Financial Operations

Articles of Incorporation in Arizona

File your Articles of Incorporation in Arizona correctly. Covers fees, agents, publication, & post-filing steps for audit-ready businesses.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··17 min readMost founders expect the risky part of incorporation to be choosing the entity type. In Arizona, the larger operational risk often shows up after the state accepts your filing. If you miss the state's publication step, your corporation's legal standing can be voided, which puts liability protection, diligence readiness, and fundraising timing at risk, as noted by Northwest Registered Agent's Arizona corporation guide.

That's why I don't treat articles of incorporation in Arizona as clerical setup. I treat them as the first audit and governance file your company creates. If you're a SaaS founder, agency owner, or finance lead building toward lender review, customer diligence, or an equity round, Arizona's process affects more than legal status. It affects whether your cap table, board actions, disclosure history, and compliance calendar hold up when someone serious starts asking for documents.

Table of Contents

- Why Arizona Incorporation Is More Than a Formality

- Preparing Your Arizona Articles of Incorporation

- Navigating Arizona's Mandatory Publication Requirement

- How to File Your Articles and What It Costs

- Common Filing Mistakes That Cause Rejection

- Post-Filing Compliance for Audit-Ready Businesses

Why Arizona Incorporation Is More Than a Formality

Arizona catches founders off guard because the filing itself looks inexpensive and straightforward, yet the state expects follow-through that many companies don't manage well under growth pressure. A founder who treats incorporation like a one-time form submission usually discovers the problem later, when a bank, investor, insurer, or acquirer asks for proof that the corporation was formed and maintained correctly.

A clean Arizona corporation file supports three things executives care about. First, it preserves liability protection. Second, it creates a reliable governance trail. Third, it reduces friction when outside parties review your company. If you want a grounded refresher on the core legal role of formation documents, Mayo Law on business legal essentials is a useful companion read.

Investor readiness starts at formation

Investors and auditors don't just ask whether you incorporated. They ask whether your records are internally consistent. That means your articles, statutory agent details, disclosure documents, board actions, and share issuance records need to line up.

A messy formation file creates downstream accounting headaches too. If your equity records are incomplete, your legal entity timeline becomes harder to reconcile with payroll setup, founder vesting, reimbursements, and tax filings. That's one reason some teams restructure early, such as through an LLC conversion to C corporation analysis, before outside capital enters the picture.

Practical rule: If a future investor, bank underwriter, or buyer can't verify your formation history from your records in one sitting, your incorporation process wasn't finished when the state stamped your documents.

The Arizona-specific issue founders underestimate

Arizona's process has a compliance character that finance leaders should take seriously. It isn't enough to be legally formed on paper. You need a defensible record that shows your company followed the state's required sequence and retained the proof.

That's the difference between a corporation that looks real and one that's operationally reliable. For growing SaaS and service businesses, that distinction matters when a diligence list lands in your inbox with requests for articles, bylaws, disclosures, board approvals, stock records, and proof of good standing.

Preparing Your Arizona Articles of Incorporation

A clean Arizona filing package does more than get a corporation approved. It creates the baseline records your finance team will rely on for bank onboarding, stock issuance, insurance applications, and later diligence.

