Financial Operations

Why Is Cash Flow Important? a Founder's Guide to Growth

Learn why is cash flow important for growing your business. We cover key metrics, profit vs. cash, and actionable strategies for SaaS, agencies, and e-commerce.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··16 min readRevenue doesn't keep your company alive. Cash does.

If you want the blunt answer to why cash flow is important, here it is: cash flow determines whether you can make payroll, pay vendors, stay in control of your growth plan, and avoid raising money on bad terms. A business can look healthy on a P&L and still be one delayed customer payment away from a mess. That isn't a bookkeeping issue. It's a leadership issue.

For founders in SaaS, agencies, and e-commerce, cash flow is also a valuation issue. A stronger cash position gives you more negotiating power with lenders and investors, and better cash flow quality is associated with lower cost of debt and equity capital, according to Phocas Software's summary of a 2017 Journal of Financial Economics study.

Table of Contents

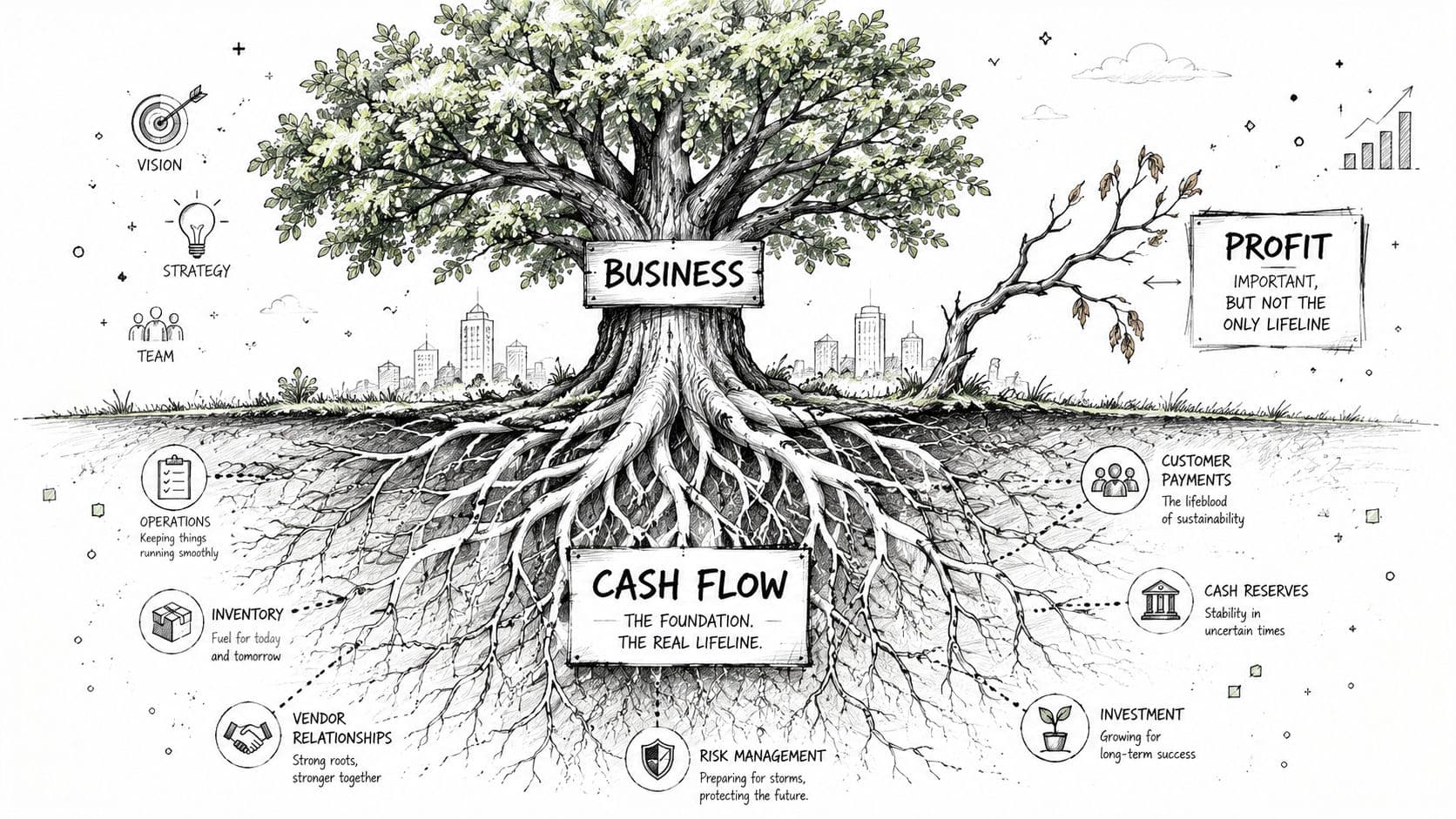

- Your Business's True Lifeline Is Not Profit

- Profit Is an Opinion Cash Is a Fact

- The 5 Cash Flow Metrics That Actually Matter

- Cash Flow Benchmarks for SaaS Agencies and E-commerce

- Warning Signs Your Cash Flow Is in Trouble

- Practical Strategies to Improve Cash Flow Now

- When DIY Finance Is Costing You More Than You Think

Your Business's True Lifeline Is Not Profit

A 2019 working paper by the Federal Reserve Bank of New York found that negative operating cash flow over a 12-month horizon was associated with a 2.5 to 4x higher probability of default than firms with positive operating cash flow, as summarized in NetSuite's cash flow management analysis. That's the number founders should remember.

If you're running a high-growth SaaS company or agency, this matters more than your net margin screenshot from last month. Payroll clears in cash. Rent gets paid in cash. Contractors, ad platforms, software vendors, tax payments, debt service, all cash. Your P&L doesn't fund any of that.

Founders often overfocus on topline growth and underfocus on timing. Timing is where businesses lose control. You close deals this month, invoice next month, collect the month after that, and pay your team every two weeks the whole time. That's how a "growing" company ends up boxed in.

