Financial Operations

Cash Flow Forecasting Techniques for 2026 Leaders

Master cash flow forecasting techniques from direct and indirect methods to advanced models. A practical 2026 guide for SaaS, agency, and e-commerce growth.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··16 min readYour spreadsheet isn't giving you control. It's giving you false confidence.

The businesses that get blindsided by cash problems usually aren't the ones with no sales. They're the ones with decent revenue, a respectable P&L, and no reliable view of when cash lands or leaves. If you're running a SaaS company, agency, or services firm between $500K and $20M in revenue, cash flow forecasting techniques aren't academic finance theory. They're operating controls.

The first upgrade is mental. Stop asking, "Are we profitable?" Start asking, "What will cash look like every week, and what assumptions is that answer built on?" Once you do that, your hiring plan, vendor decisions, debt timing, and runway discussions get sharper fast.

Why Profitable Companies Go Bankrupt

Profit is an accounting outcome. Cash is survival.

You can post a strong month on the P&L and still miss payroll if customers pay late, annual software bills hit at once, tax payments bunch up, or you loaded expenses onto a corporate card without matching collections behind them. Founders get in trouble when they treat revenue recognition like bank balance.

Profit doesn't pay bills. Cash does.

A profitable business can still run out of money because timing drives liquidity. Your accounting system records revenue when earned and expenses when incurred. Your bank account only cares when dollars move.

That gap matters most in growing companies with:

- Long collection cycles: Clients pay on net terms while you fund payroll now

- Lumpy expenses: Insurance, taxes, contractor payouts, and annual renewals hit unevenly

- Recurring revenue with churn risk: SaaS looks predictable until late renewals and failed collections stack up

- Fragmented systems: Stripe says one thing, QuickBooks says another, and your bank tells the truth

If your forecast starts with "we should be fine because revenue is up," you're already behind.

Leadership owns liquidity

Cash management isn't a bookkeeping task you delegate and forget. It's a leadership discipline. If you're making hiring, pricing, or growth decisions without a current forecast, you're guessing with a nicer spreadsheet.

Good operators pair forecasting with broader effective financial risk techniques so they can spot weak assumptions before those assumptions become a funding problem. And if you already see warning signs such as late vendor payments, rising receivables, or constant transfers between accounts, fix those first by reviewing these common small business cash flow problems.

Practical rule: If you can't explain your next eight to thirteen weeks of cash movement without opening five systems and three tabs, you don't have a forecast. You have a ritual.