Build the packet before you touch the filing portal

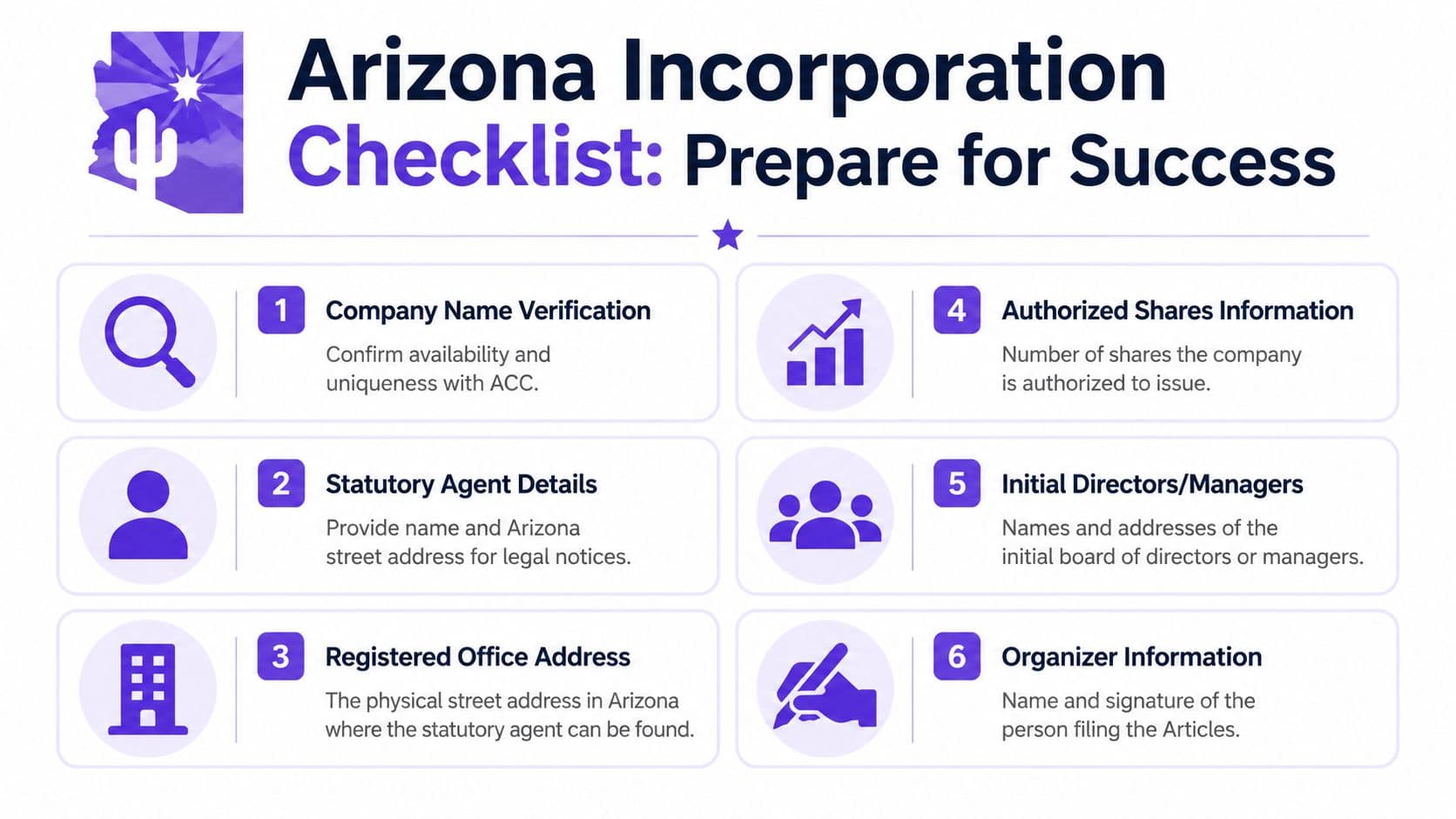

Arizona expects the filing set to be internally consistent on day one. For a standard for-profit corporation, that usually means the Cover Sheet, Articles of Incorporation (Profit), Statutory Agent Acceptance Form (M002), and Certificate of Disclosure should be drafted, reviewed, and ready as one package.

That sequence matters for control, not just convenience. If the articles say one thing, the disclosure says another, and the agent form carries a slightly different legal name or address, the problem does not end with a state rejection. It creates a broken paper trail that has to be cleaned up before counsel, lenders, or auditors can rely on the file.

The statutory agent entry deserves close review. Arizona expects a real street address for service of process, and the name and address should match the agent's acceptance exactly. A mismatch here creates a practical risk. Legal notices, tax correspondence, or lawsuit papers can miss the company, and the record will show that the formation team created the gap.

