Financial Operations

ISO vs NQ Stock Options: A Founder's Guide

Deciding between ISO vs NQ stock options? This guide details the tax, accounting (ASC 718), and strategic differences to help founders make the right choice.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··21 min readThe biggest mistake founders make in the ISO vs NQSO decision is treating it like an employee tax perk decision. It isn't. It's an operating model decision.

Choose the wrong structure and you don't just create surprise taxes for employees. You create payroll withholding issues, messy ASC 718 expense tracking, cap table errors, and due diligence friction right when you're trying to raise money. That damage shows up in your close process, your board reporting, and your valuation story. If you're already thinking about post-money valuation, you should treat your option plan with the same seriousness. Investors do.

Founders usually want a simple answer. Here it is. Use ISOs selectively for U.S. employees when the tax advantage is worth the complexity. Use NQSOs everywhere flexibility and operational control matter more. That means advisors, consultants, directors, many late-stage grants, and any situation where you don't want your team walking into AMT surprises or your finance function chasing preventable compliance work.

Table of Contents

- Choosing Your Equity Playbook ISO vs NQSO

- ISO vs NQSO The Fundamental Tax and Structural Rules

- A Tale of Two Tax Scenarios ISO vs NQSO Calculations

- The Company's Burden ASC 718 Accounting and Reporting

- When to Grant ISOs vs NQSOs A Founder's Decision Framework

- Equity Plan Red Flags Common Mistakes to Avoid

- Your Audit-Ready Equity Plan Checklist

Choosing Your Equity Playbook ISO vs NQSO

If your company is between early traction and institutional diligence, the ISO vs NQSO choice affects more than compensation. It affects whether your equity plan scales cleanly or turns into a recurring finance cleanup project.

My view is simple: most founders should start from operational reality, not tax theory. ISOs sound better because they can be more tax-efficient for employees. But they come with rigid rules, tracking requirements, and AMT exposure that many teams underestimate. NQSOs are less glamorous and far more forgiving. In practice, that makes them the default workhorse for a lot of growing companies.

That doesn't mean ISOs are a bad idea. It means they should be used intentionally. If you're granting equity to core U.S. employees and you want a retention tool with potentially favorable tax treatment, ISOs are often the right move. If you're compensating anyone outside that lane, NQSOs win immediately because they're the only practical option.

Practical rule: If your finance team can't explain the tax event, the reporting requirement, and the cap table impact of a grant in one meeting, your plan is too complicated for your current operating stage.

Three questions should drive your decision:

- Who is receiving the grant: Employees can receive either structure. Non-employees push you to NQSOs.

- How much admin complexity can you absorb: ISOs demand tighter tracking and cleaner processes.

- What story do you need your books to tell: If you're preparing for a raise, sloppy stock comp accounting creates avoidable diligence issues.

Founders often ask which plan is “better.” Wrong question. The right question is which plan creates the least friction while still delivering the incentive you want. That answer usually leads to a mixed program, not a one-size-fits-all plan.

ISO vs NQSO The Fundamental Tax and Structural Rules

Pick the wrong option type and you do not just create an employee tax problem. You create a finance, legal, and audit problem for the company.

The rule that decides eligibility

Start with the hard boundary. ISOs can only go to employees. NQSOs can go to employees, directors, consultants, and advisors, according to Greenbush Financial's overview of stock option rules. That one rule drives plan design, grant paperwork, and cap table administration.

ISOs also come with statutory limits that create real operating work for the company. No more than $100,000 of ISO value can first become exercisable in a calendar year. ISOs generally must be exercised within 10 years of grant. For holders who own more than 10% of the company, the strike price must be at least 110% of fair market value and the exercise period drops to 5 years, as Greenbush notes.

Miss any of that and you are not running a clean ISO program. You are creating grants that may need to be reclassified, explained to auditors, and cleaned up during diligence.

