Financial Operations

What Is Rev Rec? a Founder's Guide to ASC 606 & Audits

What is rev rec? Learn the ASC 606 five-step model, see SaaS examples, and avoid common errors. Get your financials audit- and investor-ready with our guide.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··15 min readRevenue recognition, or rev rec, is the rule that tells you when money becomes earned revenue, not when cash lands in your account. Under ASC 606, issued by FASB in May 2014, you have to follow a five-step model to recognize revenue based on when control of goods or services transfers to the customer.

That sounds technical. For a founder, it's operational. If you book revenue too early, your MRR, ARR, margins, and deferred revenue all stop telling the truth. If you're raising capital, preparing for an audit, or selling a business, that's where the problem shows up.

This gets more dangerous as your pricing gets more complex. A basic annual SaaS contract is usually straightforward. A contract that bundles software, onboarding, training, support, or usage-based pricing isn't. That's where a lot of growing companies drift out of compliance without realizing it.

Founders often assume rev rec is a controller problem that can wait. It isn't. It directly affects investor trust, audit readiness, and how clearly you can see your own performance.

Table of Contents

- Why Revenue Recognition Can Make or Break Your Next Funding Round

- The ASC 606 Five-Step Model Explained

- Rev Rec in Practice for SaaS and Subscription Companies

- Navigating Complex Scenarios Bundles and Usage-Based Pricing

- Common Rev Rec Errors and Audit Red Flags

- Building a System for Audit-Ready Financials

- When to Outsource Your Revenue Recognition Process

Why Revenue Recognition Can Make or Break Your Next Funding Round

If your financials don't show earned revenue correctly, investors won't trust the rest of the package either.

Under US GAAP, ASC 606 governs revenue recognition. Its core principle is that you recognize revenue to depict the transfer of promised goods or services to customers in the amount you expect to be entitled to, which means revenue is recorded when it's earned, rather than when cash is received, as explained in Meaden & Moore's ASC 606 overview.

That distinction matters most when your business gets paid before delivery, or delivers in phases. SaaS companies, agencies, and professional services firms all do this constantly. You collect cash upfront, then perform over time. If you treat bookings like revenue, your P&L looks stronger than reality and your balance sheet carries the wrong liabilities.

Why this turns into a deal issue

Investors and acquirers don't just review topline growth. They test whether your revenue is durable, whether deferred revenue is real, and whether contract terms match the accounting. If your rev rec process is weak, they'll question your KPIs too.

A good diligence process always pulls on this thread. If you're preparing for a review, this Proven SaaS due diligence guide is useful because it reflects how buyers pressure-test metrics, contracts, and reporting consistency. The same issues also show up in formal investor due diligence workflows.

Practical rule: If revenue timing depends on service delivery, milestones, implementation, or usage, you don't have a bookkeeping detail. You have a finance risk.

What founders get wrong

The common objection is simple: “We got paid, so why can't we count it?”

Because GAAP doesn't ask when you got paid. It asks when you delivered control of the promised good or service. That's why rev rec affects valuation conversations. A buyer will forgive complexity. They won't forgive numbers they can't rely on.

