Financial Operations

How to Calculate Total Revenue: A Founder's Guide

Learn to calculate total revenue for SaaS, agency, and e-commerce models. Our guide covers formulas, ASC 606 compliance, and pitfalls investors look for.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··14 min readMost founders think revenue is obvious. It isn't. If you're running a business between $500K and $20M, the number at the top of your P&L is often a blend of cash received, invoices sent, subscription activity, and platform exports that don't agree.

That's a problem because revenue is the first number investors, lenders, and buyers test. If it's wrong, everything built on top of it is wrong. Your forecast is wrong. Your margin analysis is wrong. Your sales compensation plan is wrong. Your due diligence process gets slower and more painful.

The biggest mistake I see is simple: founders learn price × quantity, then assume that formula is enough for a hybrid business. It isn't. You need the basic formula, then you need a disciplined method for subscriptions, discounts, returns, and revenue recognition under ASC 606.

Beyond Price x Quantity: Foundational Revenue Calculations

The starting point to calculate total revenue is still the universal formula:

Total Revenue = Price per Unit × Number of Units Sold

That baseline applies across business models, and it's still the cleanest way to begin. Patriot Software's overview of total revenue gives the standard example: 1,000 units at $50 each = $50,000 in total revenue.

If you don't have this formula nailed down, stop trying to build dashboards. Fix the foundation first. Your chart of accounts, invoice logic, and sales tracking all depend on this number being clean.

The basic product example

For a straightforward product business, the calculation is mechanical.

| Business type | Units sold | Price per unit | Total revenue |

|---|---|---|---|

| Product company | 1,000 | $50 | $50,000 |

| Hardware seller | 500 Xbox units | $249 | $124,500 |

That second example matters because it shows the formula doesn't care whether you sell low-ticket goods or higher-priced items. The math is identical. Your controls are what change.

How service businesses apply the same logic

Service founders often overcomplicate this part. The same principle still applies. You identify the unit, then multiply by price.

Your “unit” may be:

- A project

- A retainer period

- A billable package

- An average customer subscription amount

For businesses with multiple revenue streams, the calculation can require multiplying customer count by average service price, as noted in the same Patriot Software explanation of total revenue. That's where many firms start drifting away from precision.

Practical rule: If you can't define the unit you're selling, you can't calculate revenue reliably.

A professional services firm billing fixed-fee projects should treat each completed project or earned billing period as the unit. A subscription business should treat active customers multiplied by the relevant service price as the baseline. A hybrid model needs both.

Where founders go wrong early

Here's the common failure pattern:

- You use bank deposits as revenue. That's cash flow, not revenue.

- You use invoices as revenue. That's closer, but still incomplete if timing or fulfillment is off.

- You ignore pricing changes. Mid-period discounts and promo pricing need to be reflected in the actual revenue calculation.

- You mix channels together with no supporting schedule. That creates a top-line number no one can verify.

Your first job isn't sophistication. It's consistency. Build a revenue schedule that ties every dollar to a defined unit, a defined price, and a defined period. Then layer in the harder stuff.