Use a pre-filing review checklist addressing the operational facts behind the documents:

- Corporate name: Match the legal name exactly across the articles, agent form, disclosure, stock ledger setup, and EIN application materials.

- Statutory agent details: Confirm the agent has accepted the appointment and that the Arizona street address is complete and current.

- Character of business: Describe what the company sells or delivers so the formation record aligns with revenue activity, insurance underwriting, and bank compliance reviews.

- Capital structure: Set the authorized share count intentionally, with enough room for founder equity, option pool planning, and early financing without an immediate amendment.

- Certificate of Disclosure: Review every answer against founder, director, and officer background facts before anyone signs.

- Incorporator and director information: Make sure names, titles, dates, and signatures line up with the organizational actions you will adopt right after filing.

What finance leaders should verify before submission

The business description is not filler. It becomes part of the company's formation record, and third parties often compare it against how cash comes in. A SaaS company should describe its software subscription activity clearly. A services firm should state the service line with enough precision that a bank underwriter or investor can understand the operating model without guessing.

The Certificate of Disclosure deserves the same level of care. Arizona asks for background disclosures because the state wants transparency around the people controlling the entity. From a finance perspective, that document also affects diligence readiness. If a disclosure issue surfaces later and the filing record looks incomplete or inconsistent, the cleanup can spill into financing timelines, M&A diligence, and internal control reviews.

Professional services firms need an extra review before filing. If the business will provide licensed services, the team should confirm whether a Professional Corporation structure is required and whether ownership and governance restrictions could affect future fundraising or equity grants. That decision has downstream consequences for cap table design and who can legally hold decision-making authority.

I also want clear ownership of the draft set before submission. One person should control versioning, one person should confirm signature authority, and one final reviewer should test the packet against the company's finance setup. Teams that formalize that process early usually spend less time fixing formation records later. If your team needs a model, this scalable legal document system is a practical starting point.

Keep the signed final set in the same corporate records folder as board consents, the initial stock ledger, and officer appointments. That makes it much easier to prove authority later through supporting documents such as this certificate of incumbency reference guide.

Navigating Arizona's Mandatory Publication Requirement

Publication is the Arizona rule that catches companies that treat formation like a one-time filing. For a scaling SaaS or service business, this is a records-control issue with real diligence consequences, not a newspaper formality.