Control starts with cash discipline

You don't need austerity. You need visibility and decisions.

A founder who understands cash flow makes sharper calls on hiring, payment terms, commission plans, annual billing, vendor negotiations, and financing. A founder who ignores it ends up reacting late, usually by cutting in a panic or raising capital from a weak position.

If you're looking for fast ways to preserve liquidity before it becomes a crisis, this guide on reducing startup expenses is worth reviewing. Cost control won't fix a broken model, but it buys time while you fix collections, pricing, and working capital.

Bottom line: Profit tells you whether your model can work. Cash flow tells you whether your business can keep operating long enough to benefit from that model.

If your team still debates gross margin while ignoring cash timing, fix that now. Start by understanding the gap between revenue metrics and actual operating economics, including the difference between gross profit versus operating profit.

Profit Is an Opinion Cash Is a Fact

Accrual accounting is useful. It is not the same thing as cash reality.

The statement of cash flows is used to assess liquidity and your ability to pay debts, fund daily operations, and invest in growth. It separates operating, investing, and financing cash movement so you can see where cash is generated and where it is consumed, as explained by Visual Lease's overview of the statement of cash flows. That's why a company can report profit and still struggle to cover payroll, rent, or supplier payments.

A worked example of a profitable agency with a cash problem

Assume your agency posts this monthly P&L:

- Revenue: $200,000

- Payroll and contractors: $120,000

- Software and overhead: $40,000

- Depreciation: $5,000

- Net income: $35,000

Looks fine. But now look at cash movement in the same month:

- Customers paid only $120,000 this month

- Accounts receivable increased by $70,000

- You bought $15,000 in equipment

- You paid down $10,000 of debt principal

Now your actual cash picture is:

- Start with net income of $35,000

- Add back $5,000 depreciation because it isn't cash

- Subtract $70,000 increase in receivables

- Subtract $15,000 equipment purchase

- Subtract $10,000 debt principal payment

Net cash change: negative $55,000

That is the founder punchline. You made accounting profit and lost cash.