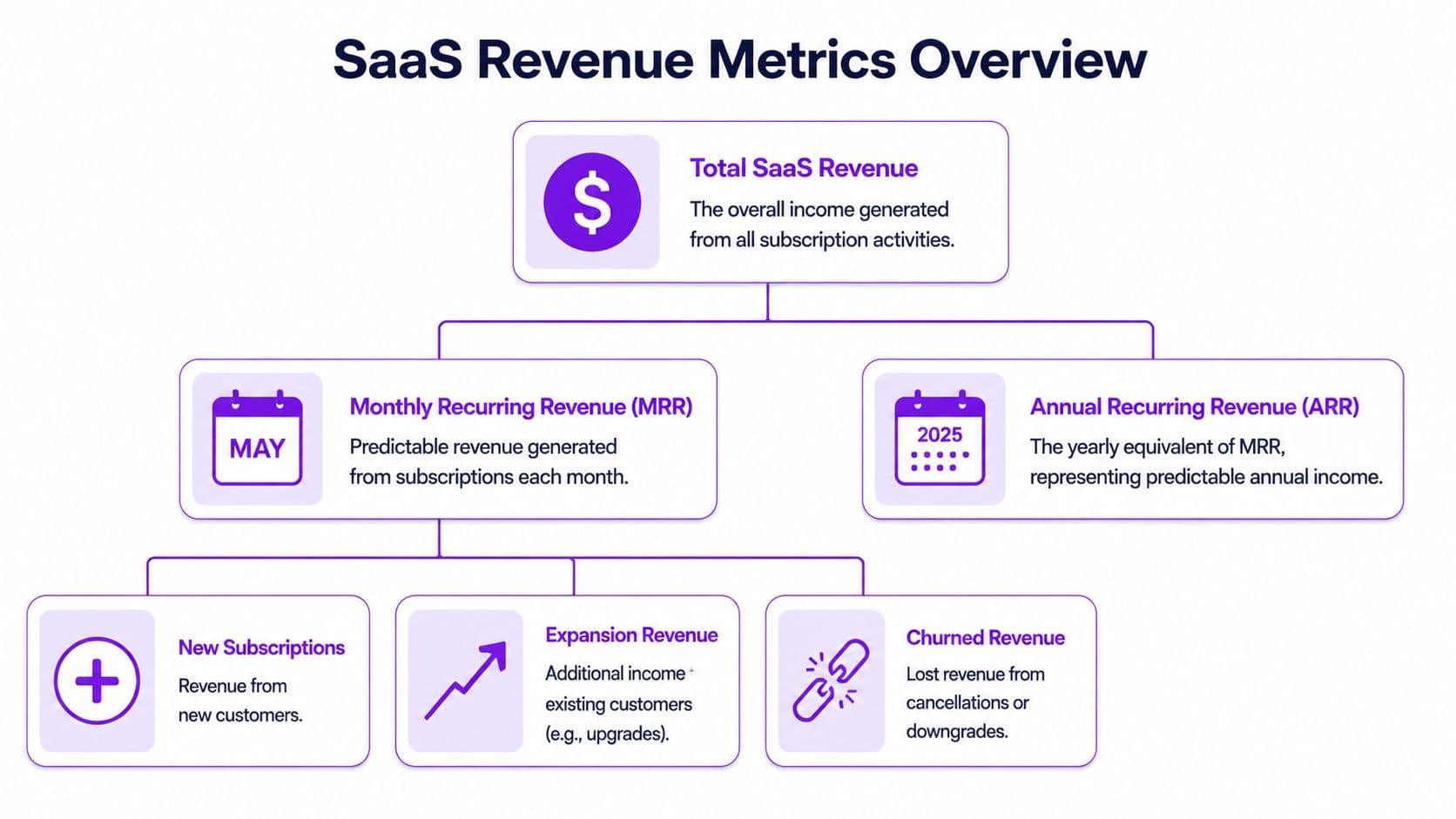

Calculating Revenue for SaaS and Subscription Models

SaaS founders love headline MRR because it's easy to quote. That's fine for a board update. It's not enough if you're trying to calculate total revenue accurately.

For modern SaaS businesses, the formula expands beyond subscriptions. HiBob's breakdown of total revenue states it clearly: Total Revenue = Monthly Recurring Revenue (MRR) + Non-Recurring Revenue + Usage-Based Revenue + Professional Services Revenue + Other Revenue. Their worked example shows $25,000 MRR + $5,000 non-recurring + $1,000 usage-based + $2,000 professional services = $33,000 monthly, excluding other revenue.

If you report only MRR, you're reporting only part of the business.

What belongs in total SaaS revenue

Use this framework:

| Revenue component | What it includes | Should it count in total revenue |

|---|---|---|

| MRR | Ongoing subscription fees | Yes |

| Non-recurring revenue | Setup fees, onboarding, one-time packages | Yes |

| Usage-based revenue | Overage charges, consumption fees | Yes |

| Professional services revenue | Implementation, migration, consulting | Yes |

| Other revenue | Additional operating revenue streams | Yes |

That's the operational reality of a growing SaaS company. You may sell a recurring platform, but your books still need to capture every earned revenue stream separately.

A worked SaaS example

Say your company has:

- A core subscription base generating $25,000 in MRR

- One-time onboarding fees of $5,000

- Usage-based overages of $1,000

- Implementation work worth $2,000

Your monthly total revenue is:

$25,000 + $5,000 + $1,000 + $2,000 = $33,000

That's your total monthly revenue for the period, based on the HiBob framework above. If you also have another qualifying revenue stream, it belongs in the “other revenue” bucket and gets added too.

