Financial Operations

Investor Due Diligence: A Founder's Guide for 2026

Navigate investor due diligence with confidence. This guide covers the timeline, data room checklist, red flags, and how to prepare investor-ready financials.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··22 min readA startup can look compliant on paper and still break under scrutiny. One often-cited example is that a 2025 study found that 68% of startups with apparent SOC 2 compliance still failed critical operational security tests during post-investment due diligence. That gap is the point.

Investor due diligence tests whether your numbers, systems, contracts, and operating habits support the story in your deck. For founders running SaaS, agencies, and service businesses in the $500K to $20M revenue range, this is often the first serious review of how the company actually works, not just how it presents.

I have seen deals slow down or lose value for reasons founders considered minor. Revenue was real, but deferred revenue was tracked inconsistently. Customers were under contract, but signatures were missing. Margins looked healthy, but service delivery costs sat in the wrong accounts. Investors read those issues as execution risk.

That is why diligence should be treated as a financial and operational proof exercise, not a file storage project. A clean data room helps, but it does not fix weak reporting, unclear unit economics, or messy controls. Strong preparation gives investors a credible explanation of how the business runs, where the risks sit, and why those risks are contained.

Founders who wait until diligence starts often end up answering preventable questions under deadline pressure. Founders who prepare early keep control of the narrative, protect valuation, and shorten the path to close. The same discipline also matters in a broader strategic analysis of M&A due diligence, where operational inconsistency can change price, terms, or buyer confidence fast.

Table of Contents

- Why Investor Due Diligence Is More Than Just a Test

- The Due Diligence Roadmap Stages and Timelines

- Building Your Investor Ready Data Room

- Proving Your Financial Story with Unit Economics

- Common Due Diligence Red Flags and How to Fix Them

- Streamline Diligence with an Outsourced Finance Partner

- Your Actionable Due Diligence Readiness Checklist

Why Investor Due Diligence Is More Than Just a Test

Investor due diligence decides whether your story survives contact with evidence. Investors aren't checking whether you've uploaded enough files. They're testing whether your company behaves like the valuation you're asking them to support.

That distinction matters. A founder says revenue is recurring, but invoices show custom one-off implementation work mixed into subscriptions. A CEO says churn is under control, but customer contracts reveal short commitments and broad termination rights. A services firm claims strong margins, but time tracking and payroll allocations don't support the gross profit story.

Practical rule: Investors fund businesses that can explain their numbers under pressure, not businesses that simply produce numbers.

The fastest way to fail diligence is to act defensive. If every request feels like an accusation, you respond slowly, over-explain, and expose weak controls. A better posture is to treat investor due diligence as a chance to show that your company is disciplined enough to scale.

That's especially true in acquisitions. If you want a sharper outside view of how buyers dissect risk across the transaction, this strategic analysis of M&A due diligence is worth reading because it highlights how diligence connects directly to valuation, deal terms, and post-close integration risk.

What actually gets judged

Investor due diligence usually answers four unspoken questions:

- Is the revenue real? Investors look for consistency across contracts, billing, collections, and recognized revenue.

- Is the margin durable? They want to know whether growth produces cash or just hides inefficiency.

- Is management in control? Sloppy close processes, undocumented approvals, and missing policies signal weak execution.

- Is there hidden risk? Cap table confusion, customer concentration, security gaps, and legal loose ends all change the deal.

A failed diligence process doesn't just cost time. It can create a credibility problem that follows you into the next conversation. Founders talk about valuation first. Investors usually decide based on operational maturity.

The Due Diligence Roadmap Stages and Timelines

Deals rarely fail because one file is missing. They fail because diligence exposes a business that does not reconcile from one function to the next.

That is why a roadmap matters. Founders who treat diligence as a document chase get dragged into reactive cleanup. Founders who understand the sequence can prepare the story underneath the files, which is what investors are really testing.

The timeline depends on deal type, deal size, and how clean the company is before diligence opens. A straightforward venture round can move in a few weeks. A complex acquisition or institutional process can run much longer, especially when investors need to reconcile financial, legal, operational, commercial, and technical risk across multiple teams.

