Financial Operations

What Is the Contribution Margin

Understand what is the contribution margin, how to calculate it for SaaS & service businesses, & use it to boost pricing & profitability in 2026.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··14 min readContribution margin is the revenue left from each sale after subtracting all variable costs directly tied to that sale. It's the cash each sale generates to pay fixed costs and then produce profit.

Most founders think they know this metric because they can repeat the textbook formula. Most are still calculating it wrong.

Your P&L can show growth while your cash position gets worse. That usually happens because you're watching revenue, gross margin, or total net income, while ignoring the cost of making one more sale happen. In digital businesses, those costs often hide in plain sight: payment processing, fulfillment, usage-based software, contractor labor, channel-specific ad spend, and platform fees.

That's why contribution margin is the metric I trust most when I'm advising a founder on pricing, hiring, channel mix, and whether growth is helping. It strips away accounting noise and answers the question that matters: if you sell one more unit, sign one more client, or add one more customer, how much money is really left?

Why Your Profit and Loss Statement Is Lying to You

A standard P&L is useful for compliance and historical reporting. It's weak as an operating dashboard.

If you're a SaaS founder, agency owner, or services CEO, your P&L groups expenses in ways that hide bad decisions. You can post stronger revenue, celebrate a healthy gross profit line, and still lose ground because the variable costs tied to each sale are rising faster than you realize.

The problem with blended reporting

Your P&L usually tells you what happened last month. It doesn't tell you whether the next sale helps or hurts.

A founder sees revenue climbing and assumes scale is working. Then the bank balance says otherwise. The reason is simple: contribution margin is a predictive metric, while total profit is a lagging one. If your contribution margin is thin or miscalculated, scaling just means you're scaling stress.

Practical rule: If you can't explain the variable cost of one more customer, one more project, or one more order, you don't understand your business model yet.

This gets worse in channel-heavy businesses. A D2C brand selling through Shopify, Amazon, and wholesale doesn't have one economic model. It has several. If you're evaluating channels like Amazon FBM for D2C brands, you need a margin view that reflects the true cost to fulfill and transact in that channel, not just a top-line sales number.

Why founders get misled

Most finance reports are built for accountants first and operators second. That's why founders often need a cleaner operating lens than a standard income statement provides. If you want a refresher on where the usual P&L layout helps and where it falls short, this guide on how to read an income statement is worth reviewing.

The hard truth is that a business can look busy, look valuable, and still have weak contribution economics. That's not a bookkeeping problem. It's a decision-making problem.

Contribution Margin Explained Without the Jargon

If you're asking what is the contribution margin, use this definition:

Contribution margin is the amount left after you subtract variable costs from revenue. That leftover amount contributes to fixed costs first, then profit.

The simple formula

There are two versions you should know:

- Contribution margin in dollars = Revenue − Variable costs

- Contribution margin ratio = Contribution margin ÷ Revenue

The dollar amount tells you how much cash is left from a sale or customer. The ratio tells you how efficient that sale is.

A simple analogy helps. Think about a coffee shop.

If a customer buys a drink, the beans, milk, cup, lid, and card fee all increase because of that sale. Rent doesn't. The manager's base salary doesn't. The espresso machine lease doesn't. The sale contributes something after the variable costs, and that amount helps cover those fixed expenses.

That's contribution margin.

Contribution margin versus gross margin

Founders mix up gross margin and contribution margin constantly. They are not interchangeable.

| Metric | Formula | What It Measures | Best For |

|---|---|---|---|

| Contribution Margin | Revenue minus variable costs | Cash left after costs directly tied to the sale | Pricing, break-even, channel decisions |

| Gross Margin | Revenue minus cost of goods sold | Production or delivery economics at a high level | Financial reporting, supplier or delivery efficiency |

Gross margin usually stops too early for operating decisions. Contribution margin goes further by isolating what changes with each sale.

Gross margin tells you the product or service looks viable. Contribution margin tells you whether selling more of it is smart.

If you need the accounting foundation beneath these formulas, keep this reference on basic formulas of accounting close. It helps clean up a lot of confusion around what belongs in which profitability metric.

