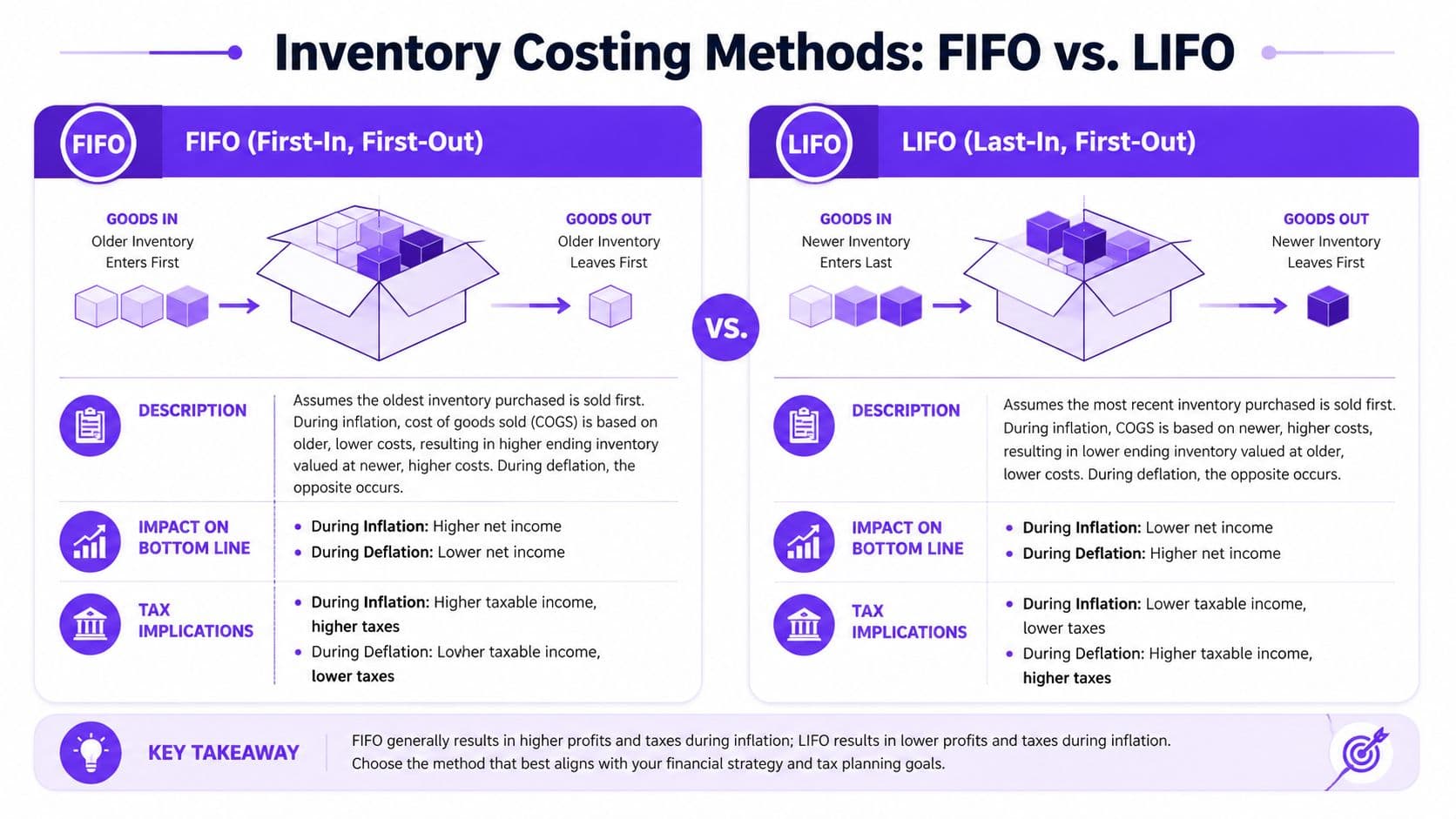

Choosing Your Inventory Costing Method FIFO vs LIFO

Your costing method isn't a technical footnote. It changes profit, taxes, and the story your financial statements tell.

Why method choice changes your reported profit

In a rising cost environment, FIFO results in lower COGS and higher reported profits, while LIFO does the opposite, and the choice can shift reported earnings and tax liabilities by up to 15-20% in volatile sectors, based on the explanation in Zuora's ASC 330 and inventory valuation summary.

