Financial Operations

Debt Service Coverage Ratio: Founder's Guide to Securing

Learn how the debt service coverage ratio impacts your ability to secure business loans. Essential guide for founders navigating funding in 2026.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··20 min readA lender can like your growth story and still decline your loan because of one ratio. Debt service coverage ratio is where that happens.

The core benchmark is brutally simple. A DSCR of 1.0 means your operating cash flow exactly covers annual debt service. Below 1.0 means a shortfall. Above 1.0 means some cushion, and many commercial lenders look for about 1.2 to 1.25 as a minimum, while some business-banking guidance says 2.0 or higher is generally healthy, as summarized by UNC and Commerce Bank guidance. If you're a SaaS founder, agency owner, or services CEO, that's the metric that decides whether your business looks financeable or fragile.

Most founders learn DSCR too late. They apply for debt because revenue is growing, then discover the bank cares less about top-line momentum and more about whether cash covers principal and interest with room to spare. If you want debt on usable terms, you need to know this number before the lender tells you.

Table of Contents

- Why You Must Understand Debt Service Coverage Ratio

- Calculating Your Debt Service Coverage Ratio

- How Lenders Interpret Your DSCR Score

- DSCR Benchmarks for SaaS Agencies and E-commerce

- Common DSCR Adjustments and Accounting Nuances

- A Practical Guide to Improving Your DSCR

- Build a Bankable Business Today

Why You Must Understand Debt Service Coverage Ratio

If you're trying to add a credit line, equipment financing, or acquisition debt, DSCR is the first serious filter. Your revenue can be climbing, your pipeline can look strong, and your customer retention can be solid. If the lender doesn't see enough cash coverage over debt payments, the conversation stalls.

That matters even more in asset-light businesses. SaaS companies often reinvest heavily in product and growth. Agencies can show healthy billings but still carry lumpy collections. Professional services firms can be profitable on paper while partner draws and timing issues squeeze cash. DSCR forces all of that into one question. Can this business service debt?

Practical rule: If you don't know your DSCR before you talk to a lender, you're negotiating from weakness.

Founders also confuse profit with debt capacity. Those are not the same thing. A business can look good on the P&L and still fail the lender's repayment test because debt gets paid with cash, not narrative. That's why understanding the link between operating performance and cash generation matters so much. If you need a refresher on that connection, read why cash flow matters for business decisions.

What founders get wrong

- They lead with growth. Lenders care about repayment first.

- They use net income. Most underwriting starts higher up the earnings stack.

- They ignore annual debt service. Monthly payments feel manageable until the annual number lands in the denominator.

- They wait until the application. By then, you can't fix the story fast enough.

The real business impact

DSCR doesn't just influence approval. It affects how much a lender is willing to advance and how much cushion they require. In practice, the ratio shapes your borrowing capacity, your covenant package, and how aggressively you can scale with debt.

If you're running a business in the $500K to $20M revenue range, this isn't a back-office metric. It's a financing metric, a planning metric, and a survival metric.

Calculating Your Debt Service Coverage Ratio

A lender can reject a profitable company in five minutes if the DSCR math does not hold up. That happens all the time with SaaS firms and agencies because founders start with the P&L, then forget the debt schedule.

Start with the standard lender formula

Use the standard formula:

DSCR = EBITDA ÷ annual principal + interest payments

For an asset-light business, the math is easy. Getting the inputs right is where founders make mistakes. Banks want operating earnings for a defined period, matched against the debt payments due in that same period. If you use quarterly EBITDA and annual debt service, or leave one loan off the schedule, your ratio is useless.

You need two numbers.

| Input | What to pull | Where founders usually slip |

|---|---|---|

| EBITDA | Earnings before interest, taxes, depreciation, and amortization | Using net income, which includes financing and tax noise |

| Annual debt service | Scheduled principal plus interest for the same period | Leaving out a term loan, shareholder note, or equipment financing |

If your books do not clearly separate operating results from below-the-line items, use this guide to calculate income from operations before you finalize DSCR.

Match the period. Reconcile every loan. Use booked numbers, not optimistic assumptions.

A worked example for a service business

Here is a cleaner example for the kinds of companies that read this article.

