Financial Operations

Bookkeeping for Nonprofit Organizations: 2026 Expert Guide

Master bookkeeping for nonprofit organizations. This 2026 guide covers fund accounting, Form 990, internal controls, & outsourcing. Get clarity.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··23 min readOnce your nonprofit crosses $200,000 in gross receipts or $500,000 in total assets, you move into full Form 990 territory, and your bookkeeping has to support a much deeper level of disclosure and control, including the Statement of Functional Expenses, as noted in Aplos' guide to nonprofit financial statements. That threshold changes the conversation. Bookkeeping is no longer a clerical task. It becomes part of governance, compliance, fundraising credibility, and board oversight.

For growing organizations, bad books rarely stay contained in the finance office. They show up as delayed grant reports, board packets nobody trusts, confused program leaders, and donors asking reasonable questions you can't answer quickly. Good bookkeeping for nonprofit organizations does the opposite. It gives you a clean line from daily transactions to strategic decisions, so leadership can scale programs without losing control of the money that funds them.

Table of Contents

- Why Standard Bookkeeping Fails Your Nonprofit

- The Two Pillars of Nonprofit Bookkeeping

- How to Handle Donations Grants and In-Kind Gifts

- Financial Reports That Keep You Compliant

- Building a Bulletproof Month-End Close and Internal Controls

- Common Pitfalls and Choosing the Right Software

- Checklist for Transitioning to Professional Bookkeeping

Why Standard Bookkeeping Fails Your Nonprofit

A for-profit bookkeeping setup assumes money is largely interchangeable. Your nonprofit can't operate that way.

Nonprofit bookkeeping evolved from simple transaction tracking into fund accounting because nonprofits must separate money by donor intent and program purpose instead of treating all cash as one pool, according to NetSuite's nonprofit accounting overview. That shift is the real dividing line. If your accounting system can't prove where restricted money came from, what it was spent on, and what remains committed, your books are not doing their job.

The real risk is loss of trust

An Executive Director usually sees the consequences before the root cause. A grant reimbursement runs late. A board member asks why cash is tight despite a successful campaign. A donor wants confirmation that their gift supported a specific program, and finance has to piece the answer together from spreadsheets, email threads, and bank activity.

Those aren't isolated annoyances. They're symptoms of a bookkeeping structure that was never built for nonprofit accountability.

Practical rule: If you can't explain a fund balance quickly and with documentation, you don't control it well enough.

The mistake is assuming small-business habits are close enough. They aren't. Nonprofits need books that support donor restrictions, functional expense reporting, annual filings, audits, and board oversight. That means recording transactions is only the starting point. The work also includes reconciliations, financial statement preparation, and a reliable trail for compliance questions.

Growth makes weak books visible

At the early stage, weak bookkeeping can hide behind a founder's memory and a lean team. In the growth stage, it breaks.

Program leaders start spending from grants with incomplete coding. Development records pledges or campaign activity in one system while finance posts deposits in another. Board reporting gets delayed because nobody trusts the first draft. Budgeting gets harder because leadership can't separate operating cash from restricted balances. If you're building stronger financial discipline, this often connects directly with how you approach budgets for nonprofit organizations.

A new Executive Director should treat bookkeeping as mission infrastructure. Clean books don't just keep you out of trouble. They let you answer harder questions with confidence: Which programs are subsidizing others? Which grants create hidden admin pressure? How much unrestricted capacity do you really have?

That is what standard bookkeeping misses. It records activity. A nonprofit needs a system that proves stewardship.