Why this step matters in diligence

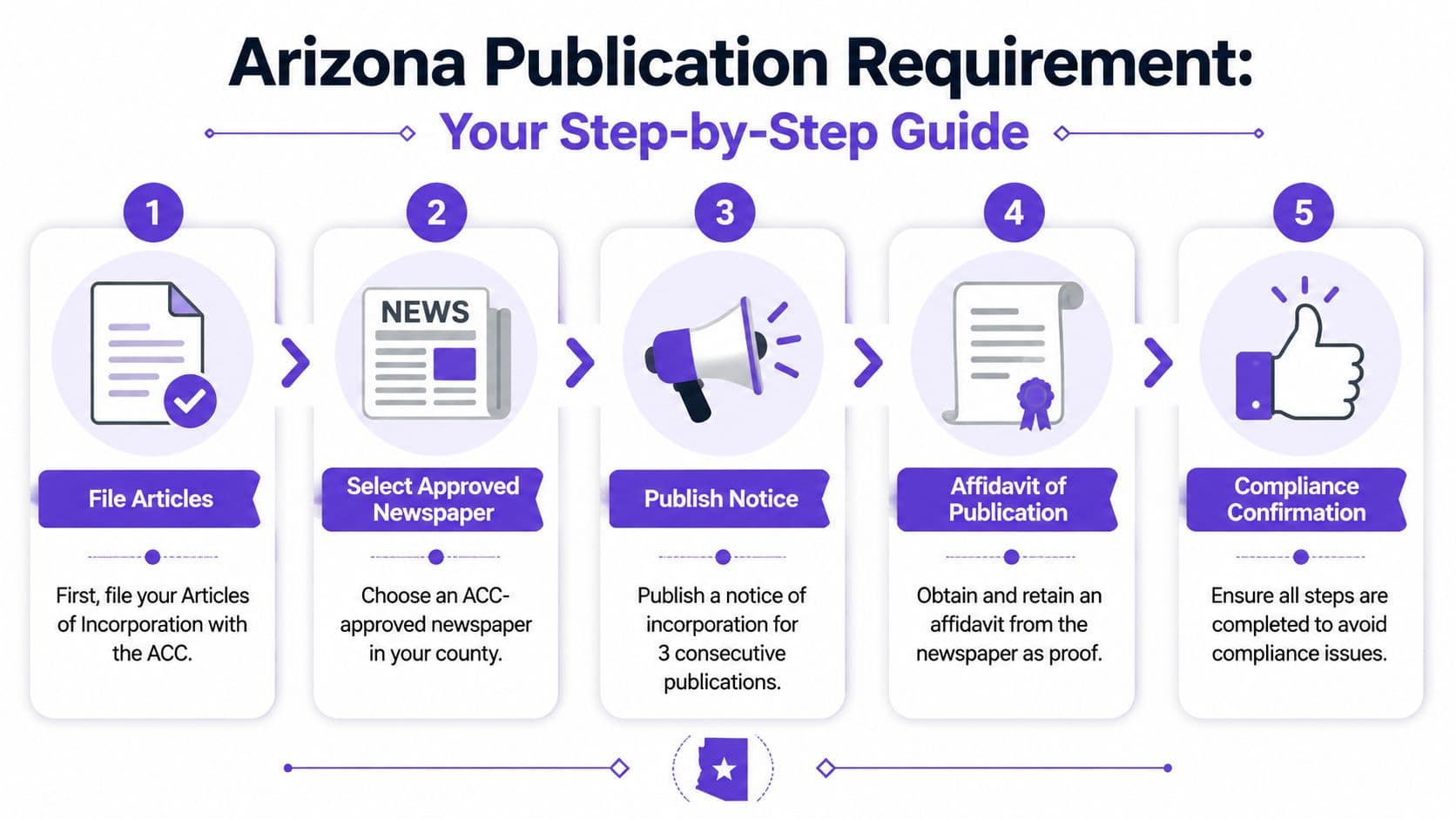

After the Arizona Corporation Commission approves the Articles of Incorporation, many corporations must publish a notice of the filing and keep proof that it was completed. The Arizona Corporation Commission explains the publication process and timing on its corporation formation instructions page.

From a finance seat, the risk is straightforward. If publication is missed, delayed, or documented poorly, the company creates a gap in its formation file. That gap tends to surface during lender diligence, investor legal review, insurance underwriting, or an audit request for organizational documents. At that point, the issue is no longer administrative. It becomes a timing problem, a cleanup cost, and a credibility problem.

The recordkeeping point matters just as much as the publication itself. Keep the affidavit or other proof from the newspaper in the permanent corporate records folder, indexed with the filed articles, Certificate of Disclosure, incorporator action, and stock records. If your team is already building the first-year tax file, store it with the materials used for your Form 1120 corporate tax filing process so legal formation and tax reporting support the same audit trail.

A practical publication workflow

Assign one owner and one reviewer. The owner gets the notice placed and collects proof. The reviewer confirms the notice ran in the correct publication, for the required period, and that the proof is saved where finance, legal, and outside auditors can find it.

Use this workflow:

- Confirm the filing was accepted. Publication starts after the articles are approved.

- Verify whether your corporation qualifies for an exception. Some corporations with a known place of business in Maricopa or Pima County are not subject to the newspaper publication requirement because the Commission posts notice instead.

- If publication is required, use an approved newspaper in the right county. Do not assume any local paper works.

- Place the notice immediately and confirm the run dates in writing. Waiting creates deadline risk with no upside.

- Collect the affidavit of publication as soon as the notice finishes running. Ask for a scanned copy and keep the original if provided.

- Save proof in the permanent records file and your compliance calendar. The date, newspaper, county, and storage location should be easy to verify later.