Say a marketing agency has trailing twelve-month EBITDA of $360,000. It also has a term loan with $180,000 of annual principal and interest payments. DSCR is:

$360,000 ÷ $180,000 = 2.0x

| Step | Amount |

|---|---|

| EBITDA | $360,000 |

| Annual principal + interest | $180,000 |

| DSCR | 2.0x |

That means the agency generates $2.00 of operating earnings for every $1.00 of required debt service.

Now take a SaaS company. If it shows $600,000 of EBITDA but owes $500,000 annually across a bank loan and founder note, DSCR is only 1.2x. On paper, that may look passable to a founder focused on growth. To a lender, it says there is very little room for churn, delayed collections, or a bad quarter.

Pull the inputs from the right places

Use a controller's process, not a back-of-the-napkin estimate.

- Pull trailing twelve-month EBITDA from your P&L. Clean up expense classification first, especially owner compensation, one-time legal fees, and non-operating items.

- Build a full debt schedule. Include every required principal and interest payment in the same twelve-month period.

- Tie the numbers back to statements. Your numerator should tie to the financials. Your denominator should tie to loan agreements and amortization schedules.

- Pressure-test the result against cash flow. If EBITDA says coverage is fine but cash is constantly tight, review how to read a cash flow statement and spot working-capital pressure.

One sentence matters here. DSCR is not a bookkeeping exercise. It is an underwriting exercise.

What to include for SaaS, agencies, and other asset-light businesses

Asset-light does not mean debt-light. If the company owes the payment, include it.

That means term loans, SBA debt, equipment financing, and any other contractual principal and interest payments belong in the denominator. For SaaS companies, revenue may be recurring, but churn and sales efficiency can move fast. For agencies, client concentration and delayed receivables can turn a decent DSCR into a cash squeeze quickly. That is why a clean base-case calculation matters more than the story around it.

Start with the unadjusted number. Then review adjustments later if they are legitimate and documented. That order keeps you honest and gives your lender a ratio they can trust.

How Lenders Interpret Your DSCR Score

Lenders don't stare at DSCR because they love ratios. They use it because it compresses operating performance and repayment burden into one credit signal.

What the thresholds mean

A ratio under 1.0 means the business doesn't generate enough operating cash flow to cover debt service. That's not a minor issue. That's a repayment problem.

Across commercial lending, minimum DSCR covenants typically cluster around 1.25x to 1.5x, according to the DSCR reference summary on Wikipedia. That range exists for a reason. A 1.25x covenant implies that a 20% drop in operating income pushes the borrower to break-even 1.0x coverage. At 1.5x, the lender has more room for volatility.

Some business-banking guidance also treats 2.0 or higher as generally healthy, but don't get complacent if you're there. A strong DSCR can still hide billing concentration, churn risk, or ugly working-capital behavior.

Lender lens: DSCR is not just a yes-or-no metric. It tells the bank how much pain your business can absorb before debt becomes the problem.

Here's a practical interpretation table for founders:

| DSCR range | What it signals to a lender | Founder takeaway |

|---|---|---|

| Below 1.0 | Cash shortfall against debt service | Fix operations or restructure debt before applying |

| Around lender minimums | Thin buffer | Expect tighter scrutiny and less flexibility |

| Solid cushion | Better resilience | You're more likely to negotiate from strength |

| 2.0 or higher | Strong coverage under many business-banking standards | Good position, assuming cash conversion is real |

If you want to understand why debt structure itself changes lender behavior, review how cost of debt affects borrowing decisions.

Red flags lenders spot fast

Banks and credit committees look for patterns, not just one clean ratio.

- Thin coverage with volatile revenue: Agencies with uneven client concentration get hit here.

- Strong EBITDA but weak cash: Lenders know collections delays can break debt service.

- New debt piled onto old debt: A fresh facility doesn't erase existing obligations.

- Covenant math that barely works: If the ratio only holds under optimistic assumptions, underwriters will discount it.

If your DSCR only works on your best month or your cleanest quarter, it doesn't work.

This explainer is also worth watching if you want a plain-English breakdown before your next lender call.

Why covenants matter after closing

Founders often treat DSCR as an approval hurdle. That's incomplete. It usually stays in the deal as a covenant, which means the lender can monitor whether your business continues to maintain minimum coverage.