If you want a clearer sense of what investors expect to see at each step, this guide to due diligence reports and what they need to prove is a useful reference. The common thread is simple. Speed comes from consistency, not from hustling after requests arrive.

What investors are trying to confirm

Each diligence track tests a different part of the same question: is this company investable at the price and structure being discussed?

| Category | Investor question | What passing looks like |

|---|---|---|

| Financial | Are the numbers accurate and sustainable? | Clean statements, reconciled accounts, support for revenue recognition, margins, and cash flow |

| Legal | Does the company own what it sells and comply with its obligations? | Signed contracts, current corporate records, clear IP ownership, and no material documentation gaps |

| Operational | Can the business execute without founder heroics? | Documented processes, repeatable controls, timely reporting, and visible accountability |

| Commercial | Is demand real, and can revenue hold up? | Explainable pipeline movement, customer concentration analysis, stable retention patterns, and clear churn drivers |

| Technical | Can the product and infrastructure support growth? | Maintainable code, manageable hosting costs, sensible architecture decisions, and credible security practices |

How the process unfolds in practice

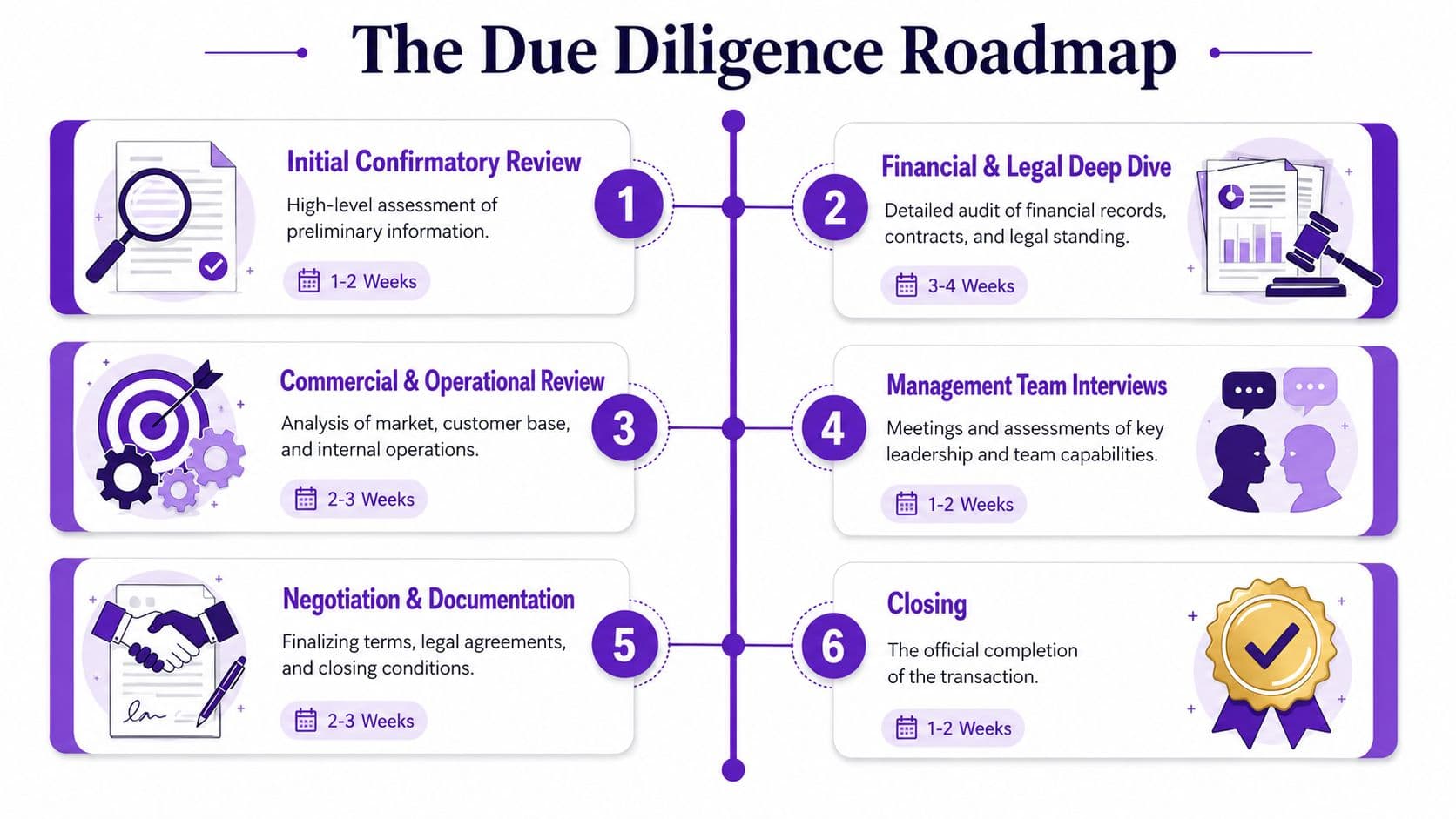

A practical diligence process tends to move through six stages.

-

Confirmatory review

Investors compare your deck, KPI definitions, financial summary, and cap table against each other. This is the first credibility test. If ARR in the pitch does not match billing records or deferred revenue, scrutiny increases fast. -

Financial and legal examination

This stage covers reconciliations, tax filings, contracts, board approvals, option grants, debt terms, and ownership records. Small gaps matter here because they suggest larger control problems. -

Commercial and operating review

Investors test how revenue is won, delivered, renewed, and supported. They look for concentration risk, pricing inconsistency, fulfillment issues, and the operational friction that weakens gross margin over time. -

Management sessions

Leadership gets similar questions in different formats. The goal is not to catch someone on style. The goal is to see whether finance, sales, product, and operations tell the same story. -

Issue resolution and deal negotiation

Findings now affect valuation, structure, and legal terms. A messy close process may lead to holdbacks. Weak revenue quality may change the multiple. Open legal items can become closing conditions. -