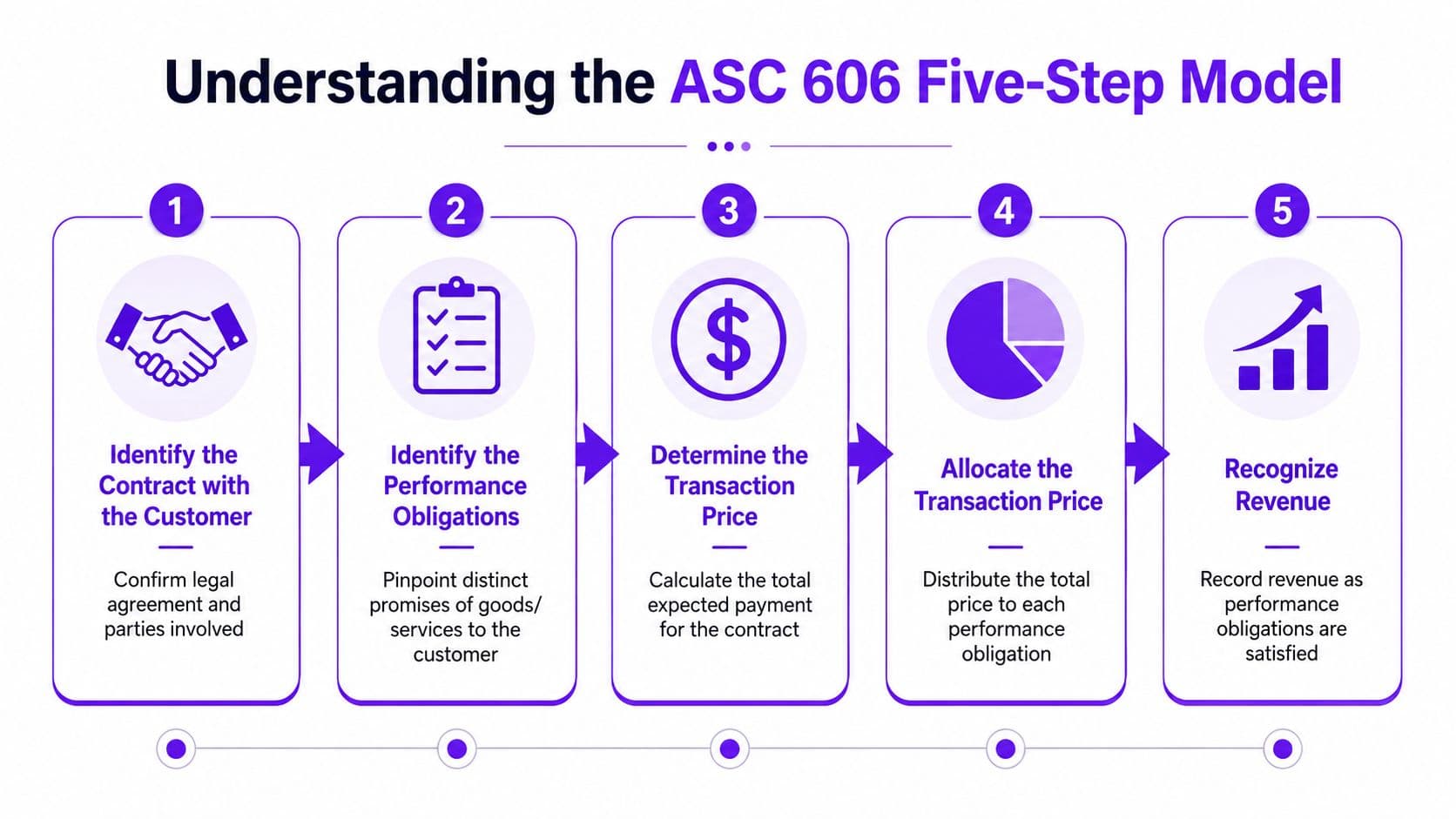

The ASC 606 Five-Step Model Explained

The standard answer to “what is Rev Rec?” is ASC 606's five-step model. That model exists so companies recognize revenue consistently, whether they sell software subscriptions, implementation projects, support packages, or service retainers.

Early in the process, it helps to see the framework visually.

The model in plain English

| Step | Action | Key Question It Answers |

|---|---|---|

| 1 | Identify the contract | Do you have an enforceable agreement with the customer? |

| 2 | Identify the performance obligations | What distinct goods or services did you promise? |

| 3 | Determine the transaction price | What total consideration do you expect to receive? |

| 4 | Allocate the transaction price | How much of that price belongs to each obligation? |

| 5 | Recognize revenue | When is each obligation actually satisfied? |

Here's how to think about each step:

-

Identify the contract.

Goal: Confirm there's a valid arrangement with rights, obligations, and payment terms.

Action: Review signed order forms, MSAs, SOWs, renewals, and modifications. -

Identify the performance obligations.

Goal: Separate the contract into distinct promises.

Action: Decide whether software access, setup, training, support, or services should be accounted for separately. -

Determine the transaction price.

Goal: Define the total amount you expect to receive.

Action: Include fixed fees and evaluate variable items like credits, incentives, and usage-based charges. -

Allocate the transaction price.

Goal: Assign the right amount of revenue to each obligation.

Action: Use Standalone Selling Price, or SSP, for each element. According to BDO's SaaS revenue recognition guidance, if observable SSP isn't available, you must use reasonable estimates based on relative standalone value, not arbitrary splits. -

Recognize revenue.

Goal: Record revenue when or as the obligation is satisfied.

Action: Book revenue over time for ongoing service delivery, or at a point in time when a one-time obligation is complete.

A concise walkthrough helps if you want the framework in video form:

Where founders usually get tripped up

Organizations are fine on Step 1 and Step 3. They struggle on Step 2 and Step 4.