Three mistakes create avoidable cleanup work.

- No one owns the task. The filing gets approved, then publication sits in an inbox until someone asks for proof.

- The company keeps only the newspaper invoice. Payment shows the order was placed. It does not prove the notice ran correctly.

- The affidavit is saved locally instead of in the company records system. That turns a simple diligence request into a document hunt.

I usually tie publication to the same launch controls as payroll registration, sales tax review, bank authority, and stock issuance approvals. That is the right level of importance. In Arizona, publication affects whether the corporation can produce a clean formation record under pressure.

How to File Your Articles and What It Costs

The filing decision is mostly about speed, documentation control, and whether you're trying to hit a financing or contract deadline. Arizona's base filing cost is simple. The total launch cost is not.

The direct cash outlay

The statutory filing fee for for-profit Articles of Incorporation is $60, and the total average cost to form, including the filing fee, a $35 expedite fee, and mandatory newspaper publication costs (typically $65 to $125), is approximately $310, excluding legal or service fees, according to Paralegal Plus on Arizona incorporation costs.

Here's a worked calculation using the figures above:

| Cost item | Amount |

|---|---|

| Filing fee | $60 |

| Expedite fee | $35 |

| Newspaper publication at low end of typical range | $65 |

| Subtotal | $160 |

At the higher end of the stated publication range:

| Cost item | Amount |

|---|---|

| Filing fee | $60 |

| Expedite fee | $35 |

| Newspaper publication at high end of typical range | $125 |

| Subtotal | $220 |

The cited average total is approximately $310, which tells you to budget beyond just the filing receipt. In practice, founders often ignore related setup costs, then lump them into “miscellaneous legal.” That's not useful if you want a clean first-month close.

If your finance team is already building the post-formation tax calendar, connect the incorporation timeline to your federal filing workflow and accounting package setup. A simple way to keep that aligned is with a working reference for Form 1120 corporate tax obligations.

Arizona Incorporation Filing Options 2026

| Method | Base Fee | Expedite Options | Standard Processing Time | Expedited Processing Time |

|---|---|---|---|---|

| File with ACC | $60 | $35 expedite | Standard processing available | Expedited processing available |

The trade-off is straightforward:

- If timing matters: Pay the expedite fee and control the sequence tightly.

- If timing doesn't matter: Standard filing saves cash, but only if your packet is complete the first time.

- If you're signing contracts soon: Don't optimize for the smallest fee. Optimize for certainty and records quality.

A rejected filing costs more than the expedite fee once executive time, launch delay, and cleanup are included.

Common Filing Mistakes That Cause Rejection

Rejections usually come from basic control failures, not hard legal judgment. For a scaling SaaS or services business, that matters because a bounced filing delays more than formation. It can push back contract execution, bank setup, payroll registration, insurance binding, and the first clean close.