What counts as a variable cost

This is the part founders get wrong.

A variable cost is any cost that moves because you made that sale. In a digital business, that can include things many teams incorrectly leave below the line:

- Payment fees

- Freelancer or contractor labor tied to delivery

- Fulfillment or shipping handling

- Channel-specific direct ad spend

- Usage-based software or infrastructure

- Transaction fees or marketplace fees

A fixed cost stays in place whether you make the sale or not. Your office lease doesn't increase because one more customer signs. Your full-time finance manager's salary doesn't change because a single project closes.

That distinction matters more than the formula itself.

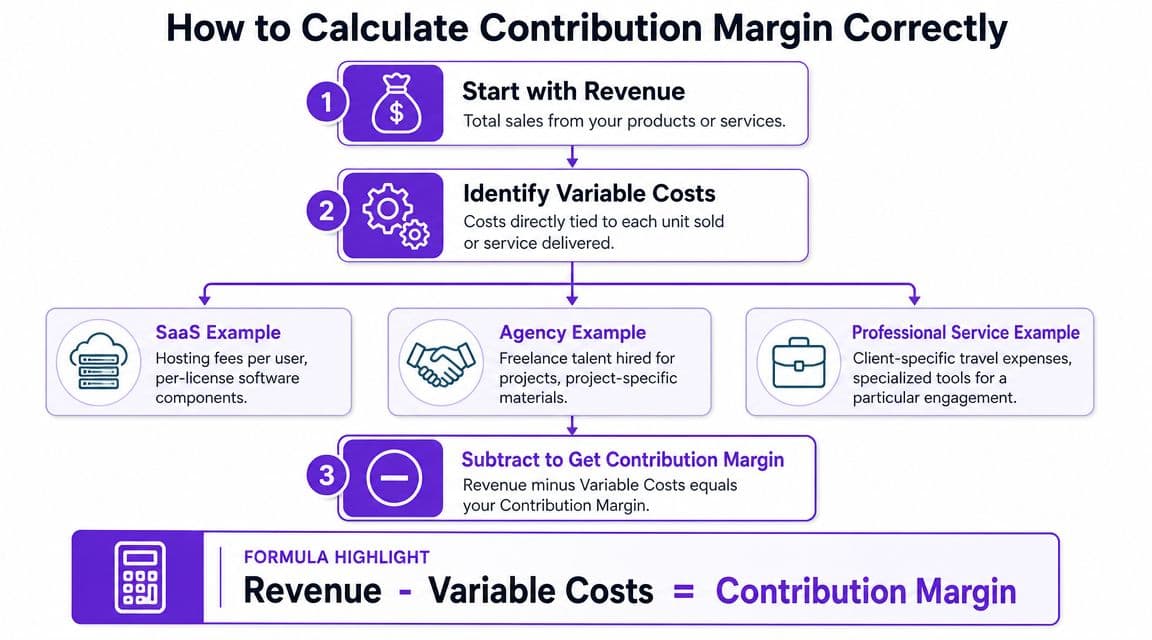

How to Calculate Contribution Margin Correctly

The formula is easy. The classification work is where finance teams earn their keep.

For modern digital businesses, it's critical to use net sales, not gross sales. Recent e-commerce guidance specifically notes that net sales should exclude taxes, returns, and shipping charges collected, and that variable costs can include payment fees, freight, fulfillment, and direct ad spend. Using gross sales can overstate margin and distort break-even analysis, especially for Shopify or Amazon sellers, as explained in Wayflyer's discussion of contribution margin over revenue.

Start with the right revenue number

Use this structure:

| Step | What to include |

|---|---|

| Net sales | Revenue after removing taxes, returns, and shipping charges collected |

| Minus variable costs | Only costs that rise because of the sale |

| Result | Contribution margin |

If you start with gross cash collected, your margin is inflated from the first line.

Worked example for SaaS

Say you run a SaaS product with one customer paying $1,200 annually.