Profit vs. cash A Tale of Two Statements

| Metric | Profit & Loss Statement | Cash Flow Statement |

|---|---|---|

| Revenue recognition | Records revenue when earned | Shows cash only when collected |

| Expenses | Includes non-cash items like depreciation | Focuses on actual cash paid |

| Main question answered | "Were we profitable?" | "Did cash increase or decrease?" |

| Best use | Margin analysis and trend tracking | Liquidity, solvency, and timing decisions |

| Founder risk if used alone | False confidence | Much lower |

A healthy P&L with weak collections is how founders talk themselves into a cash crunch.

This is why billing structure matters so much. In e-commerce and DTC, some brands use a negative cash conversion cycle to self-fund DTC store growth. In agencies and services, the opposite often happens. You staff the work now and wait to get paid later.

If this still feels fuzzy, your team probably needs a cleaner grasp of what is accrual accounting. Once you understand that difference, the cash flow statement stops looking optional.

The 5 Cash Flow Metrics That Actually Matter

The fix for cash flow isn't "watch the bank balance more closely." You need a small dashboard with metrics that show both current position and near-term risk.

Use one operating example

Use this sample business for all five calculations:

- Cash collected this month: $180,000

- Cash operating expenses this month: $150,000

- Capital expenditures: $12,000

- Beginning cash balance: $240,000

- Ending cash balance: $258,000

- Monthly recurring debt service: $20,000

- Credit sales for the month: $210,000

- Ending accounts receivable: $105,000

- Inventory purchased: $30,000

- Ending inventory tied to the period: $20,000

- Accounts payable tied to operating purchases: $25,000

A good explainer on the core concept sits here: what is operating cash flow.

The five metrics

1. Operating cash flow

Operating cash flow tells you whether the core business generates cash before financing and investing decisions.

Simple founder version:

Cash collected from customers - cash paid for operations = operating cash flow

Using the example:

$180,000 - $150,000 = $30,000 operating cash flow

If this number is negative month after month, your growth isn't funding itself. Your balance sheet or outside capital is carrying the business.

2. Burn rate

Burn rate matters most when operating cash flow is negative or volatile.

Simple version:

Cash outflows - cash inflows = net burn

If next month you collect $140,000 and spend $170,000, your net burn is $30,000. That's the amount of cash your business consumes in the month.

For growth companies, burn isn't automatically bad. Undisciplined burn is bad.

Practical rule: If you can't explain exactly what's driving burn by customer acquisition, hiring, or product investment, it isn't strategic burn. It's drift.

Here is a quick visual recap before the next three metrics:

3. Cash runway

Runway answers the only question that matters during pressure: how long until you run out of options?

Formula:

Current cash balance / monthly net burn

Using the example burn of $30,000 and ending cash of $258,000:

$258,000 / $30,000 = 8.6 months of runway

That means you don't have "time." You have a finite number of monthly decisions left.

4. Days sales outstanding

DSO measures how fast you collect from customers.

Formula:

Accounts receivable / credit sales × days in period

Using a 30-day month:

$105,000 / $210,000 × 30 = 15 days

That is healthy. If your DSO starts creeping up, your sales team, billing process, or client quality is changing.

5. Cash conversion cycle

Cash conversion cycle measures how long cash stays trapped between spending and collection.

Founder formula:

Days inventory outstanding + DSO - days payable outstanding

Using a simple worked example:

- DIO = 20 days

- DSO = 15 days

- DPO = 25 days

So:

20 + 15 - 25 = 10-day cash conversion cycle

Shorter is better. Negative can be excellent if it comes from strong billing and supplier power, not from starving operations.