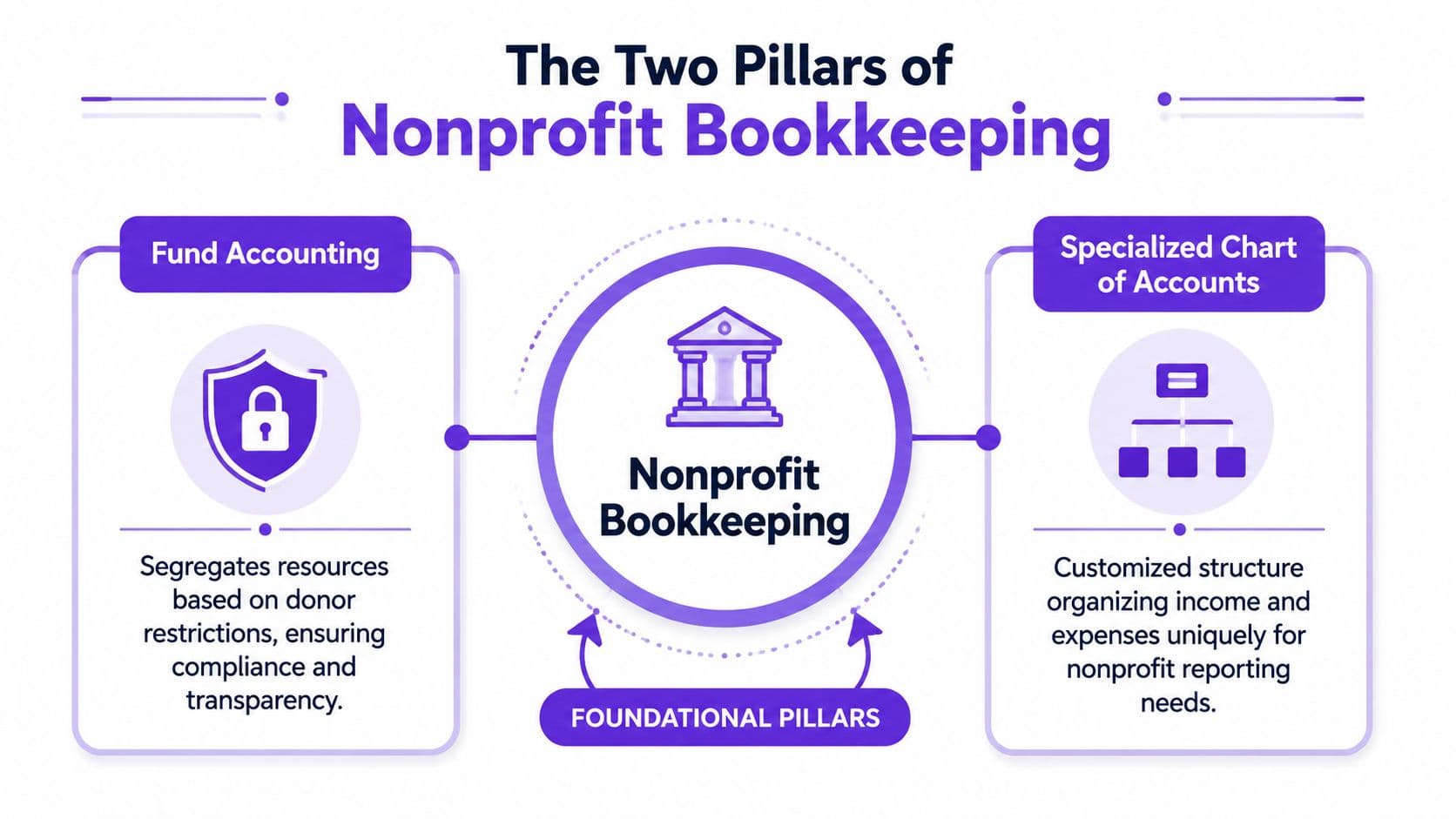

The Two Pillars of Nonprofit Bookkeeping

Fund accounting is the operating logic

Fund accounting works like a set of labeled buckets inside one financial system. Cash may sit in one bank account, but the ledger still has to show which dollars are available for operations, which are restricted to a program, which are limited by time, and which belong to a specific grant period. If that distinction breaks down, leadership starts making decisions with money it does not have permission to spend.