That means your method choice affects:

- Gross margin presentation

- Tax timing

- Comparability across periods

- How conservative your balance sheet looks

Founders often pick a method because their software defaulted to it or their prior bookkeeper never raised the issue. That's lazy finance. Pick a method because it fits your business model and reporting priorities, then apply it consistently.

A side by side comparison

Use the same purchase pattern and watch the outcome change.

Assume you bought three units at rising costs:

- Unit 1 at $10

- Unit 2 at $12

- Unit 3 at $14

You sell two units.

| Method | COGS for 2 units sold | Ending inventory | What it does in rising costs |

|---|---|---|---|

| FIFO | $22 | $14 | Lower COGS, higher profit |

| LIFO | $26 | $10 | Higher COGS, lower profit |

| Weighted Average | $24 | $12 | Smooths the extremes |

This is why method choice matters operationally, not just academically. Under FIFO, older cheaper costs move into COGS first. Under LIFO, newer more expensive costs move first. Weighted average blends the pool.

Your gross margin can look strong or weak simply because of costing policy. If you don't know which method your books use, you don't actually know your margin.

My recommendation by business type

| Business type | Best default view |

|---|---|

| E-commerce and DTC | FIFO is usually the clearest for operational visibility and simpler gross margin reporting |

| Businesses with volatile input costs | Evaluate LIFO carefully if tax timing is a major concern and your reporting environment supports it |

| Businesses with mixed or pooled inventory | Weighted average can reduce noise when unit-level specificity isn't practical |

I generally prefer FIFO for growth companies because it aligns better with how founders think about physical flow and it usually produces cleaner internal reporting. But if cost volatility is severe, you should examine the tax impact with intent, not by accident.

If you're manufacturing or assembling products before sale, your costing method needs to fit your production workflow as well as your close process. That's where a more specialized framework for accounting for manufacturing becomes important.

