Financial Operations

Reconciliation of Inventory: A Founder's Guide to Accuracy

Learn the reconciliation of inventory process step-by-step. A guide for founders on methods, journal entries, and audit controls to improve cash flow.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

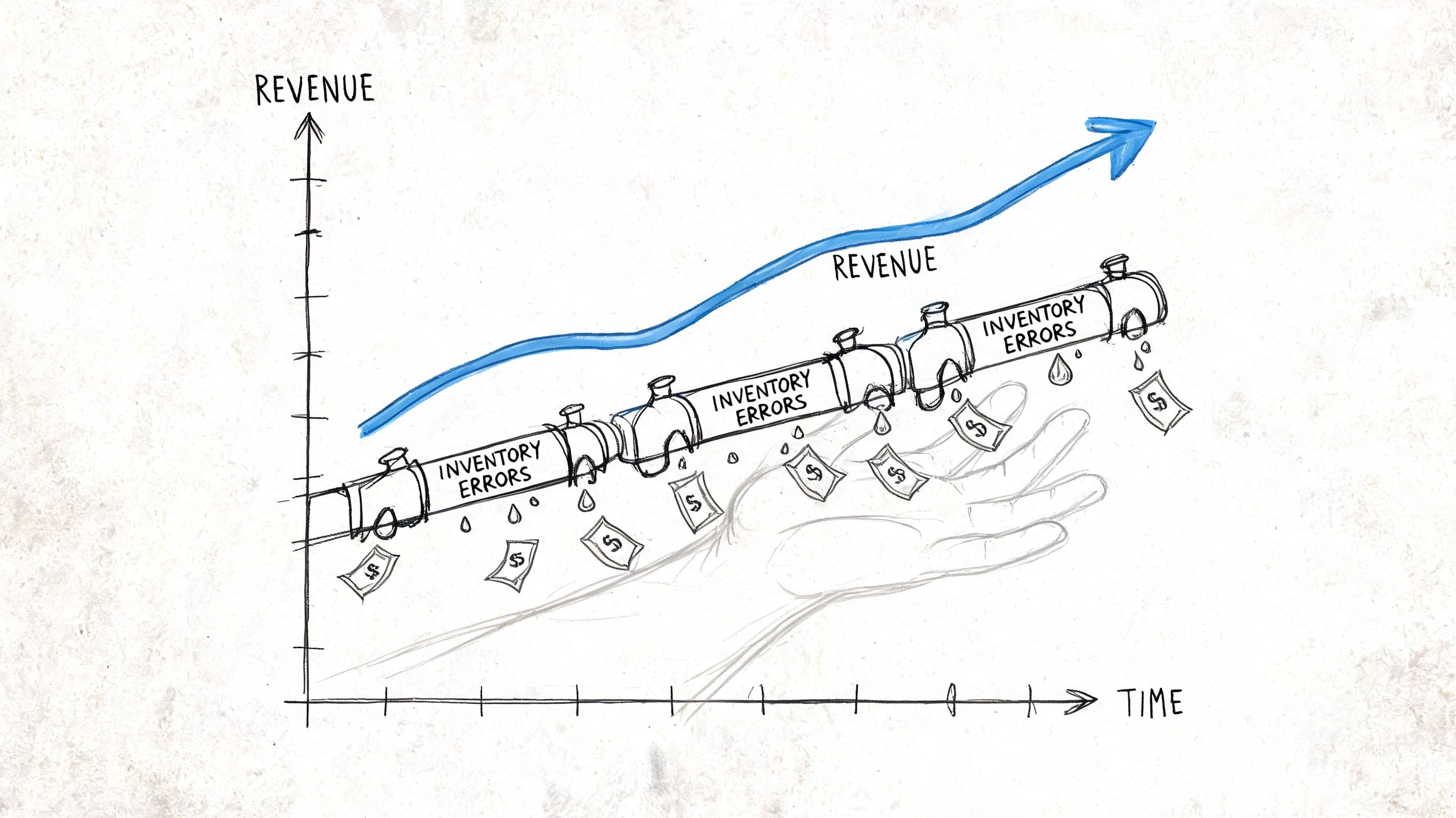

··16 min readRevenue growth doesn't protect you from bad inventory numbers. In fact, growth often hides the problem until cash gets tight, margins look wrong, or an investor starts asking why your balance sheet doesn't match operational reality.