That is why fund accounting matters. It is not just an accounting format. It is the control system that protects donor intent, supports clean grant reporting, and keeps the board from approving plans based on overstated available cash. The Financial Accounting Standards Board explains nonprofit net asset classes and the presentation of donor restrictions in its guidance for not-for-profit entities, which is the accounting backbone behind this structure. For a more practical overview, see this guide to fund accounting for nonprofits.

The labels have changed over time in financial reporting, but the operating idea stays the same:

- Without donor restrictions for general use

- With donor restrictions for purpose or time limits

- Board-designated amounts for reserves or other internal commitments, which are not the same as donor restrictions

That last distinction matters more than many Executive Directors realize. A board-designated reserve can usually be redesignated by the board. A donor-restricted gift cannot. If the team treats those two categories as interchangeable during a cash squeeze, the cleanup is painful. It can affect grant reporting, year-end financial statements, and donor confidence.

A healthy finance function can answer two questions on the same day. How much cash is in the bank? How much of that cash is available to spend?

For leaders in faith-based or legacy institutions, there's useful guidance for Church Extension Fund leaders that reinforces the same operational principle. Pooled cash is common. Blurred accountability is not acceptable.

Your chart of accounts makes the system usable

If fund accounting is the logic, the chart of accounts is the structure that lets staff use that logic consistently. I have seen organizations with decent intentions and weak charts of accounts spend hours every month rebuilding reports in spreadsheets because the ledger was never set up to answer board and grant questions cleanly.

The two common failures are predictable. Some organizations build a chart that is too shallow, so program, grant, and functional expense reporting all get forced together. Others build one that is too detailed, so every new grant or event creates another account and the general ledger turns into a filing cabinet nobody can manage.

A workable setup usually supports several reporting needs at once:

| Need | What the chart should support | What goes wrong without it |

|---|---|---|

| Fund tracking | Separate donor-restricted and nonrestricted activity | Restricted spending gets mixed into operating results |

| Program reporting | Show revenue and expense by mission area | Leadership cannot see which programs are subsidizing others |

| Grant visibility | Track each award's budget and actual spending | Grant reports require manual cleanup and late adjustments |

| Functional expense reporting | Distinguish program, management, and fundraising costs | Form 990 prep and audit support become slower and less reliable |

The goal is disciplined simplicity. Keep natural accounts focused on what the transaction is, such as salaries, occupancy, supplies, or consulting. Use segments, classes, departments, locations, or projects to track who spent it, which fund it belongs to, and which program benefited. That gives leadership cleaner reporting without turning the chart into a maze.

Poor chart design is not just a bookkeeping nuisance. It slows closes, weakens board reporting, hides margin pressure inside programs, and makes growth harder to fund. Clean structure gives you something much more useful than tidy books. It gives the Executive Director and board a reliable picture of capacity, constraint, and risk.

How to Handle Donations Grants and In-Kind Gifts

The ledger needs to reflect not just that support came in, but what kind of support it was. That's where a lot of nonprofit teams drift into avoidable errors.

Best practices in nonprofit accounting from Lamar University note that donor restrictions must be tracked separately in the general ledger, with restricted, temporarily restricted, and unrestricted funds receiving distinct treatment so spending stays tied to the applicable purpose. That changes how you classify revenue on day one, not just how you report it later.

Three revenue types that need different treatment

A cash gift for operations, a program-restricted grant, and a donated service may all support your mission. They should not all hit the books the same way.

| Transaction Type | Example | Accounting Impact (Simplified) |

|---|---|---|

| Unrestricted donation | A donor gives cash for general operations with no stated restriction | Record contribution revenue without donor restriction and increase cash |

| Restricted grant | A foundation awards funding that must be used for a named program | Record contribution or grant revenue in the restricted fund category and track related spending against that purpose |

| In-kind gift | A professional donates specialized services or a business donates goods | Record the non-cash contribution with supporting documentation and reflect the related expense or asset based on what was received |

A simple mental test helps. Ask two questions before posting revenue: What did we receive, and what conditions govern its use? If finance can't answer both clearly, the entry isn't ready.