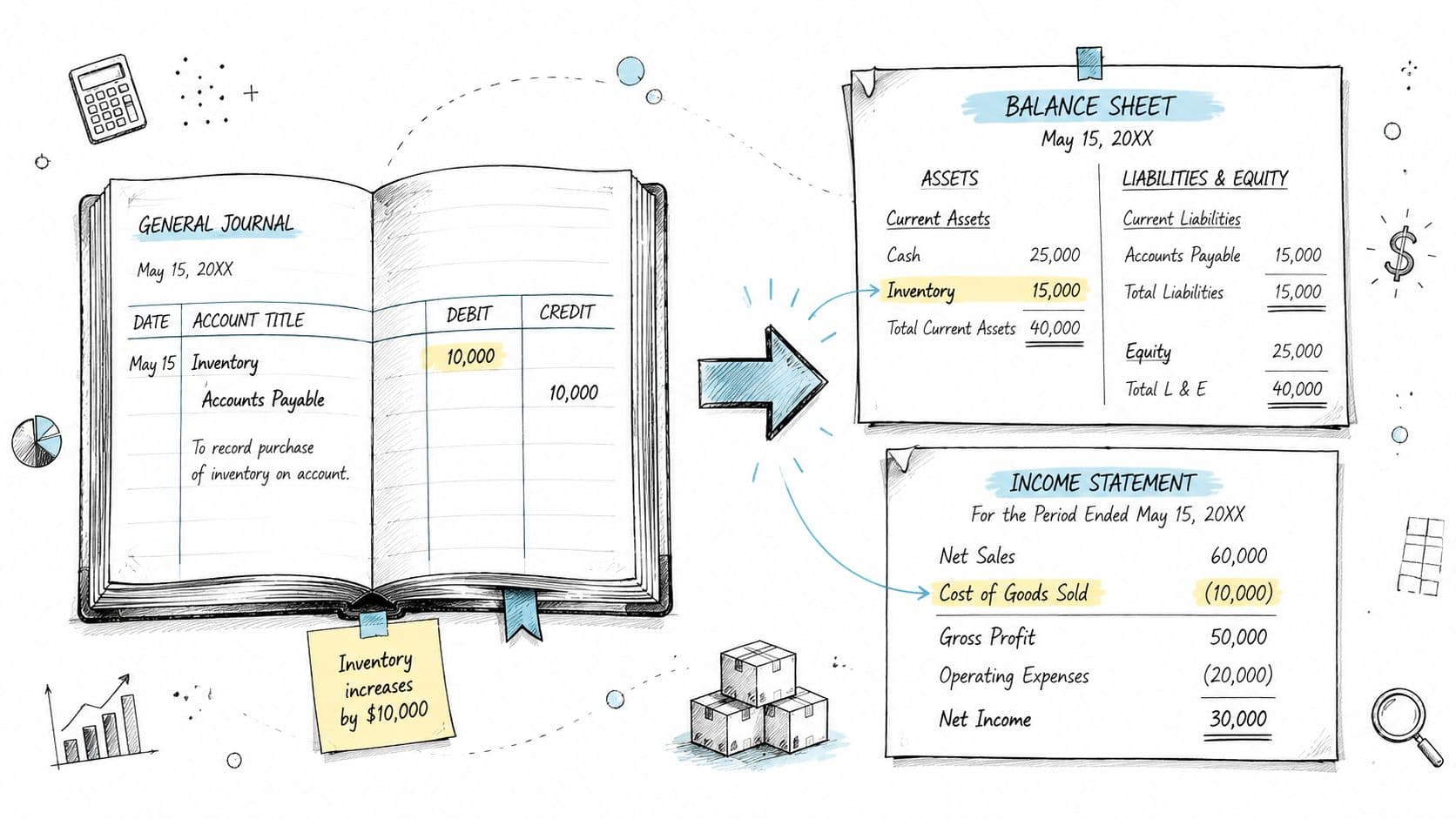

From Journal Entry to Financial Statement Impact

Bad inventory entries create fake profit. They also hide cash problems until you need a loan, a board deck, or a serious valuation conversation.

How one inventory purchase hits your books

If you buy goods for resale, starter kits for onboarding, replacement hardware for a SaaS product, or merch bundled into a client package, that purchase starts on the balance sheet. It is an asset until the related item is delivered or used.

The entry looks like this:

| Transaction | Debit | Credit |

|---|---|---|

| Purchase inventory | Inventory | Cash or Accounts Payable |

That entry increases assets. It does not reduce profit yet.

Founders get burned when the team books product purchases, inbound freight, or fulfillment inputs straight to expense. Your P&L takes the hit early, margin looks worse one month, then better the next, and nobody trusts the numbers. For an e-commerce brand, that distorts SKU profitability. For a hybrid SaaS business, it can make hardware-heavy customer cohorts look unprofitable when the issue is timing, not economics.

What happens when you sell the item

A sale usually creates two entries.

First, record the customer side:

| Transaction | Debit | Credit |

|---|---|---|

| Record sale | Cash or Accounts Receivable | Revenue |

Second, move the cost out of inventory:

| Transaction | Debit | Credit |

|---|---|---|

| Recognize product cost | COGS | Inventory |

Skip that second entry and your gross margin is fiction. Delay it and you overstate assets, understate expenses, and inflate EBITDA.

This matters even more in businesses that do not look like traditional inventory companies. If your agency pre-buys printed materials for a campaign, if your SaaS company ships a router or device, or if your e-commerce business bundles physical and digital products, the accounting still has to match cost with delivery. Modern business models do not exempt you from basic inventory discipline.

This walkthrough is worth watching if you want to see the accounting flow visually:

Operator's view: Each inventory sale reduces one asset on the balance sheet and records one expense on the income statement.

Why this matters at month-end

If your inventory subledger does not tie to the general ledger, your financials are not decision-grade.

The fallout is predictable. Gross margin by channel gets noisy. Cash forecasting gets weaker because inventory purchases and COGS timing no longer line up. Lenders question the balance sheet. Buyers and investors push harder on quality of earnings because they do not trust reported margin.

A disciplined close fixes this. Reconcile quantities, costs, and cutoffs every month. Review inventory-related entries before you finalize COGS. If your team needs a tighter process, strengthen your workflow for preparing board-ready financial statements.