Here is the practical comparison:

| Attribute | Incentive Stock Options (ISOs) | Non-Qualified Stock Options (NQSOs) |

|---|---|---|

| Eligible recipients | Employees only | Employees, directors, consultants, advisors |

| Tax at exercise | Usually no regular tax at exercise, but AMT may apply | Usually taxed at exercise on the spread as ordinary income |

| Tax at sale | Can receive favorable treatment if holding rules are met | Gain after exercise may be capital gain, but exercise spread is already ordinary income |

| Holding requirements | More than 1 year after exercise and more than 2 years after grant for favorable treatment | No ISO-style qualifying holding requirement |

| Annual cap | $100,000 of value can first become exercisable in a calendar year | No comparable statutory cap |

| Maximum term | Generally 10 years from grant | No comparable ISO statutory term in the verified data |

| Special rule for over 10% holders | Strike price at least 110% of FMV and term limited to 5 years | No comparable rule in the verified data |

The structural rules that hit finance and operations

Founders usually focus on employee tax treatment first. Finance teams should focus on administration first.

ISOs require tighter controls because the company has to track grant dates, exercise dates, post-termination exercise windows, qualifying versus disqualifying dispositions, and the $100,000 annual vesting limit across grants. If your cap table system and stock administration process are loose, ISO compliance breaks fast.

NQSOs are simpler to operate. They still require board approval, a defensible fair market value, clean grant documentation, and ASC 718 expense recognition. But they do not carry the same statutory eligibility rules or ISO holding-period monitoring. That simplicity matters when your team is small and your close process is already stretched.

The employee tax timing still matters. NQSOs usually create ordinary income at exercise on the spread between strike price and fair market value. ISOs can avoid regular tax at exercise if the requirements are met, but the spread can still create AMT exposure. If your employees need help estimating that exposure, point them to this guide on how to calculate alternative minimum tax for ISO exercises.

What this means for your books

Under ASC 718, both ISOs and NQSOs create stock-based compensation expense based on grant-date fair value. The accounting problem is not whether one type escapes expense. It does not. The primary issue is whether your records are clean enough to support the valuation inputs, vesting schedules, modifications, cancellations, and exercises.

ISOs add another layer of audit risk because the tax status depends on facts the company has to track correctly. NQSOs usually create fewer edge cases. That is one reason I tell founders to keep ISOs narrow and intentional. Use them for core U.S. employees when the retention story is strong. Use NQSOs everywhere else and keep the plan easier to administer, easier to explain, and easier to defend in diligence.

If you expect an audit, a financing, or an acquisition process in the next 12 to 24 months, operational simplicity wins more often than theoretical tax upside.

A Tale of Two Tax Scenarios ISO vs NQSO Calculations

The label on the option grant matters less than the cash and admin burden it creates later. A founder who ignores the math usually pays for it twice. First through confused employees, then through messy records, payroll fixes, and diligence questions.