If your team needs a deeper framework for coding and reporting restricted activity, this guide to fund accounting for nonprofits is a useful companion.

What teams get wrong with in-kind support

In-kind support creates more confusion than standard cash donations because the accounting issue isn't just classification. It's also documentation and valuation.

Araize's overview of bookkeeping for nonprofits points out that modern revenue streams such as in-kind donations, volunteer labor, and mixed-purpose online giving are still underexplained in most mainstream guidance, especially around valuation, documentation, and when they materially affect reporting. That's exactly where many nonprofits get stuck. They know the contribution matters operationally, but they don't have a repeatable process for recording it correctly.

What works in practice:

- Document the source clearly so you know who donated the good or service and when.

- Capture the restriction, if any because some in-kind support is designated for a specific program.

- Keep support for valuation such as invoices, rate sheets, comparable pricing, or a written description of the donated item or service.

- Coordinate with development so donor acknowledgments and accounting records tell the same story.

What doesn't work is posting a rough estimate at year-end with no backup, or ignoring non-cash gifts until the audit prep list forces the issue. That creates stress for finance and confusion for donors.

The hardest nonprofit revenue to book isn't always the biggest gift. It's the gift nobody documented well when it arrived.

Financial Reports That Keep You Compliant

IRS filing requirements and audited financial statements expose weak bookkeeping fast. By the time a finance committee sees a bad report, the underlying problem usually started months earlier with miscoded expenses, unreconciled balances, or a chart of accounts that cannot support the questions leadership needs answered.

For nonprofits in the $500K to $20M range, these reports do more than satisfy accountants. They shape board decisions, affect donor confidence, and determine whether management can spot cash pressure before it becomes a staffing or program problem.