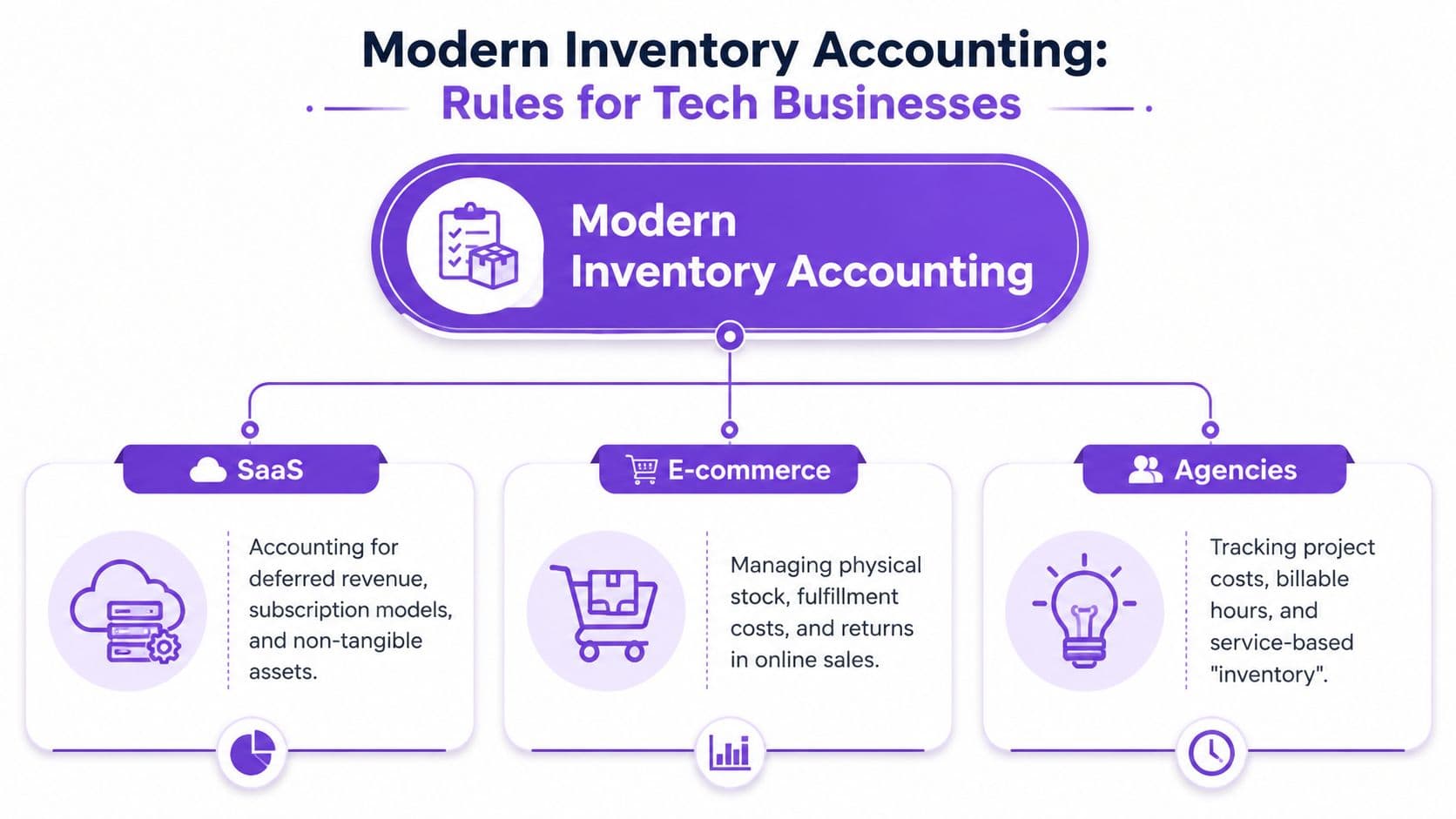

Inventory Rules for SaaS E-commerce and Agencies

Generic inventory advice is built for factories. Most growing companies don't operate that way. You need rules that reflect how your business earns revenue.

SaaS with physical components

If your SaaS business ships a hardware dongle, starter kit, router, sensor, or boxed setup item, don't leave that cost sitting on the balance sheet after it ships. Best practice is to expense the full cost immediately to COGS when the item leaves the door, so the physical cost matches the related service revenue, as explained in this discussion of SaaS companies shipping physical items.

That's where many hybrid companies get reporting wrong. They think, "We're SaaS, so inventory doesn't matter." It does if you ship anything required for onboarding, activation, or delivery.

There's a second layer if your contract bundles software access with a physical setup element. NetSuite's SaaS accounting explanation of ASC 606 notes that you must allocate transaction price across performance obligations based on standalone selling prices, then recognize the software portion over time and the physical setup portion upon delivery in its SaaS accounting overview.