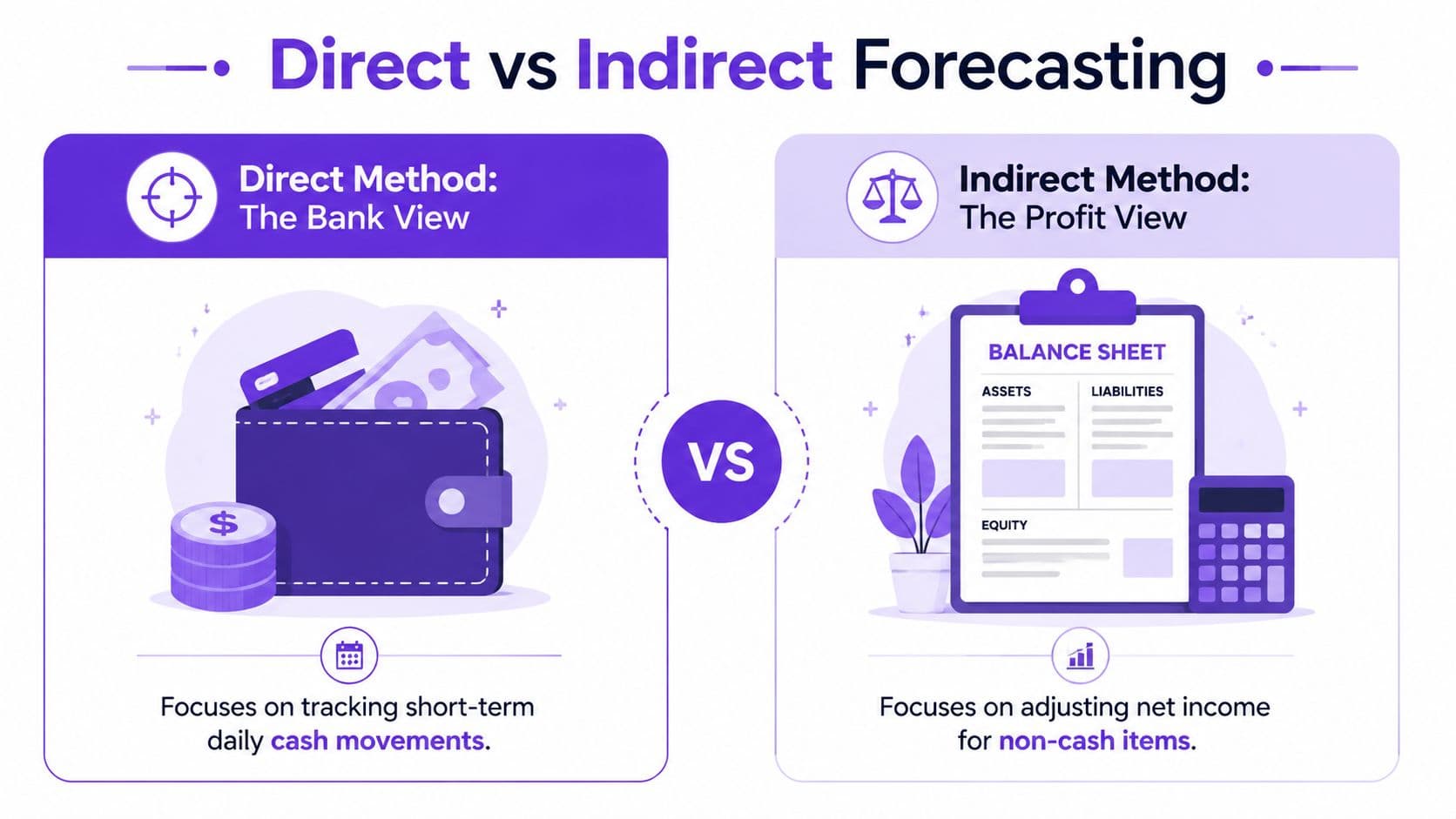

Direct vs Indirect Forecasting The Fundamental Choice

Most founders use the wrong forecast for the wrong job.

The direct method answers the question that matters in real operations: what cash comes in, what cash goes out, and when? The indirect method starts with projected profit and adjusts for non-cash items and working capital changes. That's useful for planning and reporting. It's weak for near-term control.

The bank view beats the profit view for operations

Think of it this way.

The direct method is like checking what will hit your bank account next week. The indirect method is like estimating your bank balance by starting with net income and making adjustments. One helps you schedule payroll. The other helps you explain performance.

According to Macabacus on direct cash flow forecasting, the direct method is ideal for short-term horizons of 90 days or less, and treasury benchmarks show accuracy exceeds 95% for 1 to 4 week forecasts versus 75% to 85% for indirect methods.

Direct vs. Indirect Cash Flow Forecasting

| Feature | Direct Method | Indirect Method |

|---|---|---|

| Starting point | Actual cash receipts and cash payments | Net income adjusted for non-cash items and working capital |

| Best use | Near-term liquidity decisions | Longer-term planning and financial statement alignment |

| Time horizon | Short-term, especially weekly and under 90 days | Medium and longer-term views |

| Data needed | Bank activity, AR collections timing, AP timing, payroll, subscriptions, debt payments | P&L forecast, balance sheet assumptions, working capital changes |

| Strength | Tells you whether cash will be there when bills hit | Connects forecasting to budgets and board reporting |

| Weakness | Requires cleaner operational data | Too abstract for daily and weekly decisions |

| Accuracy benchmark | Exceeds 95% for 1 to 4 week forecasts | 75% to 85% for 1 to 4 week forecasts |

My recommendation

If you're between $500K and $20M in revenue, use both methods, but don't confuse their roles.