Variable costs tied to that customer:

- Payment processing: $36

- Usage-based hosting and infrastructure: $120

- Third-party per-user software cost: $84

- Support labor directly tied to usage volume: $180

Contribution margin calculation:

- Revenue: $1,200

- Total variable costs: $420

- Contribution margin: $780

- Contribution margin ratio: 65%

The common mistake is leaving support and infrastructure entirely in overhead. If those costs rise with customer volume, part of them belongs in contribution margin.

Jason Lemkin put the broader principle clearly: “Unit economics are the truth serum for SaaS businesses. You can have beautiful growth charts and impressive MRR, but if you're spending $15,000 to acquire customers who only generate $12,000 in lifetime value, you're just a very efficient cash-burning machine.” Read the original quote at SaaStr.

Before you go deeper, it also helps to separate gross margin from contribution margin cleanly. This overview of how to calculate gross margin is useful because many teams blend the two.

Worked example for a digital agency

An agency signs a website project for $20,000.

Variable costs:

- Freelance designer hired specifically for the project: $4,500

- Freelance developer hours: $5,500

- Project-specific software and stock assets: $500

- Payment fee: $600

Calculation:

- Revenue: $20,000

- Total variable costs: $11,100

- Contribution margin: $8,900

- Contribution margin ratio: 44.5%

Your account manager's salary is not variable if they're salaried and not hired per project. Your rent is not variable. Your retainer-based strategy lead is not variable unless their cost scales per engagement in a direct, traceable way.

Worked example for e-commerce

A store sells an order with $150 in net sales.

Variable costs:

- Product cost: $45

- Freight: $10

- Fulfillment: $12

- Payment fee: $5

- Direct ad spend allocated to that order: $28

Calculation:

- Net sales: $150

- Total variable costs: $100

- Contribution margin: $50

- Contribution margin ratio: 33.3%

This is why contribution margin helps you drive smarter business decisions than top-line revenue ever will. Revenue tells you activity. Contribution margin tells you whether that activity deserves more budget.

A quick video walkthrough can help if you want the visual version of the math:

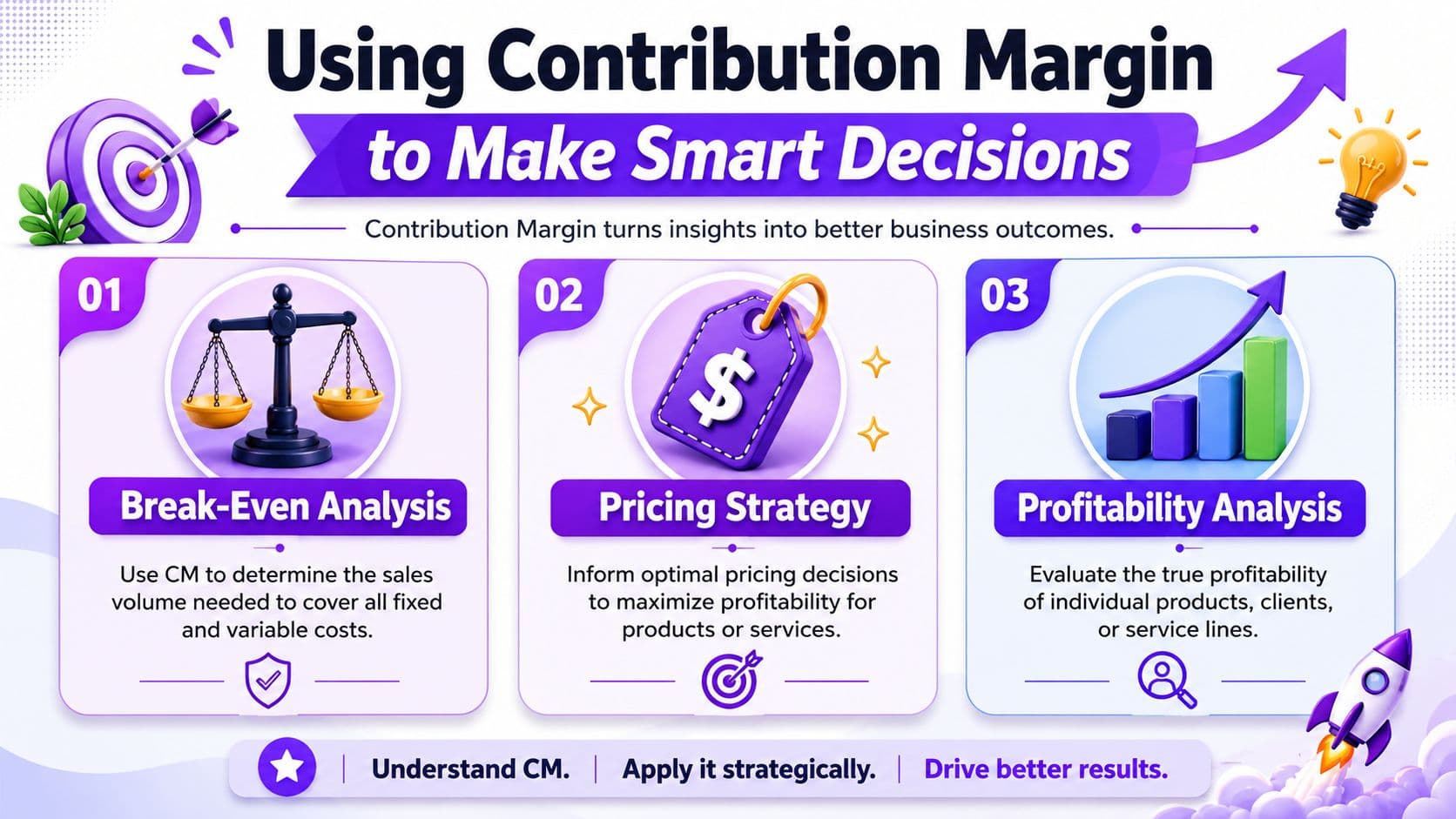

Using Contribution Margin to Make Smart Decisions

A metric matters only if it changes decisions. Contribution margin does.

Break-even analysis that actually helps

The formula is straightforward:

Break-even point in units = Fixed costs ÷ Contribution margin per unit

Say your service line has fixed monthly costs of $30,000 and each project contributes $6,000 after variable delivery costs.

- Fixed costs: $30,000

- Contribution margin per project: $6,000

- Break-even volume: 5 projects

That's useful. It tells you the minimum sales volume required before that service line starts funding the business instead of draining it.

Pricing decisions with teeth

Pricing shouldn't start with what competitors charge. It should start with your variable cost floor.

If your agency sells a recurring marketing package for $4,000 per month and direct delivery labor, software, and transaction costs total $2,800, your contribution margin is $1,200. If that leftover amount can't support overhead and target profit, the price is wrong, the scope is wrong, or the client is wrong.

Decision test: If a higher-priced offer produces less contribution because delivery complexity rises faster than price, you don't have a premium offer. You have a premium headache.

Product, client, and channel analysis

The best use of contribution margin is comparison.

A SaaS company can compare self-serve customers against sales-led customers. An agency can compare fixed-fee builds against ongoing retainers. An e-commerce brand can compare Amazon, Shopify, and wholesale.

One practical extension is customer retention. If one acquisition channel brings in customers who churn quickly, the contribution story changes fast. That's why tools like Unchurn's Churn Report are useful in a broader unit-economics review. Margin and churn belong in the same conversation.

If you want a larger framework for connecting acquisition, retention, and profitability, this guide on what is unit economics is the right next read.

Scenario analysis under volatility

Contribution margin becomes a management tool, not just an accounting metric.

Recent manufacturing guidance argues that teams should recalculate contribution margins under different tariff or cost scenarios to identify which products can absorb shocks and which require price changes. That means looking at margin by product, channel, and scenario, not relying on one company-wide average, as described in WISS's article on contribution margin in manufacturing operations.

The same logic applies outside manufacturing.