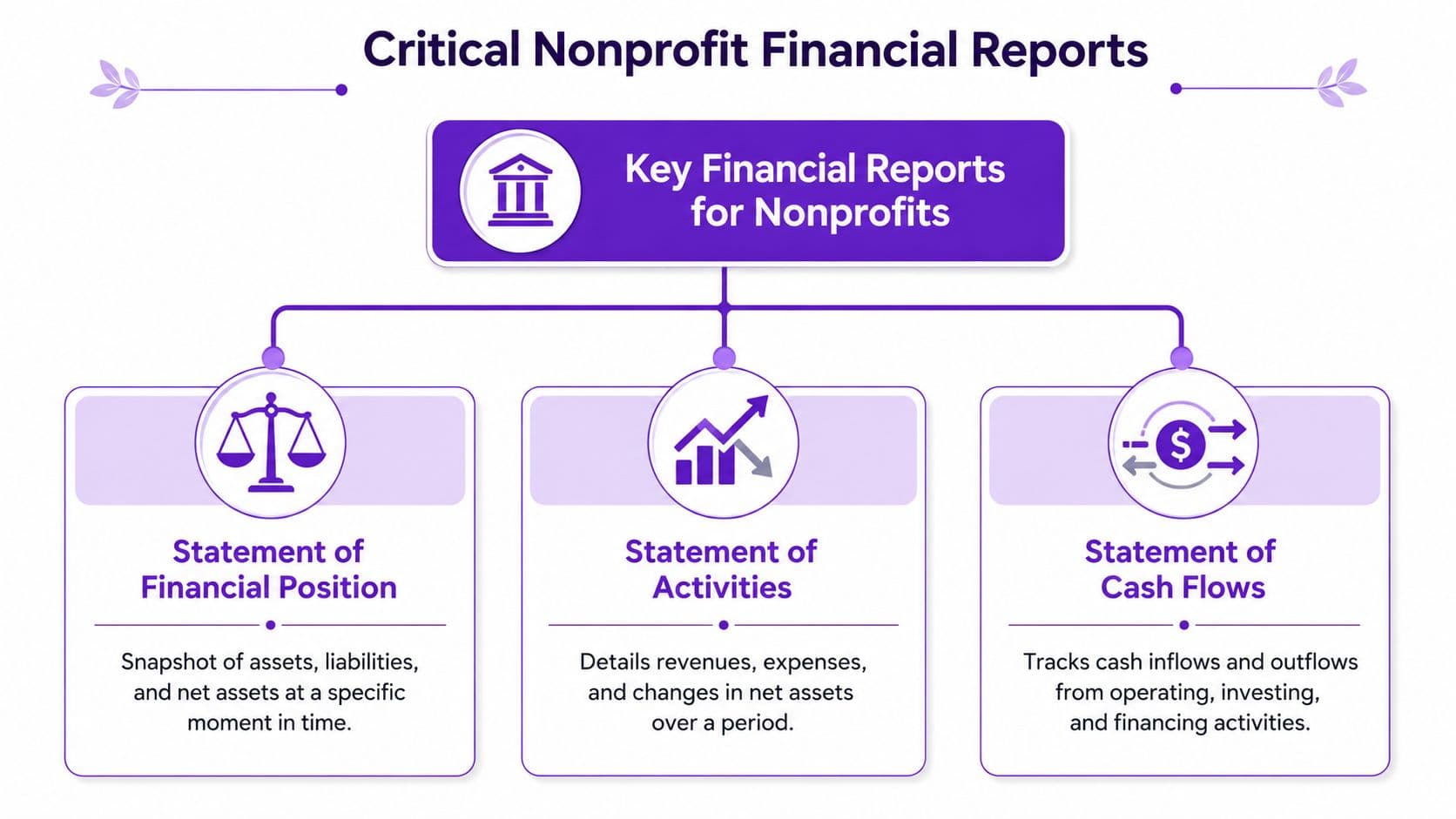

The reports your board and regulators actually need

A complete reporting package usually includes four statements. The National Council of Nonprofits outlines the core set nonprofits are expected to understand and use: statement of financial position, statement of activities, statement of cash flows, and statement of functional expenses, as explained in its guide to nonprofit financial statements.

| Report | What it tells you | Why leadership should care |

|---|---|---|

| Statement of Financial Position | Assets, liabilities, and net assets at a point in time | Shows liquidity, debt load, and whether reserves are actually available |

| Statement of Activities | Revenue, expenses, and changes in net assets over a period | Shows whether operations are covering costs and whether restricted funding is masking an operating gap |

| Statement of Cash Flows | Cash moving through operating, investing, and financing activity | Shows whether reported surplus is turning into cash you can use for payroll and programs |

| Statement of Functional Expenses | Expenses broken into program, management, and fundraising categories | Supports transparency, Form 990 preparation, grant reporting, and board oversight |

Fund accounting works like a set of labeled buckets, but your financial statements are where those buckets have to reconcile into one credible story. If the buckets are mislabeled or mixed together, the board gets a distorted view of program margins, available cash, and overhead. That is how an organization can appear stable on paper while struggling to fund basic operations.

For a practical walkthrough of account structure that supports these reports, a nonprofit chart of accounts template can help finance leaders pressure-test whether their current setup is report-ready.

This short video is also a useful primer for teams that need a visual explanation of nonprofit financial statements.

Why the statement of functional expenses matters so much

The Statement of Functional Expenses is often the first report to expose a bookkeeping system that looked acceptable on the surface. If payroll allocations, vendor coding, and shared cost treatment were inconsistent all year, this statement becomes a year-end cleanup project. That is expensive, slow, and risky.

It also matters for external filing. The IRS instructions for Form 990 explain that larger organizations generally file the full return instead of the shorter 990-EZ, based on gross receipts and total assets thresholds, and those filings require far more detailed financial disclosure, as shown in the IRS Instructions for Form 990 and 990-EZ.

In practice, functional expense reporting affects three board-level decisions:

- Program strategy. Leaders can see whether a mission area is financially sustainable or subsidized by unrestricted support.

- Fundraising investment. Development costs are visible enough to judge return, staffing levels, and campaign performance.

- Infrastructure planning. Management and general expenses stop disappearing into overhead myths and can be discussed as real capacity costs.