Signing and closing

This part feels fast only if the earlier work was disciplined. If core issues surface late, the deal slows down when everyone is least patient.

One pattern shows up in almost every rough process I have seen. The company has the documents, but the documents do not agree.

A customer contract says annual prepay. The CRM shows month-to-month. The invoice schedule does something else. Revenue is recognized on a fourth logic. At that point, diligence stops being administrative and becomes a trust problem.

Founders should plan for that reality. Build a two-track timeline. One track handles document collection. The other resolves inconsistencies across finance, legal, sales, and operations before investors find them for you. That preparation does more than shorten diligence. It protects valuation and keeps the conversation focused on company value instead of cleanup.

Building Your Investor Ready Data Room

A data room can help or hurt a deal faster than founders expect. In a clean process, it speeds answers and builds confidence. In a messy one, it exposes weak reporting, loose controls, and gaps between what management says and what the records support.

The goal is not to upload every file the company has. The goal is to make your business legible under pressure.

For founder-led companies, I recommend organizing the room into five core folders: financials, legal and corporate, intellectual property, commercial and customers, and team. That structure is familiar to investors and practical for internal teams. More important, each folder should answer a clear diligence question without forcing the investor to schedule a call just to understand basic context.

Build the room around investor questions

Start with financials. They carry the most weight, and they expose operational discipline faster than any other folder.

Investors typically ask for historical financial statements, recent management accounts, tax filings, forecasts with assumptions, cap table detail, debt schedules, working capital support, revenue breakdowns, margin analysis, cash flow reporting, and deferred revenue or backlog schedules. The request list may look administrative. It is not. Investors use it to test whether your numbers hold together across billing, collections, revenue recognition, and cash.

That is why a strong data room is more than a checklist. It is the operating story behind the checklist. If revenue grew, show what drove it. If gross margin moved, show whether the change came from pricing, delivery mix, headcount, or vendor costs. If cash conversion weakened, make the cause visible before someone asks.