That's because contracts rarely stay simple. Sales adds onboarding. Customer success adds managed support. Pricing introduces discounts or credits. Product adds usage-based billing. Suddenly one deal contains multiple obligations and the accounting team has to unwind what the commercial team packaged together.

The hardest rev rec issues usually start upstream, inside pricing and contract design, not downstream in the GL.

If your contracts include variable fees, this becomes even harder because the estimate itself affects recognition timing. That's why it helps to map contract terms directly to your rev rec logic before they hit the ledger. This is especially important when handling variable consideration under ASC 606.

Rev Rec in Practice for SaaS and Subscription Companies

For a typical SaaS company, the cleanest way to understand rev rec is to separate cash collection from revenue earned.

A simple annual SaaS example

Assume a customer signs a $24,000 annual software contract and pays the full amount upfront on January 1. The customer receives access for 12 months.

You did receive $24,000 in cash on day one. You did not earn $24,000 on day one.

You earn the revenue ratably over the service period:

- Total contract value: $24,000

- Contract term: 12 months

- Monthly revenue recognition: $24,000 ÷ 12 = $2,000 per month

That is the core rev rec idea for recurring SaaS. It matches the broader pattern described in MLRPC's SaaS revenue recognition example, where a $50,000 annual contract results in $4,166.67 recognized each month instead of all at signing.

What the journal entries look like

On the day you invoice and collect cash:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Jan 1 | Cash | $24,000 | |

| Jan 1 | Deferred Revenue | $24,000 |

That entry says: you have the cash, but you still owe the customer service delivery.

At the end of each month, as you provide the software access:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Jan 31 | Deferred Revenue | $2,000 | |

| Jan 31 | Subscription Revenue | $2,000 |

You repeat that each month until the deferred revenue balance reaches zero.

Founder takeaway: If cash comes in before delivery, your balance sheet carries the story first. Your income statement catches up over time.

Why this matters beyond the P&L

This is why deferred revenue matters so much. It's not a technical nuisance. It's the liability created when you've been paid for work you haven't fully delivered yet.

If you skip the deferred revenue schedule, your monthly financials won't hold up. Revenue will look lumpy, margins will swing for the wrong reasons, and board reporting will become a cleanup exercise instead of a decision-making tool. If you need a practical primer on the balance sheet side, this explanation of what deferred revenue means in practice is worth reviewing.

A common misconception

Founders often say, “But the contract is signed. The customer is committed.”

That's not the test. The accounting question is whether the performance obligation has been satisfied. For cloud software access, customers benefit continuously over the term, so the revenue is recognized over time.