I tell new Executive Directors to read the Statement of Activities and the Statement of Functional Expenses together. One shows whether the organization lived within its means. The other shows how it chose to spend those means. If those reports do not line up with the strategy approved by the board, the bookkeeping is not doing its job.

Building a Bulletproof Month-End Close and Internal Controls

A late close does more than delay reports. It slows decisions, hides cash pressure, and leaves the board steering with old information. In a growing nonprofit, that creates real risk. Grant spending can drift off budget, restricted balances can be overstated, and donor confidence can erode before leadership sees the problem.

A workable month-end close rhythm

Month-end close works like an air traffic control system. Each handoff has to happen in order, and everyone needs to know who is responsible for the next step. If development enters gifts late, or program staff sit on expense details, finance closes the month on guesses. Guesses turn into corrections, and corrections turn into board packets no one fully trusts.

The goal is not speed by itself. The goal is a close that is fast enough to support management and accurate enough to support compliance.

A practical sequence looks like this:

- Reconcile bank and credit card accounts so cash activity is complete and unusual items are identified early.

- Post payroll and benefits with allocations reviewed before they hit the financials, especially if salaries are split across programs, fundraising, and administration.

- Record payables and accruals so the month accurately reflects what the organization incurred, not just what cleared the bank.

- Tie donation and grant records to the general ledger so deposits, pledges, and releases are consistent across systems.

- Review restricted balances and confirm spending was charged to the right funding source.

- Investigate budget variances with department owners while the details are still fresh.

- Issue draft financials and a short close memo that explains unusual swings, liquidity concerns, and any items still under review.

Teams that need more discipline usually benefit from a documented month-end close checklist template. A checklist does not replace judgment. It reduces skipped steps, unclear ownership, and the end-of-month scramble that burns out staff.

Cross-functional coordination is often the primary failure point. Revenue may start in a donor database, pass through development, and only later reach accounting with the detail finance needs to classify it correctly. The National Council of Nonprofits addresses this broader coordination problem in its guidance on internal controls for nonprofits. The close should be treated as an organization-wide operating process, not an accounting task that finance is expected to rescue at the end.

Red flags that signal control problems

Internal controls protect the organization on ordinary days and bad days. They reduce the chance of error, make fraud harder to hide, and give the Executive Director and board a basis for trusting the numbers.

YPTC's nonprofit accounting guidance recommends segregation of duties so the person recording transactions is different from the person approving them, along with clear policies for expense approval, cash handling, payroll, and reporting. That separation matters because nonprofits often run on trust, and trust without verification fails under pressure.

Watch for these warning signs:

- One employee controls the full cash cycle from opening mail to making deposits to reconciling the account.

- Approvals happen informally in chat threads, hallway conversations, or undocumented emails.

- Payroll changes are processed without secondary review for pay rates, hours, or new hires.

- Development and accounting reports do not reconcile by donor total, campaign, or deposit date.

- User access is too broad and former staff still have active logins.

- Restricted funds are reviewed only at year-end after spending decisions have already been made.

Small nonprofits can still separate duties. One person can approve, another can enter, and a third can review the bank reconciliation or payroll register. If staffing is thin, use board treasurers, outsourced accounting support, or system-based approval workflows. The point is simple. No single person should control approval, custody, recording, and review for the same transaction stream.

Common Pitfalls and Choosing the Right Software

Bad software choices rarely fail on day one. They fail six months later, when the finance manager cannot explain grant balances, development is reporting a different donation total than accounting, and the board packet takes two days of spreadsheet cleanup to finish.

That is the full cost of weak bookkeeping systems in a growing nonprofit. Poor setup does not just create clerical mess. It slows decisions, obscures restricted cash, and raises the odds of reporting errors that can damage donor confidence and create compliance problems.

Why generic small-business setups break down

A standard small-business file can work for a very small nonprofit with simple activity. Once the organization has multiple grants, donor restrictions, program departments, and board reporting needs, the shortcuts start to show.