That changes how you should forecast. If you're a SaaS company adding debt while collections stretch or implementation costs spike, you need to know whether the ratio still holds in weaker periods. If you're an agency with project-based revenue, you need to model the downside case, not just your booked work.

A lender isn't asking whether you can make the next payment. They're asking whether your company can stay bankable.

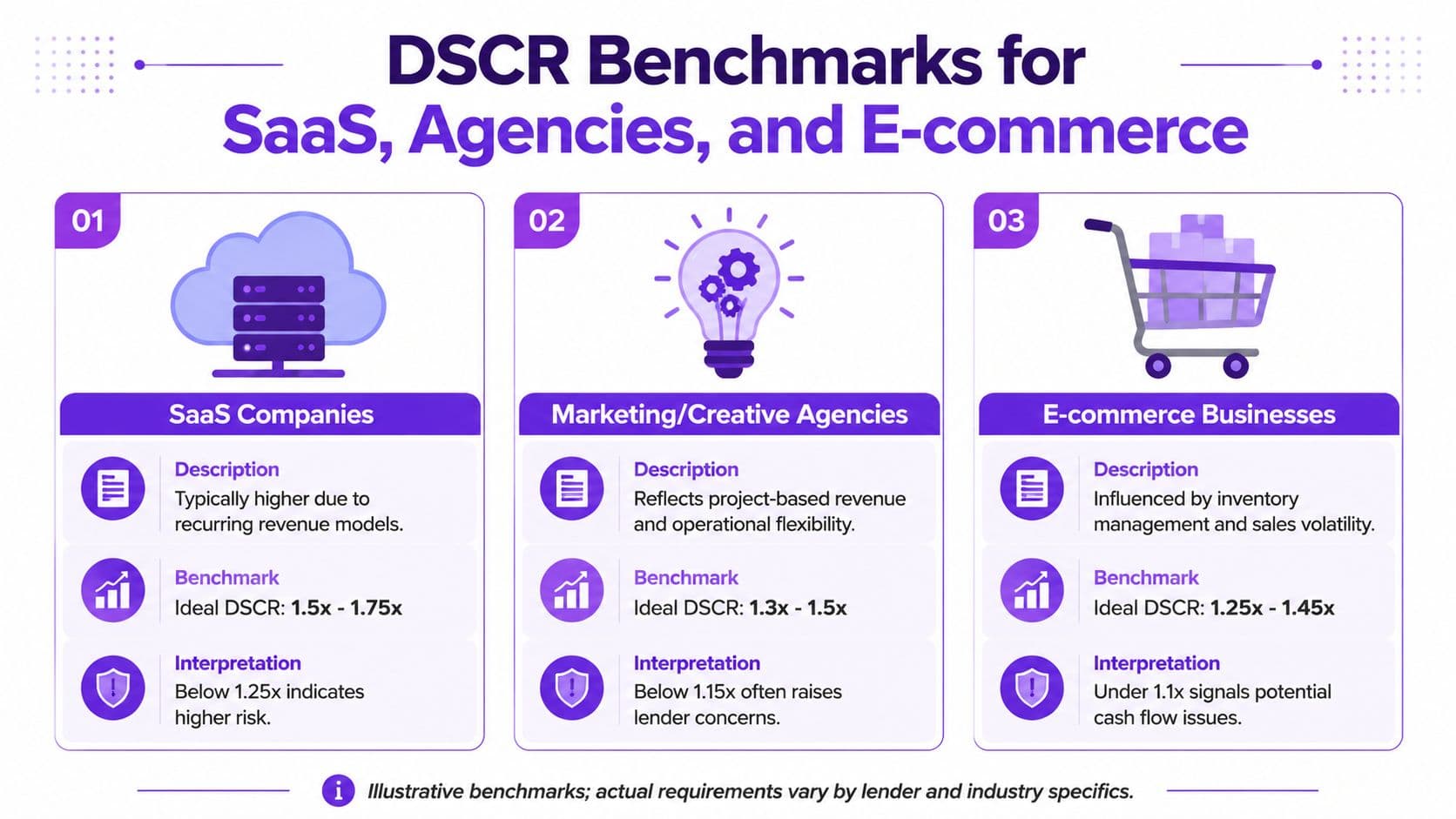

DSCR Benchmarks for SaaS Agencies and E-commerce

A 1.30x DSCR can get one company approved and push another into a credit committee debate. Founders of asset-light businesses need to stop borrowing benchmark language from real estate and start reading DSCR the way a lender reads operating risk.