MRR is not your top line

Founders often make three bad assumptions:

- MRR equals total revenue. It doesn't if you bill anything outside the subscription.

- ARR solves the problem. It doesn't. ARR is useful for annualizing recurring revenue, but it doesn't replace actual period revenue calculation.

- Platform dashboards are good enough. Stripe, QuickBooks, Xero, and your CRM rarely line up cleanly without deliberate mapping.

If you need a clean refresher on recurring metrics, review how monthly recurring revenue works. Then separate your KPI dashboard from your accounting reality. They're related, but they're not the same thing.

If your board deck says one revenue number and your general ledger says another, the ledger wins.

What I recommend

For a subscription business, keep revenue in separate buckets at minimum:

- Recurring subscription revenue

- One-time fees

- Usage-based charges

- Services revenue

- Credits, refunds, and reductions

That structure gives you two things founders need. First, a trustworthy total revenue number. Second, visibility into what drives growth. Without segmentation, you can't tell whether growth came from customer expansion, extra service work, or a temporary spike in setup fees.

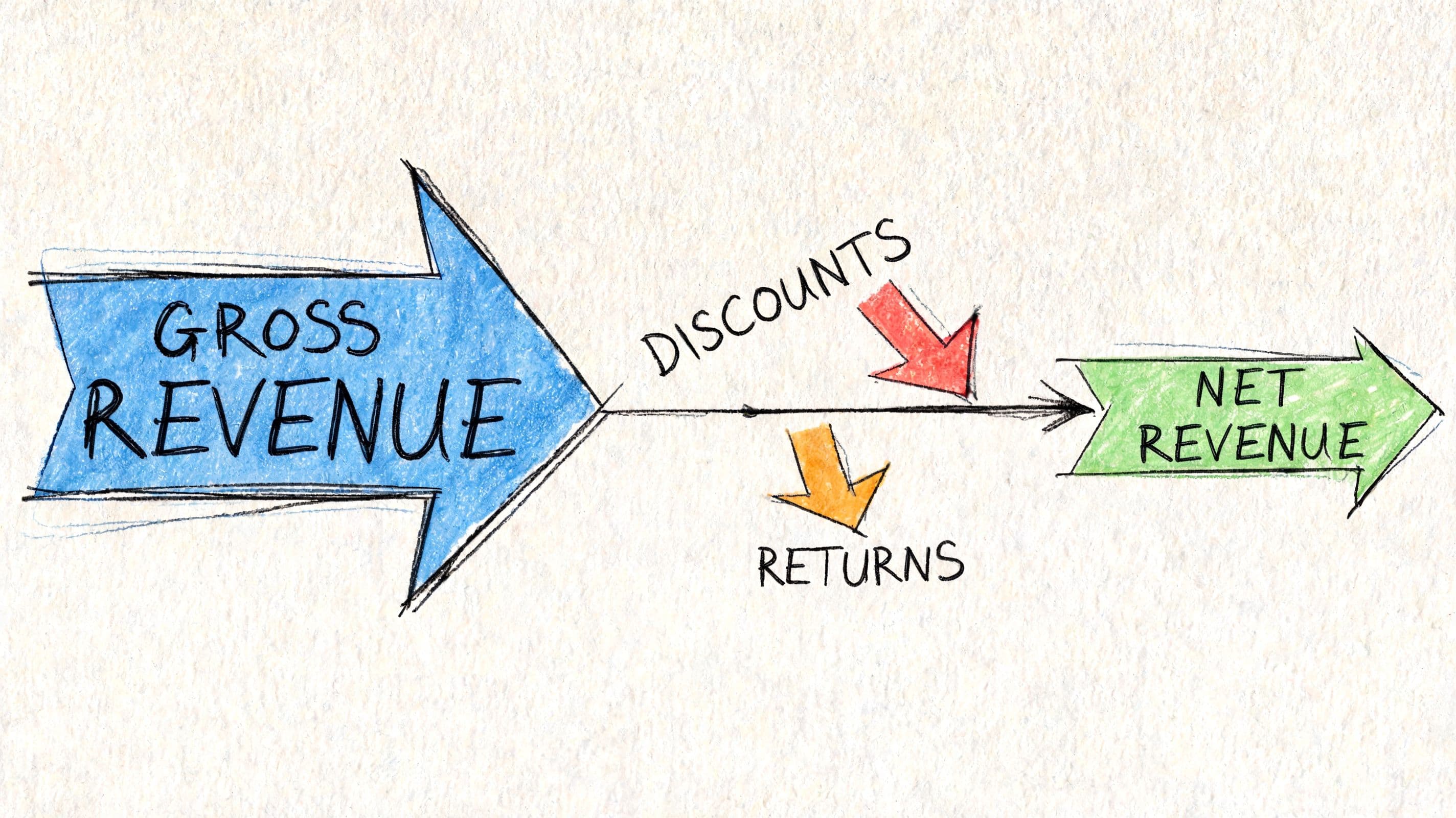

From Gross to Net: Adjusting for Discounts and Returns

Most founders stop at gross revenue. That's lazy accounting.

Gross revenue tells you what you sold before reductions. Net revenue tells you what you kept after discounts, returns, and allowances. If you skip this adjustment, you inflate performance and misread profitability.

The revenue waterfall you should use

Here's the clean way to understand it:

| Step | Revenue layer | What happens |

|---|---|---|

| 1 | Gross revenue | Start with total billed or earned sales before reductions |

| 2 | Less discounts | Remove promotional price reductions and sales discounts |

| 3 | Less returns | Remove refunded product or service value |

| 4 | Less allowances | Remove credits or concessions granted to customers |

| 5 | Net revenue | Arrive at the usable top-line number |

This is the number that should inform your margin analysis and your operating decisions.

Why discounts need discipline

If you run promos, custom pricing, or agency concessions, don't bury them in miscellaneous expense accounts. That hides erosion in your pricing strategy.

A founder who says, “we sold at full price but gave a concession later,” is describing contra-revenue. That reduction belongs against revenue, not buried lower on the P&L.

For e-commerce operators, pricing and margin discipline go hand in hand. If you want a practical operating view, this Shopify profit margin guide is a useful companion because it forces you to connect revenue quality to actual margin.