If your business sells physical products, bundles hardware with software, manages replacement parts, or ships onboarding kits, the reconciliation of inventory isn't a back-office chore. It's a core financial control. When inventory is off, gross margin is off. Cash forecasts are off. Your month-end close slows down. Due diligence gets harder.

Founders usually notice the symptom first. Stockouts that "shouldn't" happen. Unexpected write-downs. COGS that move in ways no one can explain. The fix isn't another spreadsheet. It's a repeatable reconciliation process tied directly to accounting, operations, and management reporting.

Why Inaccurate Inventory Is a Silent Business Killer

Inventory shrinkage costs US retailers an estimated $136.1 billion annually, representing 1.75% of sales, according to the National Retail Federation's 2024 National Retail Security Survey. For a business with $10M in revenue, that seemingly small percentage translates to a direct $175,000 hit to the bottom line (National Retail Federation data discussed here).

That number gets founders' attention because it reframes inventory errors for what they are. Not a warehouse issue. Not an accounting annoyance. A direct profit leak.

If you're running a business between $500K and $20M in revenue, bad inventory data creates three immediate problems:

- Profitability gets distorted. If inventory is overstated, COGS is understated. Your margin looks better than reality.

- Cash flow decisions get worse. You reorder based on bad numbers, tie up cash in excess stock, or miss revenue because the item you thought you had isn't there.

- Audit and diligence risk rises. Investors and buyers don't trust financials when inventory controls are loose.

This matters even more for tech and service businesses with physical components. A SaaS company with shipped devices, an agency selling branded kits, or a professional services firm holding billable equipment can all end up with inventory exposure that's large enough to affect working capital, borrowing base conversations, and valuation. If you're trying to tighten liquidity, this is the same conversation as improving working capital.

Practical rule: If you can't explain your inventory variance quickly, you don't have a reliable inventory process.

I've seen founders treat inventory discrepancies as temporary noise that will sort itself out during year-end cleanup. It doesn't work that way. Unreconciled inventory compounds into bad decisions month after month. By the time finance catches it, you've already purchased the wrong items, missed margin targets, and reported numbers you can't fully defend.

What is Inventory Reconciliation Really?

At a practical level, inventory reconciliation means proving that the quantity and value in your system match what you have on hand. It's the inventory version of a bank reconciliation. You wouldn't run the business based on what you hope is in the bank. You shouldn't run it based on what your ERP or accounting file says is sitting on a shelf.

The accounting backbone is straightforward:

Ending Inventory = Beginning Inventory + Net Purchases - COGS

That formula matters because it tells you what the books expect. A physical count tells you what's real. Reconciliation is the discipline of comparing those two numbers, investigating the gap, and updating the books with documentation.

Periodic versus perpetual

A lot of businesses still operate on a periodic mindset. They count everything at month-end, quarter-end, or year-end and then scramble to explain variances. That approach creates stress, slows operations, and pushes problems into one painful event.

A perpetual process is different. Inventory movements get recorded continuously through purchasing, receiving, fulfillment, returns, and adjustments. Physical counts still matter, but they validate the system instead of replacing it.

Here's the difference in plain terms:

| Approach | How it works | What usually happens |

|---|---|---|

| Periodic reconciliation | Count large portions of inventory at set intervals | Big surprises, operational disruption, delayed closes |

| Perpetual reconciliation | Update records continuously and validate with recurring counts | Faster issue detection, cleaner month-end, stronger audit trail |

For businesses with fragmented finance ops, inventory errors often sit next to AP errors, invoice mismatches, and timing issues. If that's happening in your business, the same process discipline behind optimizing invoice workflows with AI often improves inventory reconciliation too. The common thread is matching transactions to real-world activity before the close.

What good reconciliation produces

The ultimate output isn't just an adjusted inventory balance. It's a single source of truth that operations, finance, and leadership can trust.

That means:

- Physical counts validate the books.