Why the same ratio means different things

Banks still start with a familiar floor. In many commercial lending situations, lenders want to see DSCR land around 1.25x to 1.5x. That baseline matters, but it does not tell the whole story for SaaS, agencies, or e-commerce.

For these businesses, the core question is simple. How much of your reported earnings turns into cash that is available for debt payments?

A SaaS company can post clean margins and still scare a lender if collections drag, churn is rising, or implementation work is consuming cash. An agency can survive with a similar ratio if billing is tight, contracts renew consistently, and no single client controls the quarter. An e-commerce brand can show respectable profitability and still have weak debt capacity because inventory, returns, and paid acquisition eat the cash before the loan payment comes due.

In asset-light businesses, DSCR is less about asset coverage and more about cash conversion discipline.

Typical DSCR targets by business model

Use these ranges as operating targets, not trophies.

| Industry | Practical DSCR Target | What lenders focus on |

|---|---|---|

| SaaS | 1.35x to 1.75x | Net revenue retention, collections speed, deferred revenue quality, implementation burden, and whether revenue recognition matches actual cash behavior |

| Digital agencies | 1.25x to 1.60x | Client concentration, gross margin stability, staff utilization, contract length, invoicing discipline, and owner dependence |

| E-commerce | 1.40x to 1.80x | Inventory turns, return rates, supplier terms, ad spend volatility, contribution margin after fulfillment, and seasonal cash compression |

Those ranges are practical because lenders usually underwrite these models differently, even when the headline DSCR looks similar.

What a lender sees in each model

SaaS:

A lender will usually give you some credit for recurring revenue. You only keep that credit if your retention is solid and your cash collection is clean. If you book annual contracts but let receivables stretch to 75 days, your DSCR deserves more scrutiny than the P&L suggests. If your revenue policies are muddy, fix that before the bank asks questions. Founders should clean up ASC 606 revenue recognition for subscription and service revenue before presenting covenant math.

Agencies:

Agencies live or die on operating discipline. A 1.30x DSCR with monthly retainers, no client above 20% of revenue, and invoicing on day one of the month is financeable. The same 1.30x with project work, long approval cycles, and a founder who personally rescues every account is weak. Lenders know agencies can cut spend quickly. They also know revenue can disappear quickly.

E-commerce: In e-commerce, founders most often fool themselves. EBITDA can look fine while cash is trapped in inventory reorders, return reserves, and ad spend. If your business has a holiday spike or has to prepay suppliers, your DSCR target should be higher than the generic floor because the downside quarter gets ugly fast.

Controller-level benchmark guidance

If you run an asset-light business and want bank debt on reasonable terms, use this standard:

- Below 1.25x: weak. Expect pricing pressure, tighter structure, or a decline.

- 1.25x to 1.40x: passable, but only with stable revenue and clean financials.

- 1.40x to 1.75x: bankable for many SaaS, agency, and e-commerce borrowers if cash conversion supports the number.

- Above 1.75x: strong. You have room for normal volatility and a better shot at negotiating terms.

That is the founder translation banks rarely spell out. The ratio itself is only the opening screen. The underwriting decision comes from how believable the cash flow is behind it.

If you want a reference point for how commercial lenders frame debt capacity beyond a single metric, this overview of EHF Mortgages business finance is useful. The lesson for founders is straightforward. Do not manage to a generic minimum. Build enough coverage to survive a slow quarter, a collections slip, or a bad inventory cycle without breaching the loan.

Common DSCR Adjustments and Accounting Nuances

A clean 1.40x DSCR can turn into 1.10x fast once a lender strips out weak add-backs and replaces EBITDA with actual cash flow. Founders of SaaS companies, agencies, and other asset-light firms get surprised here all the time because their internal number is built for management reporting, not credit underwriting.

There is no single universal DSCR formula

Banks do not all calculate DSCR the same way. The numerator shifts based on lender policy, deal type, and how much trust they place in your accounting. Some use EBITDA. Some use operating income. Some move closer to cash flow. As noted earlier, even standard lender guidance only helps after the formula is defined.