Use the direct method to run the business. Use the indirect method to explain the business.

That means your weekly operating cadence should track cash receipts by customer timing, payroll dates, rent, debt service, software renewals, tax payments, and vendor terms. Then maintain an indirect view for board decks, annual planning, and lender conversations. If you need a refresher on the accounting statement behind all this, review how to read a cash flow statement.

The forecast that helps you avoid a cash crunch is the one tied to dates on the calendar, not just assumptions in a budget.

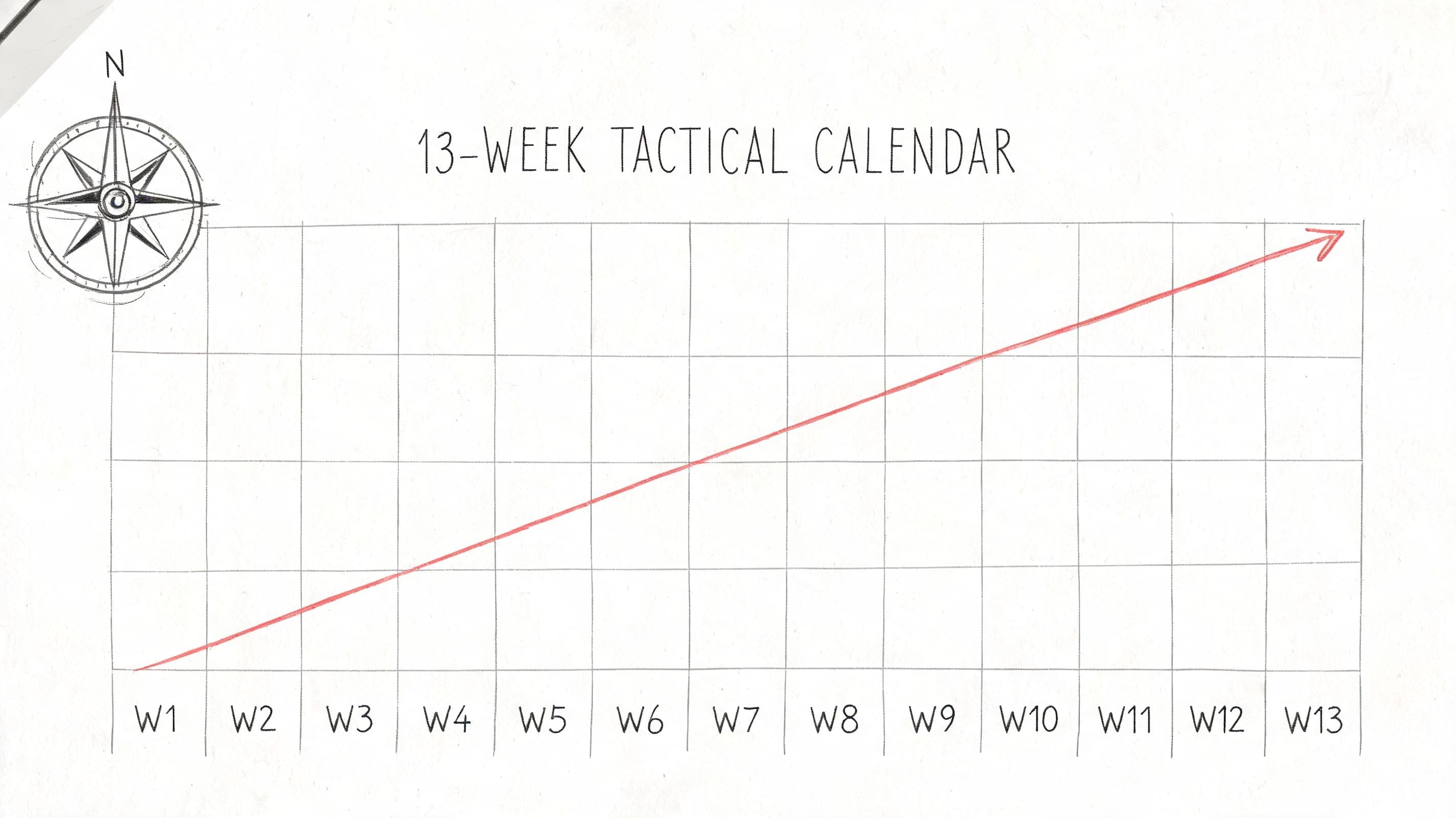

The 13-Week Cash Flow Forecast Your Tactical Playbook

If you only build one forecast, build a 13-week rolling cash flow forecast.