Essential Data Room Document Checklist

| Category | Document Request | Why Investors Ask for It |

|---|---|---|

| Financials | Monthly P&L, balance sheet, cash flow statement | To test reporting accuracy, margin quality, and cash discipline |

| Financials | Revenue bridge by product, customer, or service line | To understand what is recurring, what is project-based, and what is concentrated |

| Financials | Accounts receivable and deferred revenue schedules | To verify collections, timing, and revenue recognition |

| Financials | Forecast with assumptions | To see whether management understands the operating drivers behind growth |

| Legal and Corporate | Incorporation documents, board consents, shareholder records | To confirm ownership, authority, and governance |

| Legal and Corporate | Cap table and option records | To identify dilution issues, promised equity, and closing risk |

| Legal and Corporate | Material contracts and debt agreements | To surface restrictions, obligations, and change-of-control issues |

| Intellectual Property | IP assignments, trademarks, software ownership records | To confirm the company owns the assets investors think they're funding |

| Commercial and Customers | Top customer contracts, renewal terms, pipeline summary | To assess revenue durability and concentration risk |

| Commercial and Customers | Pricing sheets and churn analysis | To understand whether growth is healthy or subsidized |

| Team | Org chart, key employee agreements, incentive plans | To judge execution depth and retention risk |

If you want a clearer view of how findings get turned into investor-facing materials, this guide to due diligence reports and what they should include is a useful reference.

Presentation matters as much as completeness

A disorganized data room sends a clear message. Finance is behind. Leadership is not reviewing the same numbers. Risk still sits inside the business instead of being surfaced and managed.

Presentation fixes are simple, but they matter. Use a consistent file naming convention. Date every file. Add a short readme at the top of each folder with the reporting period, the source system, and any exceptions an investor should know before reviewing the files. If a revenue recognition policy changed, explain when and why. If one enterprise contract has custom terms, flag it and include the effect on billing or margin.

That level of preparation changes the tone of diligence. Investors stop spending time on basic clarification and start spending time on business quality.

Use this standard:

- Use reconciled reporting packs: The P&L should tie to the balance sheet and cash flow statement.

- Add short narrative notes: Explain one-time expenses, large variances, customer losses, or unusual gross margin movement.

- Separate source data from finished schedules: Keep CRM exports, billing exports, and cleaned support files in different subfolders.

- Control permissions in stages: Sensitive files do not need to be available on day one if the process has not reached that level.

- Show version control: If a forecast changed, label the current version clearly and archive prior versions so no one works from the wrong file.

Founders often treat the data room as an admin task to finish after the business is built. In practice, it is a live test of whether the company can defend its own numbers. Clean folders help, but consistency across systems is what protects valuation.

Proving Your Financial Story with Unit Economics

Investors don't fund revenue in the abstract. They fund revenue that converts efficiently, retains value, and scales without destroying margin. That's why unit economics sits at the center of investor due diligence for SaaS and increasingly for agencies and services firms with recurring contracts.

For SaaS, one benchmark matters immediately. According to FE International's SaaS due diligence benchmark guide, Customer Lifetime Value to Customer Acquisition Cost should be at least 3:1. Below that threshold, investors start asking whether growth is creating value or just consuming cash.

A worked LTV to CAC example

Use a simple worked example.

Assume your average customer pays $1,200 per month. Your gross margin on that revenue is 80%. Average customer lifetime is 24 months. Then:

- CLTV = $1,200 × 80% × 24

- CLTV = $23,040

Now assume you spent $180,000 on sales and marketing tied to new acquisition in the period, and you added 60 new customers.

- CAC = $180,000 ÷ 60

- CAC = $3,000

Now calculate the ratio:

- CLTV:CAC = $23,040 ÷ $3,000

- CLTV:CAC = 7.68:1

That's comfortably above the 3:1 benchmark cited above. The metric tells a clean story. Your average customer produces enough gross profit over time to justify the upfront acquisition cost.