- Variances get investigated, not ignored.

- Adjustments are documented with support.

- Management reporting uses numbers you can defend.

Inventory reconciliation isn't complete when the numbers match. It's complete when you know why they didn't match in the first place.

If your trial balance carries inventory that no one has physically validated, you're not working from clean financial statements. You're working from assumptions. That becomes obvious when the controller tries to tie inventory into the broader close process and the balances don't reconcile cleanly. If you need a refresher on how inventory flows into the books, this overview of a trial balance is worth revisiting.

Choosing Your Reconciliation Method and Frequency

The right method depends on transaction volume, SKU mix, item value, and operational complexity. The wrong method creates either too much labor or too little control. Founders often choose based on what feels familiar. You should choose based on where financial risk sits.

Full physical counts

A full physical count means stopping normal activity and counting everything. This method still has a place. It's useful when you're cleaning up a messy inventory file, preparing for an audit, or resetting after a major systems change.

But it comes with real trade-offs.

| Method | Best use case | Main upside | Main downside |

|---|---|---|---|

| Full physical count | Cleanup, year-end validation, post-migration reset | Complete snapshot of actual inventory | Disruptive, slow, often reactive |

| Cycle counting | Ongoing operations with regular movement | Continuous control without shutdowns | Requires discipline and ownership |

| Hybrid approach | Businesses in transition | Balances reset events with ongoing maintenance | Can fail if roles aren't clear |