It gives you enough runway to act and not so much distance that the numbers turn fictional. Thirteen weeks is long enough to catch a hiring decision, a tax payment, a large vendor bill, or a collection slowdown before it becomes a crisis.

What goes into the model

Your 13-week forecast should live at the cash movement level, not the budget category level.

Track:

- Opening cash: Reconciled bank balance across all operating accounts

- Customer collections: Expected receipts by week based on invoice age, billing platform, and customer behavior

- Other inflows: Financing, owner contributions, refunds, tax credits if applicable

- Fixed outflows: Payroll, rent, debt service, insurance, software

- Variable outflows: Contractor spend, ad spend, inventory, commissions, one-time projects

- Ending cash: Opening cash plus inflows less outflows

A worked example

Assume you start Week 1 with $180,000 in cash.

For that week, you expect:

- Collections from customers: $42,000

- A new annual prepayment from a client: $18,000

Total inflows = $60,000

You also expect:

- Payroll: $38,000

- Rent: $6,000

- Software and tools: $4,000

- Contractors: $12,000

- Debt payment: $5,000

Total outflows = $65,000

Net cash for Week 1 = $60,000 - $65,000 = -$5,000

Ending cash for Week 1 = $180,000 - $5,000 = $175,000

That ending cash becomes Week 2 opening cash.

Now assume in Week 2 a large customer payment of $30,000 slips into Week 3. Your Week 2 forecast changes immediately. That's the value of the model. It forces action while you still have options.

How to run it every week

A 13-week forecast only works if you treat it like an operating meeting, not a file.

- Replace forecast with actuals: Close the prior week with real cash activity

- Explain variances: Was the miss caused by timing, collections, spending, or bad assumptions?

- Roll forward one week: Keep the horizon at 13 weeks at all times

- Flag low-cash weeks early: If a trough appears, decide now whether to collect faster, delay spend, or change plans

If you want a deeper implementation guide, use this 13-week cash flow forecasting framework.

Near-term visibility changes behavior. Teams collect faster, delay lower-priority spend, and stop pretending timing issues will sort themselves out.

Advanced Forecasting Models For Strategic Planning

Once your weekly cash control is in place, you need a second layer. Stronger cash flow forecasting techniques start answering strategic questions instead of just tactical ones at this stage.

You're no longer asking only, "Can we make payroll?" You're asking, "What happens to cash if churn rises, sales cycles slow, or we hire ahead of revenue?"

Regression and driver-based forecasting

Manual forecasting breaks down when your business has multiple moving parts. SaaS and agency businesses rarely have one clean revenue stream. They have retainers, projects, annual contracts, usage-based billing, delayed collections, seasonal demand, and changing payroll load.

According to Resolve on predictive cash forecasting, regression-based statistical forecasting methods increase prediction accuracy by an average of 25% compared to manual methods, and 80% of businesses using data-driven forecasts identify potential cash shortages earlier. That's because the model can analyze multiple variables at once, including payment history, seasonal trends, customer behavior, and economic indicators.

Time series for recurring patterns

If you have enough clean history, time series forecasting helps you establish a baseline from actual behavior rather than executive optimism.

Methods such as ARIMA and exponential smoothing work well when cash has recurring patterns, especially in subscription and repeat-purchase models. A useful implementation path is:

- Start simple: Build a baseline from historical monthly or weekly inflows

- Layer business drivers: Add known changes such as hiring, pricing, churn, or major contracts

- Add scenario cases: Base case, downside case, and an operational stress case

- Refresh on real data: Don't let old assumptions sit untouched for a quarter

For a practical planning cadence, pair this with a rolling forecast approach for growing companies.