If your SaaS infrastructure cost rises, your margin changes. If contractor rates increase, your agency margin changes. If marketplace fees or fulfillment costs jump, your e-commerce margin changes. A static margin number is useless in a volatile business.

Four Practical Ways to Improve Your Contribution Margin

You improve contribution margin by pulling a short list of levers. Don't overcomplicate it.

Raise price where the market already says yes

Founders underprice because they fear churn, sales friction, or uncomfortable conversations. Meanwhile they keep serving low-margin work.

- Repackage offers: Bundle faster turnaround, reporting, or strategic access into higher tiers.

- Review legacy pricing: Old clients often sit on stale rates that no longer reflect delivery cost.

- Control scope tightly: In services, weak scoping destroys margin faster than almost anything else.

Cut the variable costs that hide in subscriptions and workflows

You don't need a restructuring project. You need a line-by-line audit.

Look first at payment processors, contractor utilization, usage-based cloud costs, project-specific software, and marketplace fees. In many companies, finance teams treat these as background noise because no single charge looks large. Together they often define the margin profile.

When a cost scales with customer count, order volume, or project load, finance needs to test whether it belongs above the contribution line.

Change what you sell, not just how efficiently you sell it

A lower-margin offer with high sales volume can still make sense. But many founders are pushing the wrong mix because they're measuring closed revenue instead of contributed dollars.

Ask your sales team better questions:

- Which offer closes fastest but consumes the most delivery labor?

- Which client type requests the most unbilled work?

- Which package attracts the cleanest customers and fewest support headaches?

That analysis usually reveals obvious winners and losers.

Improve operational efficiency in delivery

For agencies and professional services firms, margin improvement often starts in operations, not pricing.

Tighter project management reduces rework. Better client onboarding reduces custom exceptions. Cleaner handoffs cut delivery labor. If you need support operationalizing that reporting, Jumpstart Partners is one option for outsourced controller work that includes cleaner financial visibility for SaaS, agencies, and services firms.

If you want a broader profit improvement checklist, this guide on how to improve profit margins is a practical companion.

Contribution Margin Red Flags You Cannot Ignore

If your margin analysis shows the wrong answer, the problem usually isn't math. It's classification.

Signs your number is wrong

| Symptom | Likely issue |

|---|---|

| Revenue rises but cash stays tight | Variable costs are understated |

| Every product looks healthy | You're using a blended company-wide average |

| Margin changes wildly month to month | Costs are misclassified or allocated inconsistently |

| Discounts and refunds keep surprising you | Revenue is being measured incorrectly |

The mistakes I see most often

- Using gross sales instead of net sales: If returns, taxes, or shipping collections stay in revenue, your margin is inflated.

- Treating fixed labor as variable: A salaried manager doesn't become a variable cost because they're busy.

- Ignoring channel-specific costs: Marketplace fees, payment fees, and direct ad spend often get buried in operating expenses.

- Using one blended margin for everything: One service line can subsidize another and hide the problem.

- Failing to update the model after changes: New pricing, vendor terms, or delivery methods should trigger a recalculation.

A contribution margin model is only useful if it changes when your business changes.

That quote from Jason Lemkin earlier applies here too. SaaS founders in particular can mistake growth for health if acquisition and delivery economics are weak. The ugly version of that story is fast growth with structurally bad unit economics.

Turn Margin Insights into Profitable Growth

If you're still asking what is the contribution margin, the shortest useful answer is this: it's the clearest measure of whether your next sale helps fund the business or drains it.

This is why I push founders to stop managing from revenue and start managing from contribution. It sharpens pricing. It improves hiring decisions. It exposes weak clients, weak channels, and weak offers. It also gives you a much cleaner break-even model when markets shift and costs move.

Most companies don't need more reporting. They need better classification, better visibility by product or client, and tighter financial discipline around variable costs.

If you're still running the business off a high-level P&L, you're leaving money on the table.

If you want a cleaner view of true profitability, talk to Jumpstart Partners. They help SaaS companies, agencies, and service businesses build accurate financials, faster closes, and KPI reporting that makes contribution margin useful in real decisions, not just monthly bookkeeping.