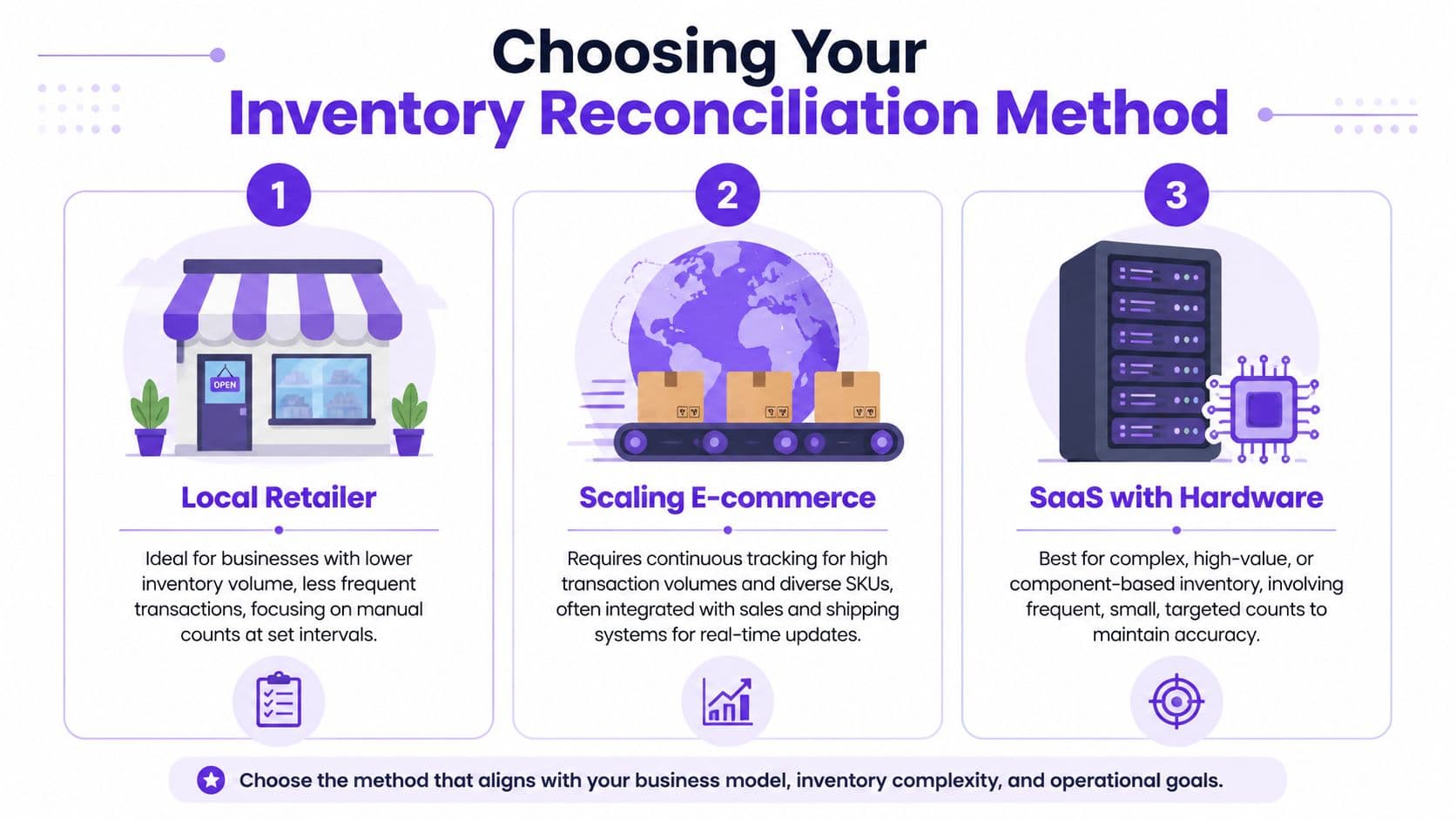

For a smaller local retailer with limited SKU complexity, periodic full counts may still be manageable. For a scaling e-commerce operation or a SaaS company shipping hardware, this approach breaks down quickly. The faster inventory moves, the less useful an annual surprise becomes.

ABC cycle counting

This is the method I recommend most often because it aligns effort with financial impact. The idea comes from the long-standing ABC framework in inventory management, where roughly 20% of SKUs typically represent 80% of inventory value. Those high-value items need more frequent attention.

Implementing ABC cycle counting can boost ongoing inventory accuracy to over 97%, a significant jump from the 5-10% discrepancy rates often found during annual physical counts in mid-sized firms. This also cuts reconciliation time by up to 70% by eliminating operational shutdowns. That data appears in the earlier-cited industry discussion on inventory reconciliation.

A practical cadence looks like this:

- A items: Count frequently because mistakes here hit margin and cash fast.

- B items: Count on a regular but less intense schedule.

- C items: Count less often, but don't ignore patterns of recurring variance.

What works for different business models

The best frequency isn't the same for every company.

Local retailer

If counts are still mostly manual and volumes are manageable, periodic counts can work. But the moment variances start affecting reorders or margin reporting, move toward recurring cycle counts.

Scaling e-commerce

You need ongoing visibility. High order volume, returns, multi-channel sales, and fulfillment timing create too many moving parts for infrequent counting.

SaaS with hardware

This group gets underestimated. A company shipping devices, replacement units, bundled onboarding equipment, or serial-tracked components needs counts tied to both physical stock and subscription reporting.

Count based on risk, not convenience. High-value and high-velocity items deserve attention first.

A founder objection I hear a lot is, "We don't have enough inventory to justify a formal process." That's usually wrong. If inventory is material enough to affect COGS, cash planning, customer delivery, or diligence, it's material enough to reconcile properly.

The Reconciliation Workflow From Count to Close

A clean inventory reconciliation process is operational, not theoretical. The workflow should be simple enough for your team to run consistently and strong enough for your controller or auditor to review without guessing what happened.

Step 1 through step 3

Start with control over the count itself.

- Set a cutoff. Define the exact point when receiving, shipping, and transfers stop or get separately logged. Without a cutoff, you're comparing a moving target to a static count sheet.

- Prepare the inventory locations. Label bins, isolate returns, separate damaged goods, and make sure consigned or customer-owned inventory isn't mixed into your count.

- Run the physical count. Use blind counts where possible so staff count what they see, not what the system says they should see.

Step 4 through step 6

After the count, finance has to convert raw activity into a defendable accounting result.

- Compare physical count to the system. Pull the book quantity and book value by SKU as of the cutoff.

- Investigate differences. Check receiving logs, shipping records, returns, transfer activity, and recent manual adjustments.

- Post the adjustment. Once the discrepancy is resolved or accepted as shrinkage, update the books with support.