A worked strategic example

Assume your SaaS company currently collects $120,000 in monthly cash receipts and pays $95,000 in monthly cash outflows. Baseline net monthly cash generation is $25,000.

Now model a downside case:

- Monthly cash receipts drop to $108,000

- Payroll and fixed operating costs remain $95,000

- Planned software and contractor expansion adds $10,000

Revised net monthly cash = $108,000 - $105,000 = $3,000

That doesn't mean you're unprofitable. It means your planned expansion nearly eliminates monthly cash cushion. That's exactly the kind of strategic mistake a driver-based model catches before you make it.

Forecasting Examples For SaaS Agencies and E-commerce

Generic forecasting advice fails because business models move cash differently. The right technique depends on how you bill, how customers pay, and what systems hold the data.

SaaS example with churn and AR timing

The standard SaaS mistake is smoothing revenue and assuming collections follow. They don't.

According to Numeric's cash flow forecasting guide for accounting and FP&A teams, a common forecasting error in SaaS is failing to model seasonality and AR aging from late payers, which masks liquidity shortfalls. The same source notes that 90% of treasurers rate forecast accuracy as unsatisfactory due to poor inputs, and recommends segmenting AR by cohort payment behavior from Stripe data and layering probabilistic churn models.

Here's a basic cash example.

Assume you have:

- 40 customers paying $500 monthly = $20,000

- 10 customers paying $1,500 monthly = $15,000

- Total expected monthly billings = $35,000

Now segment payment behavior:

- Cohort A pays on time and represents $24,000

- Cohort B regularly pays late and represents $11,000

If you expect all $35,000 in the month, your forecast is overstated. If your actual collection assumption for the month is:

- Cohort A collections = $24,000

- Cohort B collections this month = $6,000

- Remaining $5,000 slips into later weeks

Then expected monthly cash receipts are $30,000, not $35,000.

Now add churn. Assume recurring billings next month fall by $2,000 from cancellations. Your next-month billing run rate becomes $33,000 before new sales. That cash effect matters immediately even if your revenue reporting smooths the impact differently.

Founder test: If your SaaS forecast doesn't separate billed revenue, collected cash, and likely churn impact, it isn't a cash forecast.

Agency example with utilization and payment terms

Agencies often think pipeline equals cash. It doesn't. Signed work, invoiced work, and collected work are three different numbers.

Assume:

- Retainer client A pays $12,000 monthly

- Retainer client B pays $8,000 monthly

- Project work invoiced this month totals $25,000

- Total invoices issued = $45,000

Now apply terms:

- Retainers collected this month = $20,000

- Project invoices on net terms collect at 50% this month = $12,500

Expected cash receipts = $32,500

Outflows:

- Payroll = $24,000

- Freelancers = $6,000

- Software and overhead = $4,500

Total outflows = $34,500

Net monthly cash = $32,500 - $34,500 = -$2,000

Your P&L may still look fine because the full $45,000 sits in revenue. Cash says otherwise. That's why agencies need weekly collection assumptions tied to contract terms and client history.

E-commerce example with Shopify, Stripe, and inventory timing

E-commerce is where spreadsheet forecasting usually collapses first because cash drivers sit in different systems. Sales hit Shopify. Collections settle through Stripe. Payroll runs through Gusto. Inventory sits on its own purchase cycle.

Assume this month:

- Shopify sales expected to settle in cash = $80,000

- Refunds and chargebacks = $3,000

- Net inflow from sales = $77,000

Outflows:

- Inventory purchase = $35,000

- Payroll = $18,000

- Ad spend = $14,000

- Apps, shipping adjustments, and overhead = $9,000

Total outflows = $76,000

Net monthly cash = $77,000 - $76,000 = $1,000

That looks manageable until inventory terms tighten or ad spend lands before sales settle. That's why DTC brands need daily or weekly direct-method forecasting tied to platform settlement timing, not monthly summaries.