If the same company had a shorter lifetime, lower margin, or bloated paid acquisition spend, the result changes fast. For example, keep CLTV at $23,040? No. You can't assume that. Recalculate each driver accurately. Investors always do.

Show the inputs, not just the result. A ratio without assumptions looks manufactured.

If you need a practical refresher on how founders and finance teams structure these metrics, this breakdown of unit economics and how to use them is a solid operational reference.

How reporting quality changes valuation

The same FE International source notes that SaaS companies under $5M in revenue are typically valued using SDE multiples of 2.5x to 4x, while companies above $5M often shift to EBITDA multiples of 8x to 11x. That change isn't cosmetic. It reflects how buyers and investors view operational maturity.

Here's a worked comparison using the verified examples from that source:

| Company profile | Metric used | Multiple range | Implied valuation |

|---|---|---|---|

| SaaS business with $3M revenue and $600K SDE | SDE | 2.5x to 4x | $1.5M to $2.4M |

| SaaS business with $10M revenue and $2M EBITDA | EBITDA | 8x to 11x | $16M to $22M |

The lesson isn't that bigger automatically means better. The lesson is that cleaner reporting supports stronger pricing. If your EBITDA adjustments are vague, deferred revenue is wrong, or implementation labor is buried inconsistently, investors won't give you the high end of any range. They'll haircut the number or change the basis entirely.

What founders get wrong

The common objection is simple: "Our books are messy, but the business is strong."

Sometimes that's true. Investors still discount it.

Three issues show up repeatedly:

- You rely on a tax-basis P&L for an investor conversation. Tax reporting and diligence reporting are not the same thing.

- You present growth without segmentation. Investors need to know what part of growth is recurring, project-based, upsell, or one-time.

- You defend the model instead of reconciling it. If the CRM, billing system, and general ledger disagree, finance has to resolve that before diligence.

Messy books don't just create more work. They weaken the credibility of every KPI built on top of them.

Common Due Diligence Red Flags and How to Fix Them

Deals rarely fall apart because of a single dramatic discovery. They stall because routine operating gaps start connecting into a pattern. An investor sees one unreconciled balance, then an unsigned customer agreement, then a KPI that does not tie to the general ledger. At that point, the concern is no longer the individual issue. It is whether management has genuine control of the business.

That is the standard in diligence. Investors are testing whether your financial and operating story holds up under pressure, not whether you uploaded enough files.