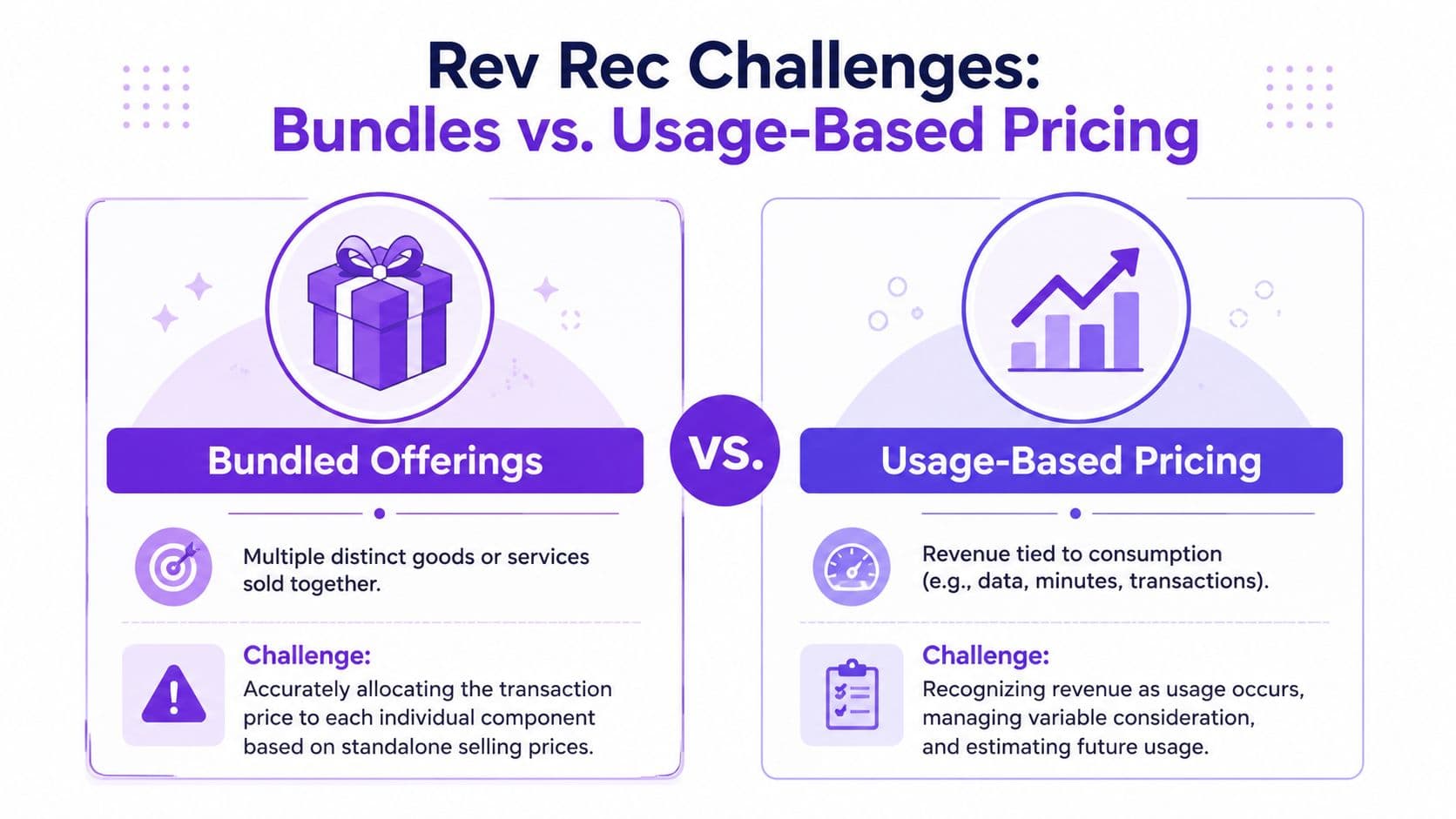

Navigating Complex Scenarios Bundles and Usage-Based Pricing

The generic guides usually stop at straight-line subscriptions. Real companies don't.

If you bundle software with implementation, training, or managed support, the accounting gets more nuanced fast. The same is true when pricing depends on API calls, transactions, storage, or credits. These aren't edge cases anymore.

Bundled contracts need allocation

According to Precursive's writeup citing a 2024 Financial Executive Research Foundation survey, 68% of SaaS firms with revenue between $5M–$20M reported audit adjustments related to improperly allocated bundled revenue, while less than 12% of public rev rec guides cover allocation across distinct performance obligations.

That tracks with what shows up in diligence. Teams understand subscriptions. They miss the split between recurring software and non-recurring services.

Use a concrete example. A contract is worth $12,000 and includes:

- 12 months of software access

- A 4-month implementation service

Under ASC 606, you don't just spread the full $12,000 evenly unless the standalone values justify that. You allocate the total transaction price based on the standalone selling price of each component, then recognize the implementation revenue after 4 months while spreading the software revenue over 12 months, as illustrated in this ASC 606 example video reference.

If your team allocates bundled deals with rough percentages or equal splits because “it seems close enough,” that's exactly where errors start.

Bundled contracts fail when finance inherits a sales package that was never translated into distinct obligations and SSP logic.

Usage-based pricing changes the timing

Usage-based models create a different problem. The issue isn't just allocation. It's variable consideration.

For variable fees such as usage-based charges or credits, ASC 606 requires you to estimate the amount and apply a constraint so you only recognize the portion that is highly probable not to result in a significant reversal when uncertainty is resolved, as explained in Orb's SaaS revenue recognition guide.

That means you can't treat projected usage like guaranteed revenue. You need a defensible method tied to actual consumption data and contract terms.

A practical way to think about it:

| Scenario | What works | What doesn't |

|---|---|---|

| Fixed subscription fee | Recognize over the contract term | Booking all cash upfront as revenue |

| One-time implementation | Recognize when the implementation obligation is satisfied | Spreading it mechanically with the subscription if it's distinct |

| Usage-based charges | Recognize based on usage and constrained estimates | Recognizing forecasted usage as if it were fixed consideration |

Why this gets missed

The finance close depends on systems that weren't built with accounting logic in mind. Stripe, Shopify, billing platforms, product telemetry, and CRM data all hold part of the answer. If they don't agree on timing, rev rec turns into manual cleanup.

That's why complex pricing should trigger an accounting review before rollout, not after the first audit comment.