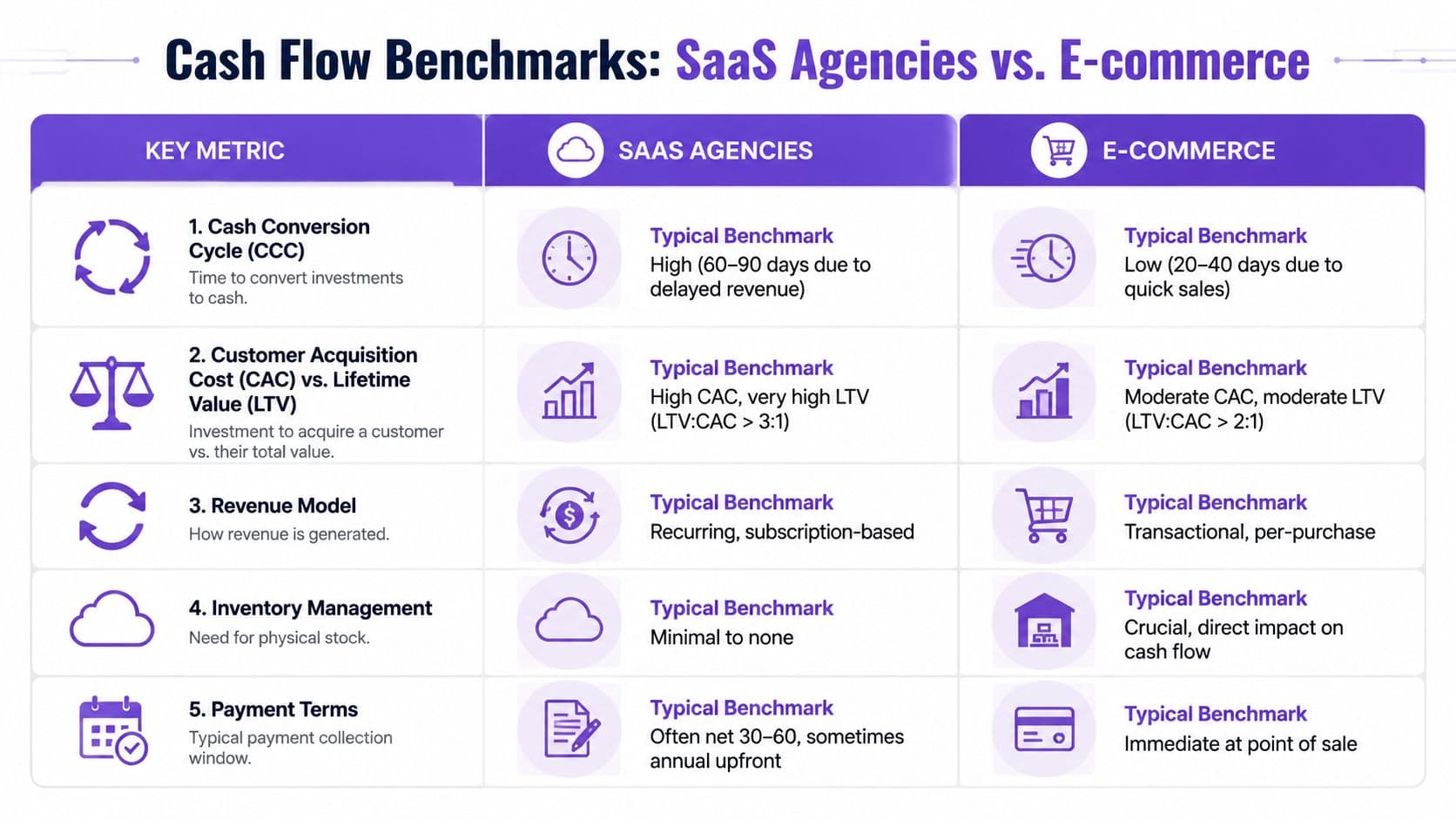

Cash Flow Benchmarks for SaaS Agencies and E-commerce

A company with clean earnings but weak cash conversion gets a worse multiple, weaker debt options, and less control. Founders who treat cash flow as a valuation driver make better pricing, billing, inventory, and hiring decisions earlier.