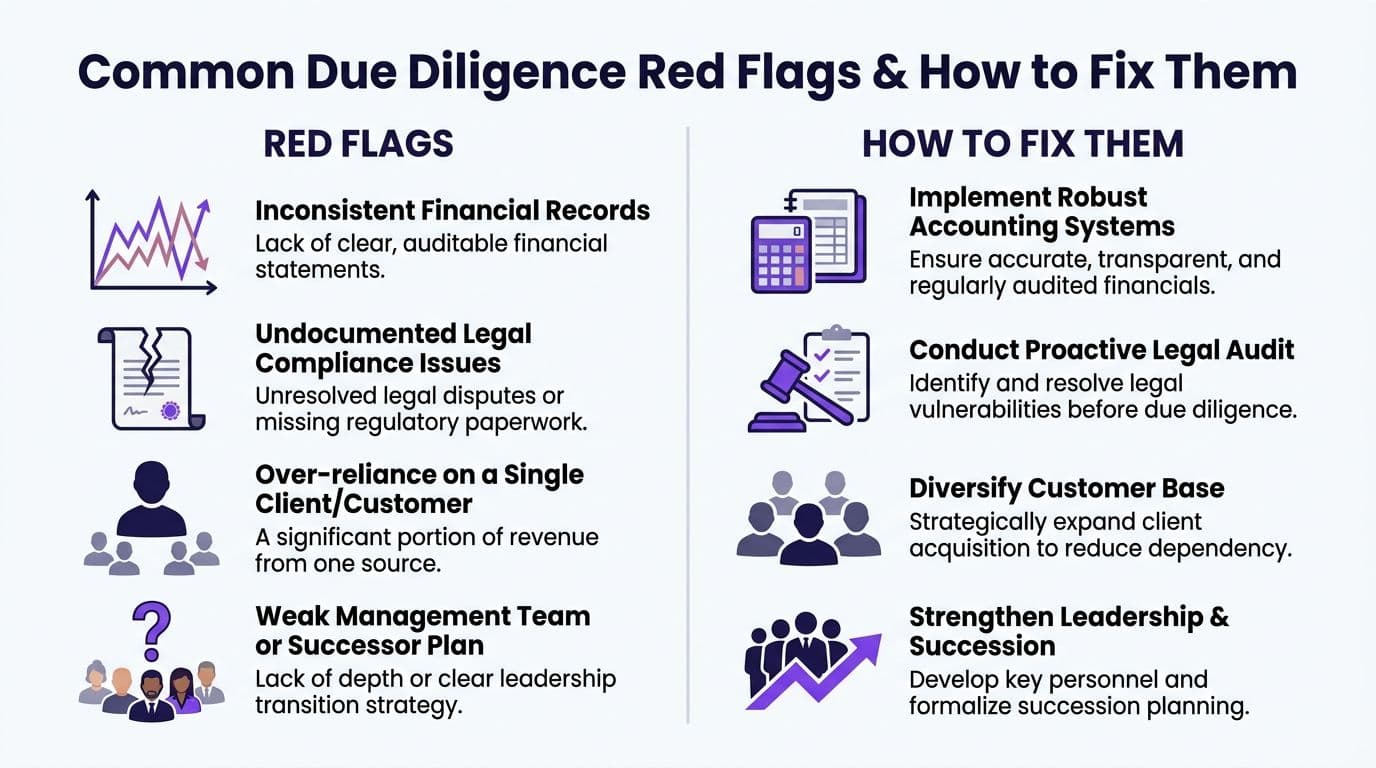

The red flags investors react to fastest

| Red flag | Why it hurts the deal | Immediate fix |

|---|---|---|

| Inconsistent financial records | Investors cannot trust margin, cash movement, or reported earnings | Reconcile bank, AR, AP, payroll, and revenue schedules before opening the data room |

| Messy cap table | Ownership uncertainty can delay closing or force legal cleanup late in the process | Formalize grants, board approvals, and historical issuances with counsel |

| Customer concentration | Revenue looks fragile when too much depends on one account | Prepare a concentration memo, renewal history, and a credible diversification plan |

| Weak contract hygiene | Unsigned MSAs and vague SOWs create enforceability risk and pricing confusion | Standardize templates and collect executed copies in one controlled repository |

| Claimed compliance without evidence | Security and vendor risk move from manageable to speculative | Document how controls operate, who reviews vendors, and what happens when incidents occur |

| Founder-only knowledge | Key-person risk increases if nobody else can explain how the company runs | Write process documentation, define role ownership, and assign backup coverage for critical workflows |

A common founder mistake is treating these as admin issues. They are valuation issues.

For example, customer concentration is not always a deal problem. Plenty of good companies have one large account. The red flag appears when management cannot explain the contract term, renewal pattern, gross margin profile, expansion path, or what happens if that customer slows spend. The same principle applies to compliance claims. Saying the company is secure does not help. Showing access reviews, policy enforcement, vendor oversight, and incident logs does.

Model quality also gets exposed fast during diligence. If assumptions change between the board deck, forecast, and cash plan, investors assume the team is still guessing. Founders who need to tighten logic, align scenarios, or present assumptions more clearly can use this primer on financial modelling for UK finance careers as a practical reference for how disciplined models are built and reviewed.

A short explainer on diligence red flags is useful here:

Fix the issue before the investor asks

The best approach is to identify weak points early, quantify them, and frame them on your terms. Investors usually accept a known problem with a credible remediation plan. They discount companies that appear surprised by their own records.

Use this sequence:

- Stabilize the numbers first: Complete reconciliations, lock reporting periods, and remove manual journal entries that do not have support.