Operator check: If your sales team tracks bookings but finance doesn't track discounts and credits against those bookings, your top line is overstated.

You also need a returns and allowances schedule that ties to your accounting records. If your current setup is messy, review how returns and allowances should be handled.

Here's a short explainer illustrating the concept visually:

The misconception that causes bad decisions

Founders often say, “A refund is just part of doing business.” True. But that doesn't mean you can ignore it in reporting.

When you calculate total revenue for decision-making, gross revenue tells only the first half of the story. Net revenue is what makes your reporting useful. It affects compensation plans, channel analysis, and whether a product line is performing.

If your gross number rises while discounts and returns rise faster, your business is not improving. Your reporting should make that obvious.

The Revenue Recognition Minefield: Navigating ASC 606

Simple guides often prove inadequate. They teach arithmetic, not accounting.

Under ASC 606, accrual-basis accounting requires you to recognize revenue when it is earned, not when cash is received, as explained in Salesforce's revenue formula overview. That timing difference can create a 15–45 day variance in total revenue reporting depending on payment terms, and their example is direct: a $10,000 contract earned in Month 1 must be recognized in Month 1 even if payment arrives in Month 2.

That rule isn't optional if you want audit-ready financials.

Cash received is not revenue earned

Here's the trap. A client pays upfront, and you book the full amount as current-month revenue. That feels good because cash hit the bank. It's still wrong if the work hasn't been delivered.

Use a digital agency example. You sign a 3-month, $30,000 project. The client pays upfront.

Wrong approach:

- Recognize $30,000 in the month cash arrives

Right approach:

- Recognize $10,000 in each month as the work is delivered

That's what accrual accounting demands. Revenue follows performance obligations, not bank activity.

Why founders resist this

They usually give one of three reasons:

- “Cash is easier to track.” Sure. It's also the wrong basis for reporting earned revenue.

- “My bookkeeper can fix it later.” Later is when diligence starts, and then the cleanup becomes painful.

- “We're not big enough for ASC 606 discipline.” If you sign contracts with timing differences, bundles, retainers, or prepaid work, you're already in the problem set.

"Under ASC 606, accrual-basis accounting is required, mandating that businesses recognize revenue when earned, not when cash is received." Salesforce's total revenue formula article

That's the expert quote founders need to hear because it cuts through the debate. This is an accounting requirement, not a style preference.