Common Forecasting Pitfalls and How to Avoid Them

Most bad forecasts fail for boring reasons. The model isn't the issue. The inputs, update habits, and decision discipline are.

Red flags you shouldn't ignore

If any of these sound familiar, your forecast is weak:

- You update it after month-end only: That's reporting, not forecasting

- Sales owns the revenue number without finance challenge: Optimism isn't a collection policy

- Your opening cash doesn't match reconciled bank balances: Every period after that is contaminated

- You ignore timing differences: Annual bills, tax payments, and debt service don't care about monthly averages

- One spreadsheet owner controls everything: That's key-person risk dressed up as process

The integration problem is real

For scaling e-commerce businesses, the biggest operational problem is often data fragmentation. According to EY's analysis of cash forecasting urgency and complexity, siloed data from systems like Shopify, Stripe, and Gusto can require hundreds of hours of manual collation, and the disconnect between sales, procurement, and finance obscures true cash drivers. The same source notes that AI-driven reconciliation of this multi-entity data has cut cash shortfalls by 30%.

That problem isn't limited to e-commerce. Agencies and SaaS teams run into the same issue when billing, payroll, AP, and bank data live in separate tools.

What to do instead

Build discipline around a few essential practices:

- Use reconciled data first: Never start with stale balances

- Separate timing from amount: Many misses are timing errors, not volume errors

- Review variances weekly: Every variance should improve the next forecast

- Stress-test your assumptions: Late payments, churn, delayed deals, and vendor acceleration belong in the model

- Challenge the objection that accounting software already does this: QuickBooks records history well. It doesn't replace a founder-grade forward cash model

"Unit economics are the truth serum for SaaS businesses. You can have beautiful growth charts, but if your cash flow doesn't work, you're just a pretty graph on the way to zero."

Jason Lemkin, SaaStr

Automating Your Forecast with the Right Tech Stack

Manual exports are the tax you pay for not fixing your finance stack.

If your team still downloads CSVs from Stripe, copies Shopify payout data into Excel, pulls payroll from Gusto, and then tries to map everything back to QuickBooks or Xero, your forecast will stay late, fragile, and hard to trust.

What an effective stack looks like

A useful operating setup usually includes:

- General ledger and close system: QuickBooks, Xero, or NetSuite

- Billing and collections data: Stripe, Shopify, or invoicing tools

- Payroll and people costs: Gusto or BambooHR-connected payroll workflows

- Cash reporting layer: A forecast model or platform that maps timing by week

- Automation and reconciliation controls: So actuals feed the forecast quickly

If you still receive bank data in messy formats, use a practical client-side financial data conversion guide before it reaches your model. Clean inputs save hours of avoidable rework.

One option in this market is Jumpstart Partners, which supports outsourced controller and bookkeeping workflows for growing businesses and integrates with tools such as QuickBooks, Xero, NetSuite, Stripe, Shopify, and Gusto. The broader point matters more than the vendor. Your forecast should pull from systems of record, not from whatever file someone exported last Friday.

How automation changes the workflow

Automation doesn't mean finance stops thinking. It means finance stops retyping.

A good process:

- Pulls actual cash activity from connected systems

- Reconciles opening balances before forecasting

- Updates weekly inflow and outflow expectations

- Flags variances and unusual movement for review

- Produces a rolling decision-ready cash view

For more on that architecture, review this guide to automation of financial reporting.

A short walkthrough helps if you're redesigning the process:

What you should do next

Don't start by buying software. Start by fixing the operating design.

- Map your systems: List where cash data lives

- Choose one forecast owner: Accountability first

- Build a 13-week direct-method model: Weekly buckets, reconciled opening cash

- Connect your core sources: Bank, GL, billing, payroll, and AP

- Review every week with leadership: Collections, spend, and near-term decisions on the table

A forecast should help you decide whether to hire, delay spend, push collections, or raise capital sooner. If it can't do that, rebuild it.

If you want a tighter forecasting process tied to your actual systems and operating cadence, talk to Jumpstart Partners. They help growing companies turn messy books, delayed closes, and spreadsheet-driven cash management into a usable weekly forecast and cleaner finance operations.