E-commerce and agency realities

E-commerce founders usually know they have inventory. What they miss is valuation discipline. Returns, damaged stock, and obsolete units can keep sitting in the asset account far too long, which inflates the balance sheet and flatters margin.

Agencies and professional services firms often insist they have "no inventory." That's often false in practice. If you've prepaid media, bought licenses for client delivery, or acquired implementation materials that haven't yet been consumed, you still need a clear policy for when those costs sit as assets and when they move into expense.

If a cost is tied to future delivery, don't guess. Define whether it belongs in inventory, prepaid expense, or period expense, then apply that rule consistently.

A practical view by model

| Business model | What to watch closely | Accounting priority |

|---|---|---|

| SaaS | Hardware, onboarding kits, bundled contracts | Match shipped item cost to revenue timing |

| E-commerce | Returns, obsolete stock, damaged goods | Keep ending inventory realistic |

| Agencies | Prebought licenses, media, project-specific deliverables | Define asset versus expense rules clearly |

For SaaS specifically, many operators benchmark gross margin in the 80-90% range, and that benchmark depends on excluding unsold inventory from COGS and counting only the costs accrued in the period, as discussed in RevTek Capital's SaaS COGS overview. If your hybrid SaaS margin looks off, inventory treatment is one of the first places to look.

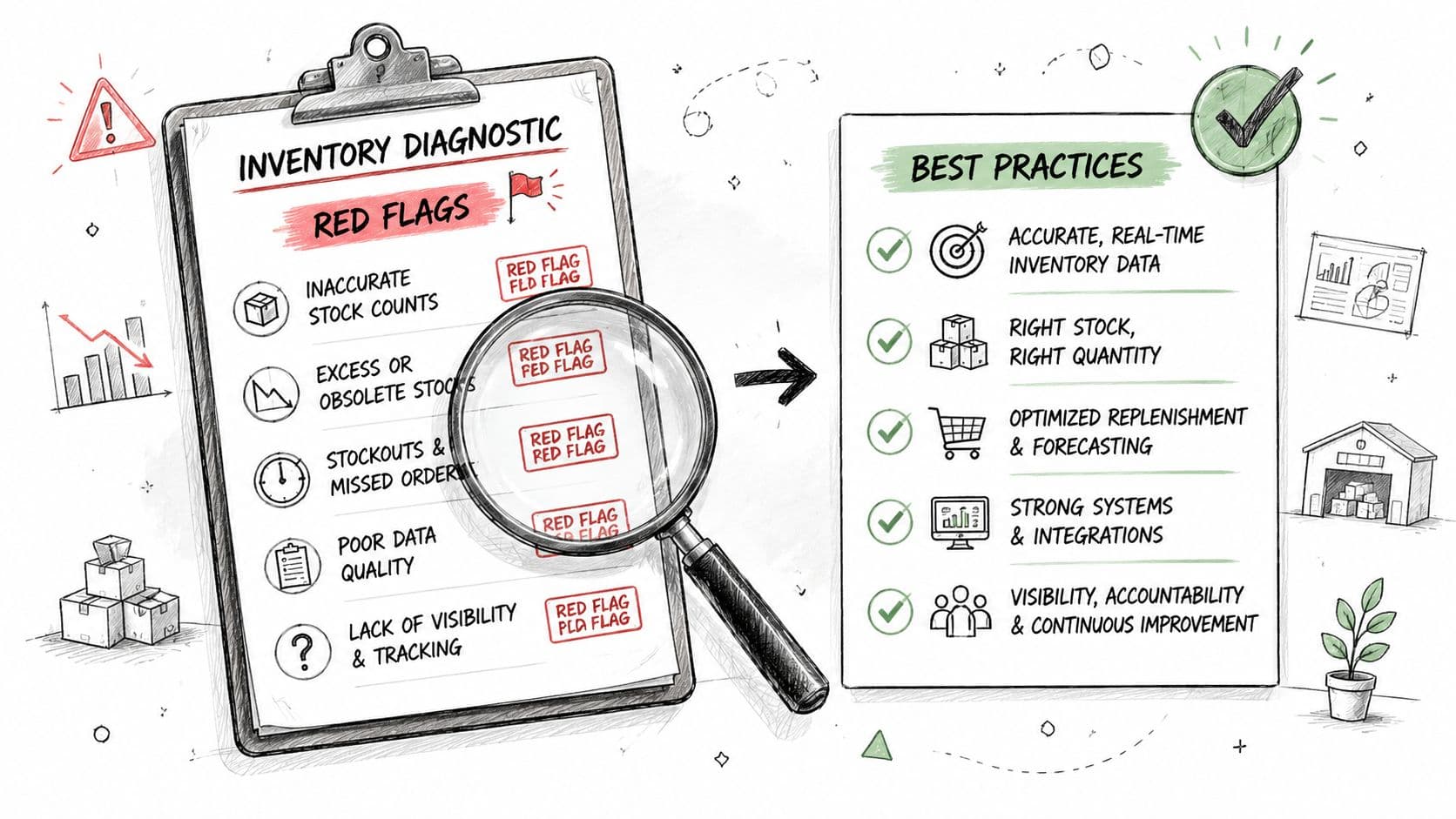

Common Errors and Inventory Management Best Practices

Founders love to say their inventory process is "good enough." It usually isn't.

Red flags

If any of these sound familiar, your inventory accounting is weakening your numbers right now:

- Spreadsheet dependence. Your operational count lives in Excel, but accounting lives somewhere else.

- No formal count process. People "know roughly what's on hand" but don't run disciplined physical counts or cycle counts.

- Obsolete stock stays on the books. Damaged, expired, slow-moving, or unusable items remain valued like healthy inventory.

- Inconsistent treatment of shipping and handling. The same cost gets capitalized one month and expensed the next.

- Returns and shrinkage get buried. Variances are plugged instead of investigated.

NetSuite's inventory management discussion points to inconsistent tracking in decentralized environments as a major driver of loss and visibility problems in its inventory management challenges overview. That's especially relevant if your stock sits across multiple warehouses, 3PLs, retail points, or remote teams.

What to tighten this month

Don't overhaul everything at once. Fix the controls that drive reporting quality first.

- Create one source of truth. Your accounting system and inventory records have to reconcile. If you're using QuickBooks, Xero, Shopify, or NetSuite, define which system owns quantity and which owns financial value.