- Run a contract sweep: Pull customer and vendor agreements into one folder structure and tag each one as signed, expired, amended, or non-standard.

- Write exception memos: If there is customer concentration, a pending dispute, a one-time margin swing, or a revenue recognition judgment, explain it clearly with facts and next steps.

- Test every compliance claim: Gather policies, screenshots, access logs, vendor review records, and evidence that controls are performed.

- Review earnings quality internally: A buyer will examine recurring revenue, margin normalization, cutoff accuracy, and add-backs. An internal review using a quality of earnings framework for diligence helps surface issues before they become investor objections.

One more practical point. Founders often try to answer every diligence question live on a call. That usually makes things worse. If support is incomplete, say you will confirm and follow up with documentation. Clean follow-up builds credibility. Improvised answers create new work and new risk.

Investors can work with an imperfect business. They struggle to work with an unclear one.

Streamline Diligence with an Outsourced Finance Partner

Diligence gets expensive when your core finance function is reactive. Founders feel that pressure first. The controller is chasing reconciliations, the CEO is answering basic reporting questions, and nobody has time to run the business.

That's the point where an outsourced finance partner stops being administrative help and starts becoming infrastructure.

What an external finance team actually solves

A capable external team brings order to the parts of diligence that usually break first:

- Month-end close discipline: Clean closes create confidence in every report that follows.

- Revenue recognition consistency: SaaS and hybrid services businesses need clear treatment for subscriptions, implementation, and deferred revenue.

- KPI integrity: MRR, ARR, CAC, gross margin, and cash burn all need a data trail back to source systems.

- Data room preparation: Reports, schedules, and support files need to be produced in a format investors can effectively use.

If you're evaluating options, one example is finance and accounts outsourcing for growing companies, where outsourced controller and bookkeeping support is used to produce investor-ready reporting, improve close cadence, and support diligence preparation.

What good support looks like in practice

The standard isn't fancy reporting. It's dependable reporting.

A strong outsourced setup should give you current financials, clear reconciliations, documented policies, and a finance owner who can respond to diligence questions without rebuilding the file from scratch. For businesses with subscription revenue, payroll-heavy delivery, or multi-system billing, that matters more than another dashboard.

"Investors aren't just buying your product; they're investing in your operational maturity. Clean, real-time financials aren't a 'nice-to-have', they are the primary indicator of a well-run company. A team that outsources this to experts like Jumpstart signals they're focused on growth, not just surviving."

Sarah Chen, Partner at Growth Equity Ventures.

The misconception here is that outsourced finance is only for companies that aren't developed enough to hire in-house. In practice, it's often the opposite. Smart operators use external specialists when they need cleaner execution before they need a full internal department.