For founders, the practical point is simple. If you do not know what your lender will add back, exclude, or haircut, your DSCR is only a draft.

The biggest adjustment areas in asset-light businesses are usually these:

- Owner compensation: If the founder pays themselves $350,000 and the market replacement cost is $180,000, a lender may add back $170,000. If distributions are mixed with payroll and not documented well, expect pushback.

- One-time expenses: A $90,000 ERP cleanup, $60,000 legal dispute, or $120,000 rebrand can be added back if you can prove it was unusual and non-recurring. If the same "one-time" line shows up every year, it stays.

- Contractor and delivery labor: Agencies often try to treat freelance labor as adjustable. Lenders usually reject that. If contractors are required to deliver client work, that is an operating cost, not an add-back.

- Rent and software: Founders love to call these discretionary. Credit teams usually do not. If the business needs the office, the platform, or the tool stack to operate, those costs belong in the run rate.

- Revenue recognition: SaaS companies with implementation fees, usage-based billing, or multi-element contracts need clean policies. If your books are messy under ASC 606, lenders will question earnings quality. Review this guide to ASC 606 revenue recognition for SaaS and service businesses before presenting adjusted results.

Controller view: DSCR is where accounting policy meets bank risk policy.

Why institutional lenders use CFADS

Many lenders, especially on larger or more structured deals, care less about EBITDA and more about Cash Flow Available for Debt Service, or CFADS. Breaking Into Wall Street's explanation of project finance DSCR and CFADS lays out the logic well. Start with operating earnings, then subtract the cash drains that reduce debt capacity, such as taxes, maintenance capital spending, and working capital needs.

That approach is stricter. It is also closer to reality.

A SaaS company can post strong EBITDA and still miss cash targets because annual contracts are collected late, commissions are paid upfront, and implementation payroll hits before the customer goes live. An agency can show a healthy margin in the P&L while receivables stretch to 75 days and client deposits shrink. EBITDA misses those issues. CFADS catches them.

The practical implication for founders

Walk into the bank meeting with a bridge from book earnings to lender-style cash flow. If your reported EBITDA is $1.2 million, show exactly how you get to adjusted EBITDA, then to cash available for debt service. Spell out the $150,000 founder comp normalization, the $80,000 one-time legal bill, the $200,000 receivables build, and the actual annual debt service requirement. That is how you control the conversation.

Use this framework:

| Version | What it emphasizes | Why it changes the discussion |

|---|---|---|

| EBITDA-based DSCR | Core operating earnings | Fast screen for smaller loans and simpler deals |

| Operating income or NOI variants | Lender-specific income definitions | Can reduce comparability across term sheets |

| CFADS-based DSCR | Cash left after real business cash drains | Better test for whether debt can actually be paid |

If two lenders produce different DSCR numbers from the same financials, they are usually underwriting different risks, not making a math error. Your job is to know which version matters before you negotiate structure, pricing, or loan size.