The problem is structural. Small-business bookkeeping is usually organized around profitability and basic cash flow. Nonprofit bookkeeping is organized around accountability. Finance needs to show not only what came in and what went out, but also whose money it is, what it can be used for, and whether it was spent in line with restrictions. Fund accounting works a lot like keeping separate labeled envelopes inside one bank account. The cash may sit in one place, but each dollar still has rules attached to it.

Month-end close is often where weak systems get exposed. If revenue data lives partly in the CRM, partly in a donor platform, and partly in the general ledger, staff end up exporting files, fixing coding by hand, and posting entries after the fact. That creates delay, but the larger risk is false confidence. Reports can look polished while the underlying classifications are wrong.

The most common failures are predictable:

| Pitfall | What it looks like in practice | Consequence |

|---|---|---|

| Misclassifying restricted revenue | Grant income posted as general operating support | Leadership overstates spendable cash |

| Releasing restrictions too early | Program expenses coded to the wrong grant or period | Donor reports and financial statements conflict |

| Overgrown chart of accounts | New accounts created for every event, campaign, or gift type | Close process slows and trend reporting becomes unreliable |

| CRM and GL mismatch | Donation platform totals do not tie to deposits and ledger entries | Finance and development lose trust in each other's numbers |

| Small-business software used without nonprofit configuration | No fund, grant, or functional tracking built into the setup | Heavy manual work, audit friction, and higher error risk |

I see one trade-off come up often. Leaders choose the cheapest platform because the budget is tight, then absorb the difference in staff time. That usually works until reporting complexity increases. At that point, the organization is paying for the cheaper system with delayed closes, rework, and missed management insight.

What to look for in nonprofit accounting software

Choose software based on reporting discipline, not popularity.

A sound system should let the team track restrictions, grants, programs, and functional expenses without building every report from scratch in Excel. It should also support the way nonprofit decisions get made. The Executive Director needs timely budget-to-actuals. Program leaders need spending visibility before they overrun a grant. The board needs financials that are clear enough to govern from, not just receive.

Look for these capabilities:

- Fund accounting support so restricted and unrestricted activity stays separate

- Grant and contract tracking by award, budget period, and spending category

- Dimensional reporting through classes, locations, departments, or tags

- Custom financial statements that match board, audit, and funder needs

- Integration with donor systems, payroll, and bill pay to reduce manual reconciliation

- User permissions and audit trails so approvals, edits, and access are easier to control

- Import and export flexibility for clean data transfers during audits, grant reporting, and system changes

If you are weighing options, this guide to the best accounting software for nonprofits is a practical starting point.

Software alone will not fix broken processes, though. A powerful platform in careless hands just produces faster confusion. If your team lacks capacity to maintain clean books, structured close procedures, and accurate coding, outside support may be the better near-term decision. Some organizations reach that point before they need a new platform. If you need extra accounting capacity, Hire Bookkeepers can be one way to fill the gap while leadership decides whether to upgrade systems, staffing, or both.

The right setup should make good decisions easier. That is the standard. If the books depend on one staff member's memory, a maze of spreadsheets, or month-end cleanup nobody else understands, the system is already too weak for the organization you are trying to build.

Checklist for Transitioning to Professional Bookkeeping

There comes a point when the issue isn't effort. It's capacity.

A founder, Executive Director, or operations lead can hold the books together for a period of time. But once the organization is juggling multiple grants, board reporting deadlines, donor restrictions, payroll allocations, and month-end reconciliations, professional bookkeeping becomes a management decision, not a luxury.