What proper recognition looks like

You need to classify revenue by performance obligation:

| Revenue type | Recognition pattern | Founder mistake |

|---|---|---|

| Product delivery | At point of delivery | Booking on invoice date regardless of shipment or fulfillment |

| Subscription or retainer | Over time | Booking the full contract at signing |

| Milestone-based project work | As milestones are satisfied | Booking based on cash collection |

If your business has contracts, implementation work, annual prepayments, or bundled deliverables, you need rules for each category. Don't leave this to memory.

Non-negotiable controls

You need these in place:

- A written revenue recognition policy that matches how you sell

- Deferred revenue accounts for cash collected before work is earned

- Revenue schedules by contract for multi-period work

- Monthly review of fulfilled versus invoiced work

- System mapping across Stripe, QuickBooks, Xero, or NetSuite

If you don't have those controls, your monthly revenue number is a guess wearing a spreadsheet costume.

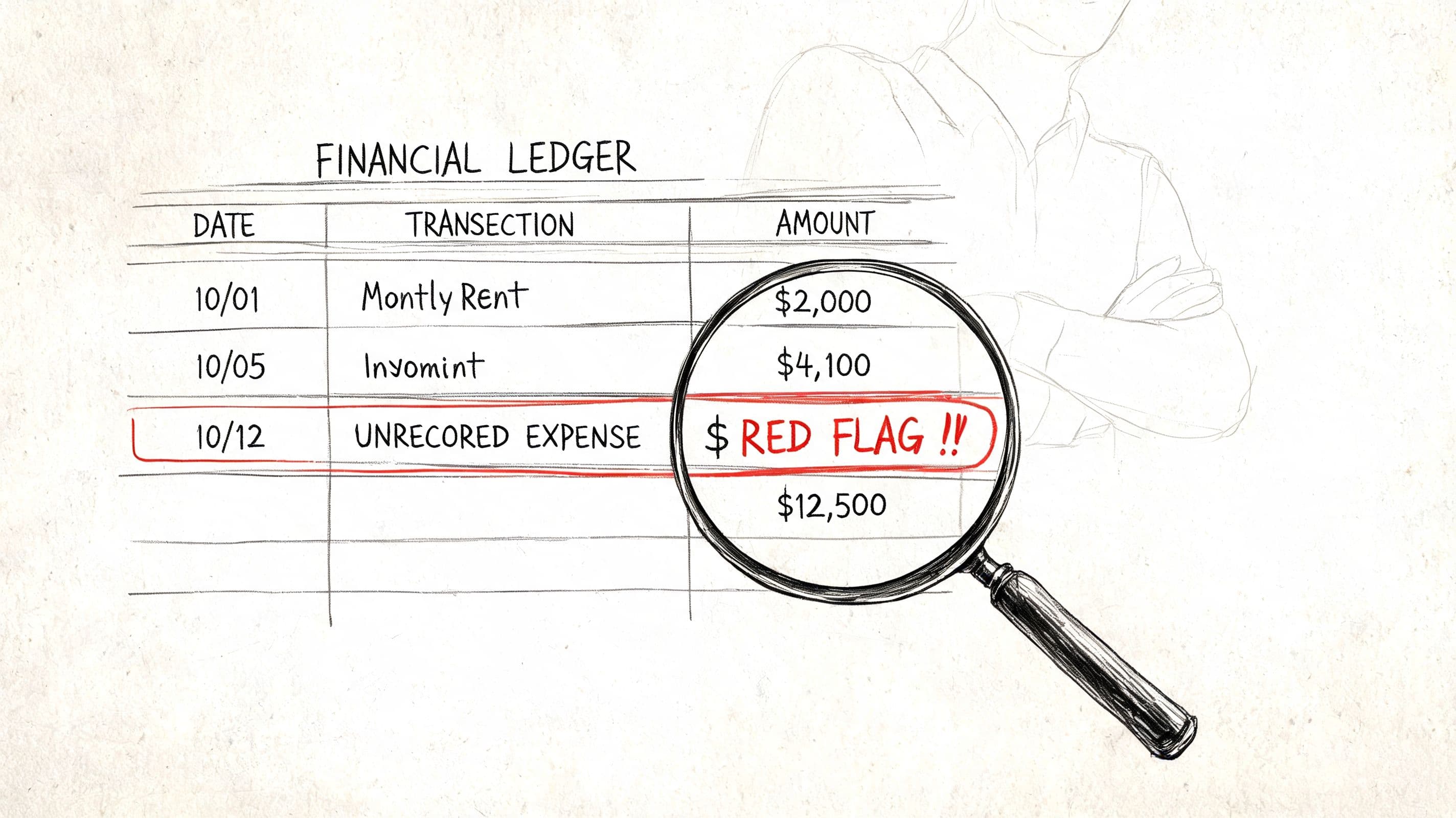

Revenue Red Flags That Kill Deals and Attract Audits

Investors and auditors don't start by asking whether your team works hard. They start by asking whether your numbers tie out.