Use these thresholds to judge whether your cash engine is helping or hurting enterprise value:

- Operating cash flow to net income ratio: 0.8 to 1.0 is strong. 0.4 to 0.6 means reported profit is not turning into usable cash fast enough.

- Debt service coverage: 1.5x to 2.0x annual operating cash flow is the floor if you want lender confidence and room for error.

- 13-week cash forecast: model a 20 to 30% revenue drop and a 45 to 60-day sales cycle slowdown. If the business breaks under that pressure, your cash model is weak.

- Collection speed, prepaid cash, and working capital discipline matter more than margin percentage alone in all three models.

SaaS cash flow is built in pricing and billing

SaaS cash flow starts with contract structure. A company at $2 million ARR can still feel broke if it bills monthly, takes 45 days to launch, and lets enterprise invoices age.

Push annual prepay where the market supports it. Invoice implementation at signature. Shorten time-to-go-live. Those choices improve cash before you cut spend.

For SaaS, the benchmark table is simple:

| Lever | Strong | Weak |

|---|---|---|

| Billing cadence | Annual upfront or shorter collection lag | Monthly billing with slow collection |

| Deferred revenue | Healthy prepaid balance that funds growth | Little prepaid cash support |

| OCF to net income | 0.8 to 1.0 | 0.4 to 0.6 |

| Debt coverage | Above 1.5x | Near 1.0x |

A buyer or lender reads this as control. If customers pay you before you deliver the full service period, your growth needs less outside capital.

Agencies win on invoicing speed and contract discipline

Agencies rarely die because revenue disappears overnight. They run into cash trouble because payroll is biweekly and clients pay whenever they feel like it.

If your average client pays in 55 days and your team gets paid every 14, you are financing delivery out of your own bank account. That destroys flexibility. It also lowers the quality of earnings because revenue looks fine while cash trails behind.

Set a standard: upfront retainers, milestone billing, change-order approval before extra work, and one owner for collections. If you need a broader breakdown of the red flags, review these common cash flow problems in small businesses. Agency versions usually show up as overdue receivables, underbilled scope, and rushed draws on a credit line.

E-commerce cash flow lives or dies in inventory turns

E-commerce collects cash fast. That is the good news. The bad news is that inventory, returns, and ad spend can absorb cash long before the P&L makes the damage obvious.

The benchmark that matters here is not just gross margin. It is how quickly inventory converts back into cash and how much of that cash gets trapped in slow-moving SKUs. If you overbuy by even one purchase cycle, you can post profitable months while starving operations.

The operating focus is different by model:

- SaaS: cash improves through billing design, prepayment, and faster onboarding

- Agency: cash improves through tighter terms, invoicing discipline, and collections ownership

- E-commerce: cash improves through inventory turns, reorder accuracy, and supplier terms

Here is the founder-level rule. If revenue growth requires more cash than your model can self-fund, your valuation story gets weaker, not stronger.

Warning Signs Your Cash Flow Is in Trouble

Cash flow problems usually announce themselves early. Founders just ignore the signals because revenue still looks good.

Here are the red flags I take seriously:

- Bank balance keeps shrinking while sales rise. That's the classic sign of working capital strain.

- You miss forecasted cash targets repeatedly. Your model is weak, your assumptions are weak, or both.

- Receivables age upward month after month. Sales quality, invoicing discipline, or customer fit is deteriorating.

- You rely on a credit line to cover normal operations. Debt should support timing and strategy, not routine survival.

- Vendors get paid later and later. You are preserving cash by transferring stress to suppliers.

- The gap between net income and cash widens. Your earnings quality is getting worse.