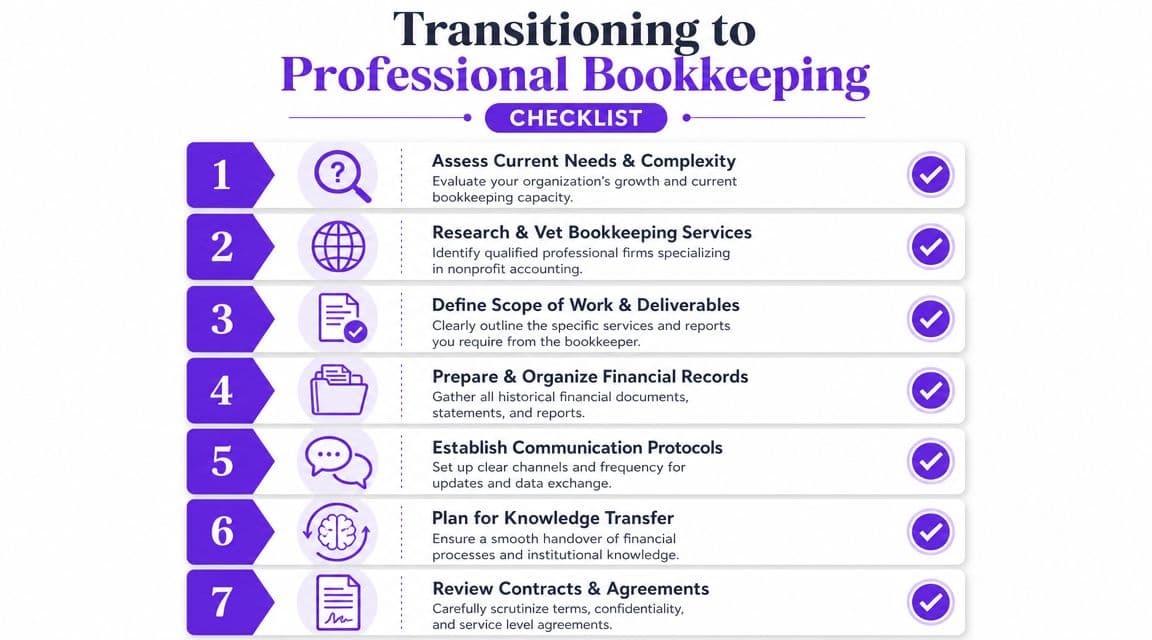

What to prepare before you hand off the books

A clean transition starts with organization. If you prepare the right records up front, the new bookkeeping partner can diagnose problems faster and avoid carrying old confusion into the new process.

Gather these first:

- Formation and compliance documents such as bylaws, tax-exempt determination letters, and prior filings.

- Access to financial systems including accounting software, banks, payroll, bill pay, and donation platforms.

- Current chart of accounts and reporting packages so the new team can see how you classify activity today.

- Grant agreements and donor restriction documentation since fund tracking begins here.

- Prior reconciliations and open balance questions so unresolved issues are visible instead of buried.

If you're exploring providers, a marketplace like Hire Bookkeepers can help you see the range of bookkeeping support available and compare fit before you commit.

How to make the transition smooth

The handoff itself should be structured. Don't treat it like a software migration and don't treat it like a one-time cleanup. Treat it like an operating change.

A strong transition plan usually includes:

- Define scope clearly. Monthly bookkeeping, close support, grant tracking, board reporting, and cleanup work should be spelled out.

- Set a reporting calendar. Decide when draft financials, final reports, and leadership reviews should happen each month.

- Assign internal owners. One person should own development data, another approvals, another banking access.

- Document policies. Expense approvals, restricted-fund reviews, and coding rules should not live in someone's head.

- Plan knowledge transfer. Explain historical quirks, recurring grants, seasonal campaigns, and board expectations early.

- Review the first reporting cycle closely. The first clean close often reveals old balance issues, coding inconsistencies, or missing documentation.

A mature nonprofit doesn't outsource bookkeeping to avoid responsibility. It does it to improve visibility, control, and consistency.

If your team is spending too much time untangling fund balances, fixing reports late, or rebuilding donor detail by hand, it may be time to replace improvised finance work with a real system.

If your nonprofit needs cleaner books, stronger month-end discipline, and reporting that your board and donors can trust, Jumpstart Partners can help you build a more reliable finance function. A consultation is the fastest way to assess where your bookkeeping process is breaking down, what needs cleanup first, and how to put compliant, decision-ready reporting in place.