The rejection pattern I see most often

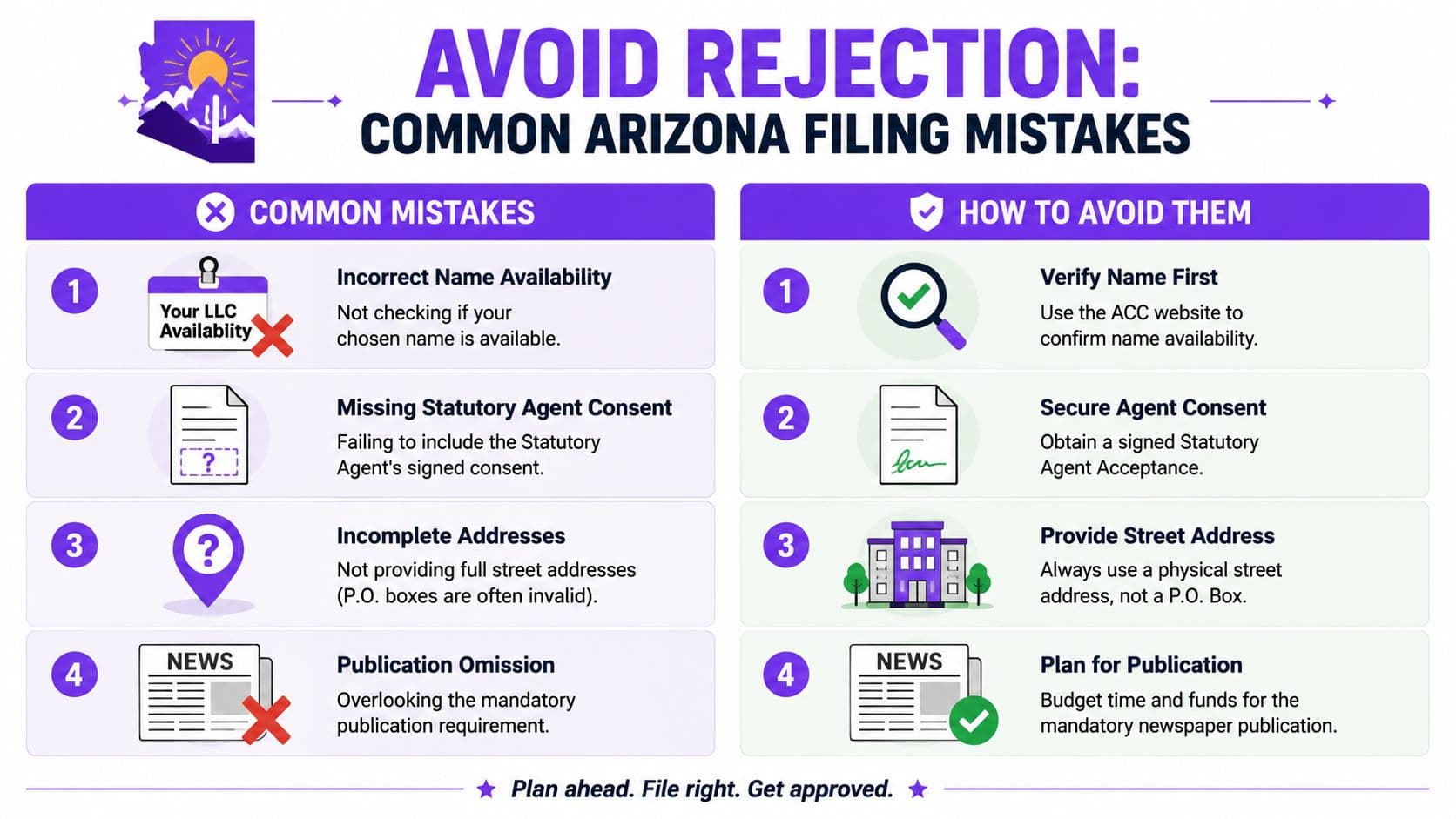

As noted earlier, missing the statutory agent acceptance form is the single biggest reason Arizona filings come back. Naming the agent in the articles does not complete the requirement. Arizona wants the acceptance included in the filing package, and if it is missing, processing stops until you fix it.

The next category is inconsistency. A business description that is too generic, a street address that does not match across documents, or a Certificate of Disclosure that conflicts with the articles can all trigger questions or rejection. These look like clerical mistakes, but they create a larger problem for finance and diligence. If your formation record is inconsistent on day one, investors, lenders, and auditors have a reason to question whether your cap table, board approvals, and tax registrations are being maintained with the same discipline.

I advise founders to review the filing set the same way they would review a lender package. One version of the company name. One source of truth for addresses, directors, and incorporator details. One final reviewer with authority to stop submission. That review standard is the same one buyers and investors expect in due diligence reports for transactions and compliance.

Red flags before you submit

Run this check before you file:

- Missing M002: Do not submit until the statutory agent has signed acceptance.

- P.O. box for the agent: Use the required physical address.

- Generic character of business language: Describe what the company does.

- Name mismatch: Match punctuation, suffixes, and capitalization across every document.