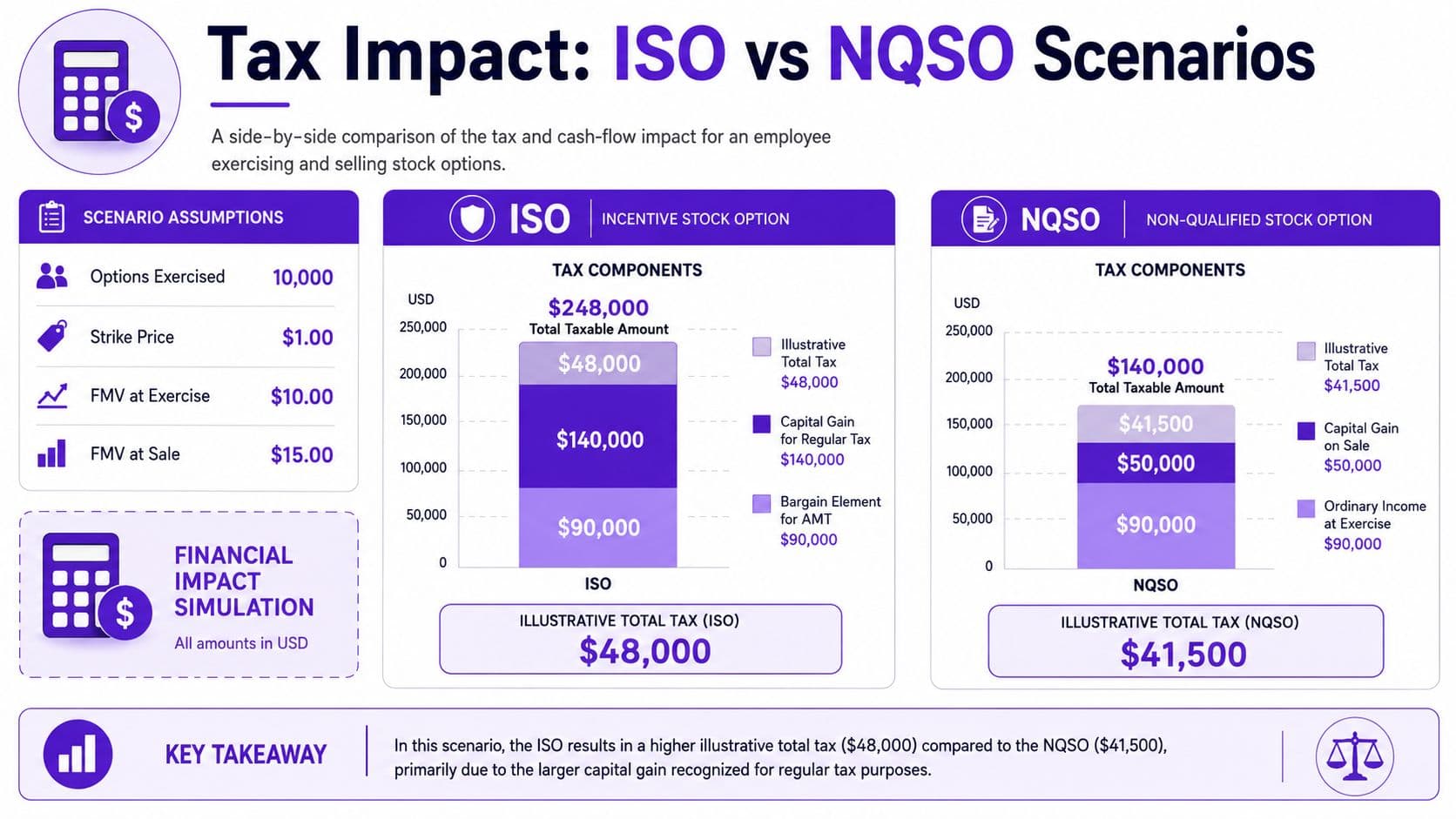

Worked example using the provided numbers

Use a simple case:

- 10,000 options exercised

- Strike price: $1.00

- FMV at exercise: $10.00

- FMV at sale: $15.00

Start with the two numbers that drive everything.

- Exercise cost = 10,000 × $1.00 = $10,000

- Spread at exercise = ($10.00 - $1.00) × 10,000 = $90,000

For NQSO, that $90,000 spread is ordinary income at exercise. The employee owes tax before any sale proceeds show up. If your payroll process is sloppy, the company inherits the problem because withholding and reporting attach to that exercise event.

For ISO, the same $90,000 spread does not create regular taxable income at exercise if the rules are met, but it can create AMT exposure. That is the trap. Employees hear “better tax treatment” and skip the cash planning. If you want a practical walkthrough, send them this guide on how to calculate AMT on an ISO exercise.

Now look at the sale math.

- Total gain from strike to sale = ($15.00 - $1.00) × 10,000 = $140,000

- Gain after exercise value = ($15.00 - $10.00) × 10,000 = $50,000

The infographic's example summarizes the outcomes this way:

| Scenario | Key tax component | Amount |

|---|---|---|

| ISO | Bargain element for AMT | $90,000 |

| ISO | Capital gain for regular tax | $140,000 |

| ISO | Illustrative total tax | $48,000 |

| NQSO | Ordinary income at exercise | $90,000 |

| NQSO | Capital gain on sale | $50,000 |

| NQSO | Illustrative total tax | $41,500 |

The important point is operational, not theoretical. In this example, the ISO holder can face a larger near-term cash burden even though the option type is often pitched as the employee-friendly choice. Founders who promise tax efficiency without showing the exercise and sale timeline set up avoidable frustration.