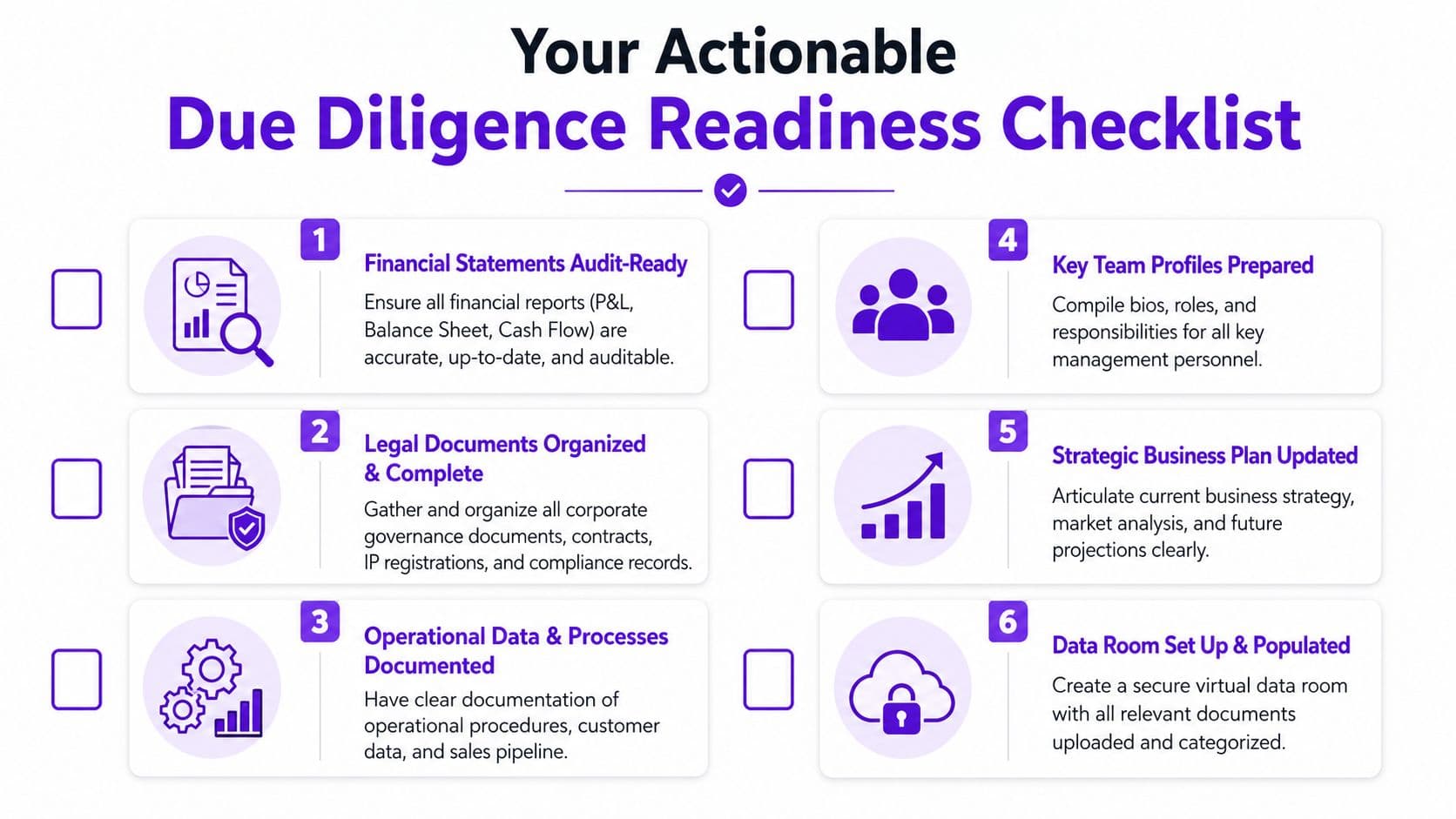

Your Actionable Due Diligence Readiness Checklist

Diligence readiness doesn't start when the term sheet arrives. It starts when you decide your numbers and operations need to hold up under third-party review.

Use the next ninety days well.

Next 30 days

- Clean historical bookkeeping: Reconcile cash, revenue, payroll, debt, and major balance sheet accounts.

- Centralize company records: Gather contracts, cap table files, tax documents, and board approvals.

- Define your KPI set: Decide which metrics management and investors will both rely on.

Days 31 to 60

- Build management reporting: Monthly P&L, balance sheet, cash flow, KPI dashboard, and commentary package.

- Test your financial narrative: Make sure your revenue mix, margin profile, and forecast assumptions all align.

- Document operational controls: Write down key approval, billing, collections, and security procedures.

Days 61 to 90

- Populate the data room: Upload final documents with naming standards and folder logic.

- Run a mock diligence review: Have someone challenge inconsistencies across contracts, systems, and reports.

- Assign owners for follow-up: Every likely investor question should have a clear internal owner.

If you want a practical companion document for this phase, use this financial due diligence checklist for growing businesses to turn the work into an internal project plan.

If your team is preparing for fundraising, acquisition talks, or a lender review, Jumpstart Partners can help you clean up reporting, organize your data room, and build the financial narrative investors expect to see.