- Founders delay hiring, tax payments, or owner distributions because “cash is tight”. The issue has already moved from finance into operating decisions.

What these signals usually mean

These symptoms don't all point to the same problem.

A rising DSO points to collections and client quality. A falling bank balance with stable DSO often points to margin compression, inventory buildup, capex, or debt service pressure. Increased line-of-credit dependence usually means your operating model hasn't caught up with your growth plan.

If these issues sound familiar, review a practical breakdown of cash flow problems in small business. Then answer one question immediately: is this a timing issue, a pricing issue, or a structural margin issue? If you can't answer that fast, you don't have enough reporting discipline.

Practical Strategies to Improve Cash Flow Now

Cash flow improves when you change process, terms, and behavior. Not when you ask the team to "be more careful."

A peer-reviewed study found that reductions in cash flow management inefficiencies were associated with higher firm performance, with approximate improvements of 6.8%, 0.03%, and 7.2% for specific cash flow measures when those measures declined by one unit, according to the NIH-hosted study on cash flow management and firm performance. That matters because disciplined cash management improves outcomes, not just survival odds.

Speed up inflows

Start with receivables because it's the fastest lever.

- Invoice immediately after delivery, milestone completion, or contract trigger.

- Shorten payment friction by using ACH, card-on-file, or automated reminders through tools like Stripe, QuickBooks, or Xero.

- Assign collections ownership to a named person, not "the finance team."

- Change contract terms for new deals. Deposits, retainers, annual prepay options, and milestone billing all improve timing.

Slow down outflows without damaging operations

Don't slash blindly. Sequence cash.

| Move | What to do |

|---|---|

| Vendor terms | Ask for longer terms where you have purchase history and reliability |

| Spend approvals | Require signoff for non-essential software, contractors, and discretionary marketing |

| Large purchases | Time equipment, tooling, or major implementations around real cash generation |

| Debt review | Revisit principal schedules and covenant pressure before they force the conversation |

A company with decent margins and poor payment timing can often fix cash faster than a company with weak margins and perfect bookkeeping.

Fix the operating engine

At this stage, lasting improvement occurs.

- For SaaS: tighten implementation, reduce billing delays, and push annual plans when the product supports it.

- For agencies: invoice for scope changes fast, stop carrying unapproved work, and use deposits on high-labor projects.

- For e-commerce: buy inventory with discipline, clear slow-moving stock, and line up purchasing with actual sell-through.

If you need a more detailed operating playbook, this guide on how to improve cash flow is a useful next step.

One practical option for companies that need tighter reporting is an outsourced controller setup. Firms like Jumpstart Partners can handle cash forecasting, month-end close, and reporting cadence so leadership can make faster decisions with cleaner numbers.

When DIY Finance Is Costing You More Than You Think

At a certain stage, DIY finance becomes expensive.

If you're doing between $500K and $20M in revenue and still managing cash with a bank balance, a basic bookkeeper, and a spreadsheet someone updates when things feel urgent, you're underpowered. The problem isn't effort. The problem is decision quality.

Cash flow management for a SaaS company, agency, or e-commerce brand requires more than reconciled books. You need monthly financials you trust, a rolling cash forecast, clarity on receivables and payables, and someone who can translate those numbers into operating decisions. Otherwise, you'll keep solving the wrong problem. You'll cut marketing when collections are the issue. You'll delay hiring when pricing is the issue. You'll raise capital when billing design is the issue.

This is also where spending discipline gets more specific. For example, software and infrastructure costs often expand, creeping up as teams grow. A resource on practical IT budget optimization can help uncover waste without cutting tools your team needs.

The founder-level question isn't whether finance is "handled." It's whether finance is helping you control the business.

If you want cleaner cash visibility, tighter monthly reporting, and a finance function built for growth-stage SaaS, agencies, or e-commerce, talk to Jumpstart Partners. A good controller setup won't just tell you where cash went. It will help you decide what to do next.