Common Rev Rec Errors and Audit Red Flags

Most rev rec failures are visible long before the auditor points them out. You can usually spot them in contract files, deferred revenue schedules, or the absence of a consistent monthly process.

Red flags in your books

Here are the warning signs I'd check first:

- Annual contracts booked upfront: If you're recognizing the full value of a prepaid annual agreement on invoice date, your revenue is likely overstated and deferred revenue is understated.

- No deferred revenue rollforward: If no one can show opening balance, additions, recognitions, and ending balance by month, your books aren't audit-ready.

- Bundled deals treated as one line item: Distinct obligations need separate treatment. When finance accepts the sales package without allocation logic, errors follow.

- Contract modifications handled ad hoc: Renewals, upsells, credits, and scope changes need a consistent accounting policy.

- Revenue schedules living only in spreadsheets: Spreadsheets aren't the problem by themselves. Uncontrolled spreadsheets are.

According to RevenueHub's guidance on implementing ASC 606, failing to allocate transaction price correctly across distinct performance obligations can create significant balance sheet distortions, including misclassifying deferred revenue as current revenue, and auditors frequently detect this as a material error source during investor-ready financial package preparation.

Misconceptions that cause real problems

The most common bad assumption is “our contracts are simple.” They usually aren't.

Another one is “our tax CPA will catch it.” Tax and GAAP reporting solve different problems. If your internal reporting is weak all year, your audit prep becomes expensive cleanup.

A useful discipline is to run your own quarter-end review the way an outside party would. Teams already do this in marketing, sales ops, and disputes. The finance version is the same idea. A structured Q4 campaign audit is a good example of how disciplined reviews surface hidden process failures early. Your accounting team should apply the same mindset to contract terms, billing logic, and recognition schedules before the formal audit starts. This audit preparation checklist is a practical place to start.

Warning sign: If your controller needs to “remember how we handled that last deal,” you don't have a rev rec system. You have tribal knowledge.

Building a System for Audit-Ready Financials

Revenue recognition doesn't scale through heroics. It scales through policy, system design, and review.

What actually works

A reliable setup has four parts working together:

-

Documented policy

Your team needs written rules for subscriptions, setup fees, bundled services, discounts, credits, and contract modifications. -

Configured systems

QuickBooks, Xero, or NetSuite should reflect the policy. Stripe or Shopify data has to flow in cleanly. Product or usage data has to tie to billing and accounting periods. -

Defined ownership

Sales owns contract structure. Finance owns accounting policy. Rev ops or billing owns data flow. Problems start when everyone assumes someone else made the call. -

Monthly review controls

Reconcile deferred revenue, test new contract types, and review exceptions before closing the books.

What breaks under pressure

The weak version looks familiar:

- Billing drives accounting: The invoice layout becomes the revenue policy.

- SSPs aren't maintained: Teams can't defend how bundled revenue was allocated.

- Usage data isn't complete: Finance can't determine what was earned in the period.

- Manual workarounds pile up: Each exception gets its own tab in a spreadsheet until no one trusts the output.

A good rev rec process doesn't eliminate judgment. It makes judgment visible, documented, and repeatable.

If your stack includes NetSuite, Stripe, or another billing platform, the critical question is whether those systems are configured to support your actual contract logic. Automation helps only after you define the accounting treatment clearly.

When to Outsource Your Revenue Recognition Process

At a certain point, keeping rev rec fully in-house stops being efficient.

The trigger usually isn't company size by itself. It's complexity. If you're preparing for your first audit, raising a priced round, adding bundled contracts, introducing usage-based billing, or cleaning up legacy books, rev rec starts consuming senior finance time fast.

Outsourcing makes sense when:

- Your contracts evolved faster than your accounting process

- Your close depends on manual spreadsheets and one person's memory

- Your board or investors need cleaner monthly reporting

- Your internal team is strong operationally but thin on ASC 606 depth

- You need an objective review before diligence or audit

The mistake is treating outsourcing like loss of control. Good outsourced support gives you more control because the rules, schedules, and review process become explicit. Your team spends less time rebuilding history and more time using the numbers.

If you're weighing that move, outsourced finance support is most useful when it covers both policy and execution. This overview of outsourced controller services is a good benchmark for what to expect.

If your team is wrestling with deferred revenue, bundled contracts, or usage-based pricing, Jumpstart Partners can help you clean up the process, document the policy, and produce financials that hold up in diligence and audits. The fastest next step is a working review of your contracts, billing flows, and monthly close so you can see exactly where revenue recognition is breaking and what to fix first.