The support matters. If inventory is changed without a paper trail, you fixed the number but weakened the control.

Worked example with real numbers

Use the standard formula first:

Ending Inventory = Beginning Inventory + Net Purchases - COGS

Assume the following for one item category:

- Beginning inventory: $120,000

- Net purchases during the period: $80,000

- COGS recorded during the period: $140,000

Your book ending inventory is:

$120,000 + $80,000 - $140,000 = $60,000

Then your team performs the physical count and values the inventory at $55,000.

That means you have a $5,000 shrinkage.

Here is the reconciliation summary:

| Item | Book Value (System) | Physical Count Value | Discrepancy (Shrinkage) | Journal Entry |

|---|---|---|---|---|

| Inventory category total | $60,000 | $55,000 | $5,000 | Debit Inventory Shrinkage Expense $5,000; Credit Inventory $5,000 |

The journal entry is straightforward:

- Debit Inventory Shrinkage Expense $5,000

- Credit Inventory $5,000

That entry does two things. It reduces the inventory asset on the balance sheet to what you have on hand, and it records the loss in the period so your P&L reflects reality.

If the books say $60,000 and the shelf says $55,000, you do not have a $60,000 asset.

What finance leaders should review before posting

Before you finalize the entry, check these points:

- Recent receipts: Were goods received physically but not entered yet?

- Unshipped orders: Did the system relieve inventory before product left?

- Returns timing: Were returned items counted physically but not reinstated in the system?

- Unit cost issues: Does valuation reflect the correct cost, not just the right quantity?

- Duplicate adjustments: Did someone already post a manual correction upstream?

For many businesses, inventory issues are what prevent a disciplined close. If your month-end keeps getting delayed by stock variances, it helps to align this process with a broader month-end close checklist so inventory isn't handled as an afterthought.

Close the loop, not just the balance

The final step is managerial, not mechanical. Document what caused the discrepancy and what control changes follow from it. If a count found receiving errors, change the receiving process. If unscanned returns created the problem, change how returns hit the system.

A reconciliation that ends with an adjustment but no process improvement guarantees repeat errors.

Investigating Discrepancies A Troubleshooting Guide

A variance isn't the problem. It's evidence of a problem.

The most effective finance teams treat inventory discrepancies like failed controls, not random noise. If the same SKU is off repeatedly, or if certain locations always produce write-downs, that's a process signal. You need to trace it back to a human action, a system gap, or a weak handoff.

Top-performing businesses maintain a shrinkage rate below 1% and an inventory accuracy rate above 98%. Key causes of shrinkage to investigate are theft (35%), damage (25%), and administrative errors (30%), according to NRF data (retail inventory reconciliation benchmarks).

Red flags worth escalating fast

Use this checklist when a variance appears:

- Repeated SKU variances: The same item goes missing or gets overstated count after count.

- Timing mismatches: Inventory moves near month-end don't match receiving or shipping records.

- One-shift patterns: Errors cluster around one team, one location, or one process handoff.

- Return problems: Returned items re-enter the building but never re-enter the system.

- Damage without documentation: Stock is unusable, but no one recorded a write-off or disposition.

Match the variance to the likely root cause

| Symptom | Likely cause | What to review |

|---|---|---|

| Inventory always lower than books | Theft, unrecorded shipments, damage | Fulfillment logs, scrap records, access controls |

| Inventory always higher than books | Receiving delays, duplicate sales relief, bad unit setup | PO receipts, item mapping, integration timing |

| Variances spike after promotions | Process overload | Picking accuracy, returns flow, temporary labor training |

| High-velocity items drift most | Weak scan discipline | Barcode usage, bin movements, cycle count cadence |

The adjustment fixes the ledger. The investigation protects the business.

The common founder mistake is to post the write-down and move on. That's acceptable once. It becomes negligence when it repeats. If inventory is material, track shrinkage rate, inventory accuracy, and discrepancy resolution rate every month. Those metrics tell you whether the process is improving or whether you're just getting faster at booking losses.

System Tips for QuickBooks Xero and NetSuite

Your accounting system doesn't solve inventory reconciliation on its own. It either supports a disciplined process or records the consequences of a weak one. The difference comes down to setup, integration quality, and how consistently your team uses the system.