When they review revenue, they're looking for evidence of control. If they don't find it, confidence drops fast. A bad revenue file signals more than a math problem. It signals weak finance leadership.

The red flags I'd fix immediately

According to a 2025 Shopify report, 45% of merchants in the $1M–$20M range mishandle multi-channel revenue aggregation, which leads to underreporting and missed growth visibility. The same source says 67% of agencies struggle with QuickBooks/Xero syncs for hybrid revenue models, delaying month-end closes by 15+ days. Those figures come from this Umbrex revenue contribution analysis page.

That lines up with what due diligence teams usually find in hybrid businesses.

Mixing cash and accrual in the same month

This is the fastest way to lose credibility. If some revenue is based on deposits and some is based on earned work, your P&L is contaminated.

What it signals: you don't have a reliable close process.

One top-line number with no channel support

If you sell through Shopify, Stripe, subscriptions, and service invoices, but report one revenue figure with no schedules behind it, nobody can validate the result.

What it signals: your reporting can't survive diligence.

Refunds, fees, and credits buried in random accounts

Channel platforms create noise. That's normal. Dumping all adjustments into a catch-all account is not.

What it signals: margin distortion and poor control over actual net revenue.

A revenue number that doesn't tie to supporting schedules isn't a metric. It's a claim.

What an outside reviewer expects to see

A serious reviewer wants this package:

| Expected support | Why it matters |

|---|---|

| Revenue by stream | Shows how total revenue was built |

| Contract or invoice support | Confirms existence and timing |

| Deferred revenue detail | Validates recognition timing |

| Refund and credit schedule | Tests quality of top-line revenue |

| Platform reconciliation | Confirms Shopify, Stripe, and accounting records align |

If any one of those breaks, the reviewer starts asking broader questions about controls, forecasting, and leadership.

Warning signs inside your own business

Use this checklist on yourself:

- Your monthly revenue changes after the close is “final.”

- Your sales report and accounting report disagree.

- You can't explain deferred revenue clearly.

- You need manual spreadsheet patches every month.

- You don't know revenue by channel without asking three people.

If those feel familiar, don't defend the system. Replace it.

Turn Accurate Revenue Data Into Strategic Growth

Accurate revenue reporting isn't an accounting finish line. It's the starting point for every smart operating decision you need to make next.

Once you calculate total revenue correctly, you can trust your forecasts. You can segment growth by channel. You can spot whether expansion revenue is masking churn, whether services revenue is propping up weak product demand, or whether discounts are eating the business from the inside.

What you should do next

- Document your revenue rules: Write down how each revenue stream is recognized. Subscriptions, projects, prepaid contracts, usage fees, and credits each need a clear rule.

- Segment your top line: Split recurring, one-time, usage-based, and services revenue in the P&L.

- Review your accounting system setup: Confirm deferred revenue and contra-revenue accounts are configured correctly.

- Reconcile every channel monthly: Shopify, Stripe, invoicing, and your accounting platform must agree.

- Automate reporting where possible: If you want cleaner visibility without chasing spreadsheets, this guide on how to monitor daily sales growth automatically is a practical way to tighten reporting rhythm.

- Build a repeatable close process: Revenue shouldn't depend on one employee remembering how last month was handled.

Bottom line: Clean revenue data lets you make aggressive decisions with less risk.

For founders who want fewer surprises, the next operational step is stronger automation and tighter reporting discipline. A good place to start is this overview of financial reporting automation, especially if your current process depends on exports and manual reconciliations.

If your revenue number is late, inconsistent, or impossible to defend, don't wait for a fundraise or audit to expose it. Fix it while the stakes are still manageable.

If you want help turning messy books into investor-ready financials, Jumpstart Partners can help. Their team supports growing SaaS, agency, and service businesses with outsourced controller and bookkeeping services, ASC 606 workflows, cleanup projects, and month-end reporting built for real decision-making.