- Write a count policy. Assign who counts, who reviews, how you handle zero counts, and how you document damaged or obsolete items.

- Set write-down rules. If inventory is no longer saleable at recorded value, reduce it. Keeping it inflated doesn't protect profit. It hides problems.

- Review forecasting discipline. If your purchasing team needs a practical operating resource, this guide to inventory forecasting and FBA automation is useful because it connects inventory planning to execution instead of stopping at theory.

Management test: If you can't explain why inventory changed from the beginning to the end of the month, you don't control it.

When to Outsource Your Inventory Accounting

Outsource inventory accounting before bad inventory data starts dictating your decisions. By the time your team is debating quantity on hand, revising COGS after close, or explaining margin swings with guesses, you've already lost money.

The trigger is not business size. The trigger is complexity. A Shopify brand with bundled products, Amazon fees, returns, and inventory split across a 3PL and retail pop-ups can outgrow DIY accounting fast. So can a SaaS company selling hardware, prepaid implementation blocks, usage credits, or reseller licenses. Agencies run into the same problem when they carry pass-through media, production materials, or prepaid vendor commitments that hit margin in the wrong period. Asset-light does not mean inventory-light.

Watch for the failure pattern. The close slips. Gross margin moves after invoices are sent. Tax filings need cleanup. Lenders and investors ask simple questions about inventory, deferred costs, or fulfillment economics, and nobody gives the same answer twice. That is a finance systems problem, not a bookkeeping inconvenience.

Good outsourced support fixes it in three places. First, it sets ownership across operations, accounting, and fulfillment so quantity, cost, and write-down decisions do not live in separate spreadsheets. Second, it applies one accounting policy across channels, products, bundles, returns, and hybrid digital offers. Third, it produces reporting you can use for pricing, purchasing, and cash planning. That matters if you're trying to protect working capital and avoid stockouts without distorting margin.

Founders should not spend nights chasing inventory variances.

You should spend that time on pricing, sales efficiency, hiring, and capital allocation. Bring in specialists to build reconciliations, cut close time, and make inventory logic hold up under audit, diligence, and board scrutiny. If you're evaluating that move, this guide to outsourced controller services for growing companies is the right starting point.

If your books cannot produce clean inventory, clean COGS, and believable gross margin on demand, your valuation takes a hit. Jumpstart Partners helps SaaS, agency, e-commerce, and service businesses build investor-ready financials, tighten month-end close, and turn messy inventory logic into clear cash flow visibility.