QuickBooks and Xero

In QuickBooks, start with the inventory valuation reports and recent adjustment history. Review whether purchases, sales, and manual inventory changes are flowing to the right accounts. If you see frequent manual entries with weak descriptions, your audit trail is already compromised.

In Xero, the risk is often app sprawl. Inventory may sit partly in Xero and partly in a separate operational tool, with timing mismatches between the two. That setup can work, but only if ownership is clear and reconciliation happens on a schedule.

For businesses whose files are already messy, a cleanup often has to happen before reconciliation becomes reliable. That's where targeted work like QuickBooks cleanup services can remove historical noise before you build new controls.

NetSuite and hybrid inventory

NetSuite is stronger when you need item-level control, serial tracking, location logic, and structured cycle counting. But more capability also means more room for bad configuration. If units of measure, item types, or fulfillment workflows are wrong, NetSuite will faithfully produce bad numbers at scale.

This gets more serious for hybrid SaaS businesses. For SaaS companies with hybrid physical inventory, reconciling hardware with subscription data is critical. A 5% shrinkage from unreturned units on a stock of 1,000 IoT devices can lead to a $50K+ overstatement of ARR, a major red flag for investors during due diligence. This issue is a focus of Deloitte's 2025 Tech Inventory Report (hybrid inventory discussion here).

If you're shipping devices tied to subscriptions, don't reconcile only the stock ledger. Reconcile serial-tracked units to active subscriptions, returns, replacements, and unreturned hardware status. That's how you avoid reporting ARR that assumes deployed assets are still producing valid subscription economics.

A short walkthrough can help your team visualize how the process should connect across systems:

What auditors expect to see

Auditors and diligence teams usually look for the same core controls:

- Clear cutoff procedures

- Documented count results

- Approval of manual adjustments

- Consistent valuation methodology

- Traceable support from count to journal entry

If you can produce those quickly, inventory becomes a controlled balance. If you can't, it becomes a credibility issue.

When to Outsource Your Inventory Accounting

You should outsource inventory accounting when the internal cost of doing it poorly exceeds the external cost of doing it right. For most founder-led businesses, that point arrives earlier than they expect.

Here are the signs:

- Month-end stalls on inventory. Finance can't close because operations and accounting don't agree.

- Nobody owns the full process. Purchasing, warehouse, fulfillment, and bookkeeping each handle a slice, but no one reconciles the whole flow.

- You need investor-ready numbers. Fundraising, audit prep, lender reporting, or a quality-of-earnings review puts pressure on inventory accuracy.

- The founder is acting as the tie-breaker. If you're still resolving stock questions personally, the process isn't scalable.

"Founders often underestimate the strategic importance of flawless financial controls. Accurate inventory reconciliation isn't just about avoiding losses; it's about building a trustworthy financial narrative that underpins your company's valuation." - Expert Quote Placeholder, e.g., Managing Partner at a VC firm or Jumpstart CEO.

Outsourcing doesn't mean giving up control. It means installing control. A good outsourced finance team builds the count calendar, ties system activity to accounting, reviews variances, and forces documentation before adjustments hit the ledger. For some companies, support staff can help with repeatable admin tasks around bookkeeping. If you're sorting out where a virtual assistant fits versus where a controller-level review is required, Match My Assistant's VA guide is a useful comparison point.

The work usually belongs with a controller-minded partner, not a generic bookkeeper. For example, Jumpstart Partners handles outsourced controller work for growing businesses, including reconciliation workflows across platforms like QuickBooks, Xero, NetSuite, Stripe, and Shopify, with inventory controls folded into a broader close process. If you're evaluating that model, their overview of outsourced controller services shows what should sit inside the role.

A common objection is, "We're not big enough yet." That's backwards. You don't wait until diligence to build clean inventory records. You build them before they become a negotiation point in diligence.

If inventory discrepancies are delaying your close, distorting margins, or creating diligence risk, talk to Jumpstart Partners. They help growing businesses build reliable reconciliation processes, tighten month-end, and produce financials you can effectively use to run the company.