- Disclosure mismatch: Make sure the Certificate of Disclosure aligns with the articles and signer information.

- Wrong entity type for licensed work: Professional services may need a professional corporation structure rather than a standard corporation.

The Certificate of Disclosure deserves extra attention. Arizona asks for it for a reason. The state is screening for prior bankruptcies, convictions, license actions, and other items that affect public trust. If that form is incomplete or inconsistent, the issue is not just filing delay. It raises governance questions that can resurface later during underwriting, banking reviews, or an equity raise.

I see this most often in founder-led service firms that are trying to move fast. Legal drafts one version, operations updates an address, finance opens vendor accounts under another version of the name, and nobody does a final tie-out. Then the filing is rejected, or worse, accepted with a record set that does not match the books. Cleaning that up later costs more than doing the review properly up front.

The practical fix is simple. Assign one owner to compare the articles, M002, Certificate of Disclosure, and internal setup checklist line by line before submission. At the same time, line up your EIN application, bank resolution, and right-sized commercial insurance for Arizona companies so the entity record, risk coverage, and finance systems start from the same facts.

Post-Filing Compliance for Audit-Ready Businesses

Once the state accepts the filing, your corporation exists. That doesn't mean your company is ready for an audit, a lender package, or a seed round. Those outcomes depend on what you do in the first few weeks after formation.

Your first corporate records package

Start with the basic corporate record set. Obtain your EIN, adopt bylaws, document the initial board action, issue founder stock correctly, and store everything in one permanent file. If you use tools like QuickBooks, Xero, Stripe, Gusto, or NetSuite, align the legal entity start date with the accounting start date so your books don't drift from your governance record.

This is also the point to build a chart of accounts that reflects how you operate. SaaS businesses should separate recurring subscription revenue from implementation or services revenue. Agencies should distinguish project revenue, retainers, pass-through media spend, and contractor costs. Professional services firms should decide early how they'll track labor utilization, owner distributions, and reimbursable expenses.

"Founders who set up their chart of accounts to track SaaS metrics like MRR and CAC from the moment of incorporation save an average of 40 hours and $15,000 in accounting cleanup fees before their first seed round or audit. Getting it right at the start is the highest-leverage financial decision you can make." – Sarah Chen, CPA, Head of Client Strategy at Jumpstart Partners

Even if you're not fundraising yet, set the system up as if you were. That means retained board approvals, dated stock issuances, signed founder documents, and consistent bookkeeping from month one. It also means putting risk transfer in place. If you're evaluating policies after formation, right-sized commercial insurance for Arizona companies is a useful starting point for matching coverage to your operating profile.

The annual compliance item you can't ignore

Arizona requires ongoing maintenance. After incorporation, Arizona requires you to file an annual report in your corporation's anniversary month, costing $45. This is a mandatory annual compliance cost required to avoid penalties and administrative dissolution, according to Wolters Kluwer's Arizona incorporation requirements.

That annual report should sit on the same compliance calendar as your tax deadlines, payroll filings, sales tax reviews, contract renewals, and insurance renewals. Don't leave it to memory. Put it in your close checklist, your legal calendar, and your board admin file.

For audit readiness, I'd lock in these next steps within your first operating cycle:

- Create the permanent file: Articles, approvals, disclosures, stock records, EIN letter, and publication proof.

- Set up accounting cleanly: Match the entity start date and opening balances to the legal timeline.

- Document authority: Record who can sign contracts, open accounts, and approve payments.

- Calendar annual obligations: Include the anniversary-month report and corporate record review.

- Run a light internal review: Make sure legal records and accounting records tell the same story.

If you want a practical framework for the finance side of that process, this audit preparation checklist for growing companies is a strong place to start.

If your Arizona corporation is formed but your books, governance records, or compliance calendar still feel improvised, Jumpstart Partners can help you turn that entity into an audit-ready operating company. Their team supports SaaS, agencies, and professional services businesses that need clean monthly closes, investor-ready financials, and a finance function that keeps pace with growth.