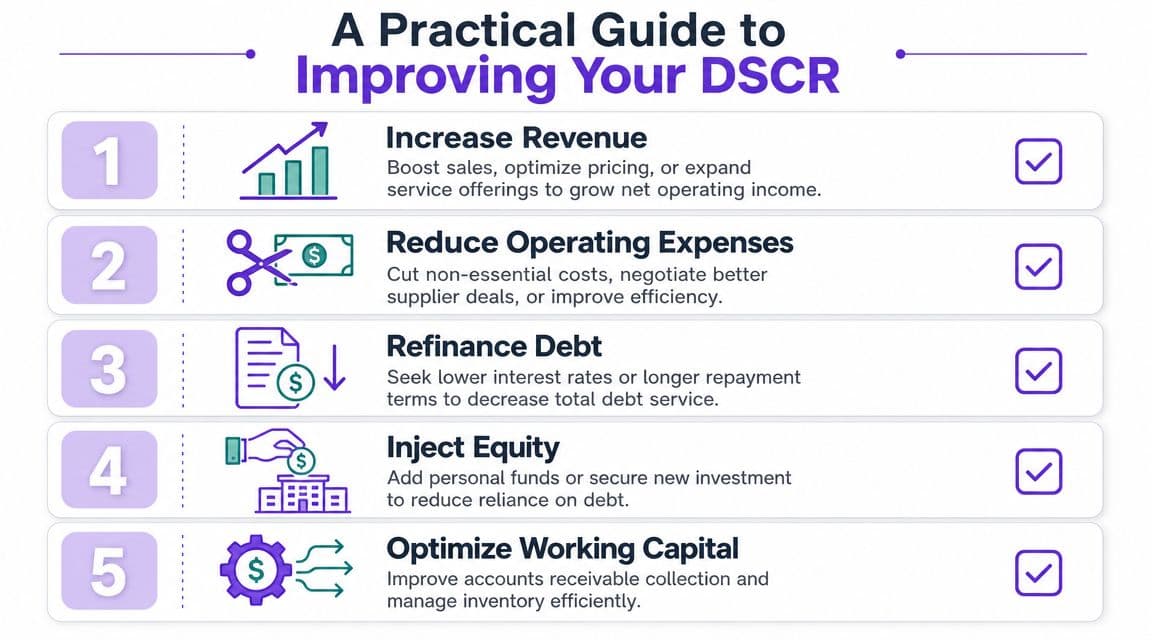

A Practical Guide to Improving Your DSCR

You improve DSCR in only two ways. Increase the cash available to service debt, or reduce the debt service burden. Everything else is decoration.

Improve the numerator

Start with operating performance that converts to cash.

- Raise quality of revenue: For SaaS, push annual prepay where it fits your model. For agencies, tighten scopes and eliminate underpriced work. For professional services, move faster on utilization and billing discipline.

- Cut low-value overhead: Don't trim expenses blindly. Cut software sprawl, redundant contractors, and delivery inefficiencies that don't support margin.

- Fix collections: A decent DSCR on paper won't save you if receivables age badly. Faster invoicing and tighter follow-up improve real cash coverage. If cash is constantly tight, revisit practical ways to improve cash flow.

Stronger DSCR usually starts with operational discipline, not financial engineering.

Reduce the denominator

If debt service is the problem, attack it directly.

- Refinance expensive or short-duration debt. Longer amortization or lower pricing can reduce annual principal and interest burden.

- Consolidate fragmented obligations. Multiple small facilities often create unnecessary payment pressure.

- Use equity for the wrong debt. If you've funded long-term initiatives with short-term debt, fix the capital structure.

- Delay nonessential financed purchases. Don't stack fresh payments onto a ratio that's already thin.

Build a lender-ready action list

Use a simple checklist before you ask for debt.

| Action | What to review | Intended effect on DSCR |

|---|---|---|

| Rebuild EBITDA | Clean expense coding and remove obvious noise | Clarifies the numerator |

| Tighten collections | AR aging, invoice timing, client payment behavior | Improves cash conversion |

| Rework debt schedule | Principal, interest, maturity profile | Lowers denominator pressure |

| Stress test forecast | Base, downside, and slower-cash scenarios | Shows whether coverage holds |

| Prepare adjustment memo | Owner pay, one-time items, policy explanations | Helps defend the calculation |

Common objection from founders

The pushback I hear most is this: "We're growing fast, so the ratio will take care of itself."

No. Growth can hurt DSCR if it requires hiring ahead of revenue, longer implementation cycles, heavier ad spend, or more working capital. Fast growth with weak cash discipline is exactly how founders end up surprised by a lender decline.

Track DSCR monthly. Forecast it quarterly. Manage it before you need it.

Build a Bankable Business Today

Treat debt service coverage ratio as an operating metric, not just a banking metric. That's the shift.

Your action plan is straightforward. First, calculate your current DSCR using your real operating earnings and full annual debt service. Second, identify the handful of levers that will move it most, usually margin quality, collections, or debt structure. Third, build a forecast that shows how the ratio holds under pressure, not just in your best-case month.

That process makes your business stronger even if you never borrow. It forces discipline around earnings quality, cash conversion, and capital structure. That's what lenders trust, and it's what buyers and investors respect too.

If you want help turning messy books, uneven cash flow, and unclear lender math into a clean financing story, Jumpstart Partners can help. Their outsourced controller team works with SaaS, agencies, and growing businesses to tighten financial reporting, improve cash visibility, and build lender-ready forecasts that support a stronger DSCR.