A short explainer can help if you're walking your team through the distinction:

What the company should learn from Alex's exercise

This example is not just an employee tax story. It is a company operations story.

First, cap table accuracy has to survive the exercise event. If 10,000 options are exercised, your system needs the right grant ID, strike price, exercise date, share issuance, and post-exercise holdings. Get any of that wrong and your ASC 718 support becomes harder to defend.

Second, NQSO exercises hit payroll and tax reporting immediately. The spread creates compensation income. That means your finance team needs a clean handoff between the cap table, payroll provider, and general ledger. If that handoff fails, you get W-2 errors, withholding corrections, and audit comments.

Third, ISO exercises still create work even when payroll withholding is not triggered. You need records that show the grant qualified as an ISO, stayed within plan limits, and was exercised on the right terms. You also need a process for employee communications, 3921 reporting, and board-approved documentation that ties back to the option plan and grant files.

Here's my recommendation. Use examples like this in every grant package and exercise memo. Show the employee the $10,000 exercise cost, the $90,000 spread, and the different tax timing by option type. Then make sure your finance team can book the event, update the cap table, and support the paperwork without rebuilding the file during diligence.

That is how you keep an equity plan fundable, auditable, and usable.

The Company's Burden ASC 718 Accounting and Reporting

Stock options do not stay in the legal folder. They hit your P&L, your cap table, your payroll process, and your audit file.

That is why founders get burned here. They treat ISOs vs NQSOs as an employee tax choice, then discover the true cost shows up in finance operations.

Under ASC 718, every option grant needs a defensible grant date, a supportable fair value method, a clear vesting schedule, and a monthly expense schedule that ties to the general ledger. If any of those pieces are weak, your auditors push back, your diligence requests get longer, and your finance team wastes time rebuilding records you should have had from the start.

The option type changes the workflow. NQSOs usually create payroll coordination and tax withholding at exercise. ISOs usually create more compliance tracking around qualification, holding periods, and Form 3921 reporting. Both still require disciplined stock compensation accounting.

Where companies actually break

The failure points are operational, not theoretical.

A board approves grants after the stated grant date. The 409A support does not line up with the strike price used in the grant notice. The cap table says one thing, payroll says another, and the GL says something else. Then a financing or audit starts, and your team has to explain why the equity records do not reconcile.

Investors notice this fast. Auditors notice it faster.

If your equity process is loose, option grants can also expose governance gaps in the underlying company setup. Even basic formation records and approvals should be consistent with your plan documents, board consents, and the company's business operating agreement.

What ASC 718 demands from finance

Use a repeatable process every month, not a quarter-end rescue project.

-

Lock down grant documentation

Board consent, option agreement, strike price support, and grant date must match. If they do not, grant-date accounting gets harder to defend. -

Book stock comp expense monthly

Do not wait until the audit. Monthly entries keep the P&L credible and expose errors while they are still easy to fix. -

Reconcile the cap table to the GL

Grants, forfeitures, modifications, and exercises should tie across Carta, Pulley, Shareworks, QuickBooks, Xero, or NetSuite. If they do not tie, you have a control issue, not just a bookkeeping issue. -

Build separate workflows for ISO and NQSO exercises

NQSO exercises need payroll and tax reporting coordination. ISO exercises need qualification checks, clean exercise records, and Form 3921 support. -

Treat modifications as accounting events

Extended post-termination exercise windows, repricing, and changed vesting terms can trigger incremental expense. Legal may draft the change, but finance owns the accounting result.

My recommendation

Keep your ISO program narrow unless you can administer it properly. If your finance stack is thin, your close process is inconsistent, or your cap table history is messy, broad ISO grants create more risk than value for the company. NQSOs are often easier to operate because the tax treatment is more straightforward and the exceptions are fewer.

The standard is simple. Your equity records should be audit-ready at any point in the year, not only after a cleanup sprint. If you need a benchmark, use the same discipline described in these financial reporting best practices for growing companies.

A clean option plan helps recruiting. A clean option process helps fundraising. Founders should care more about the second one.

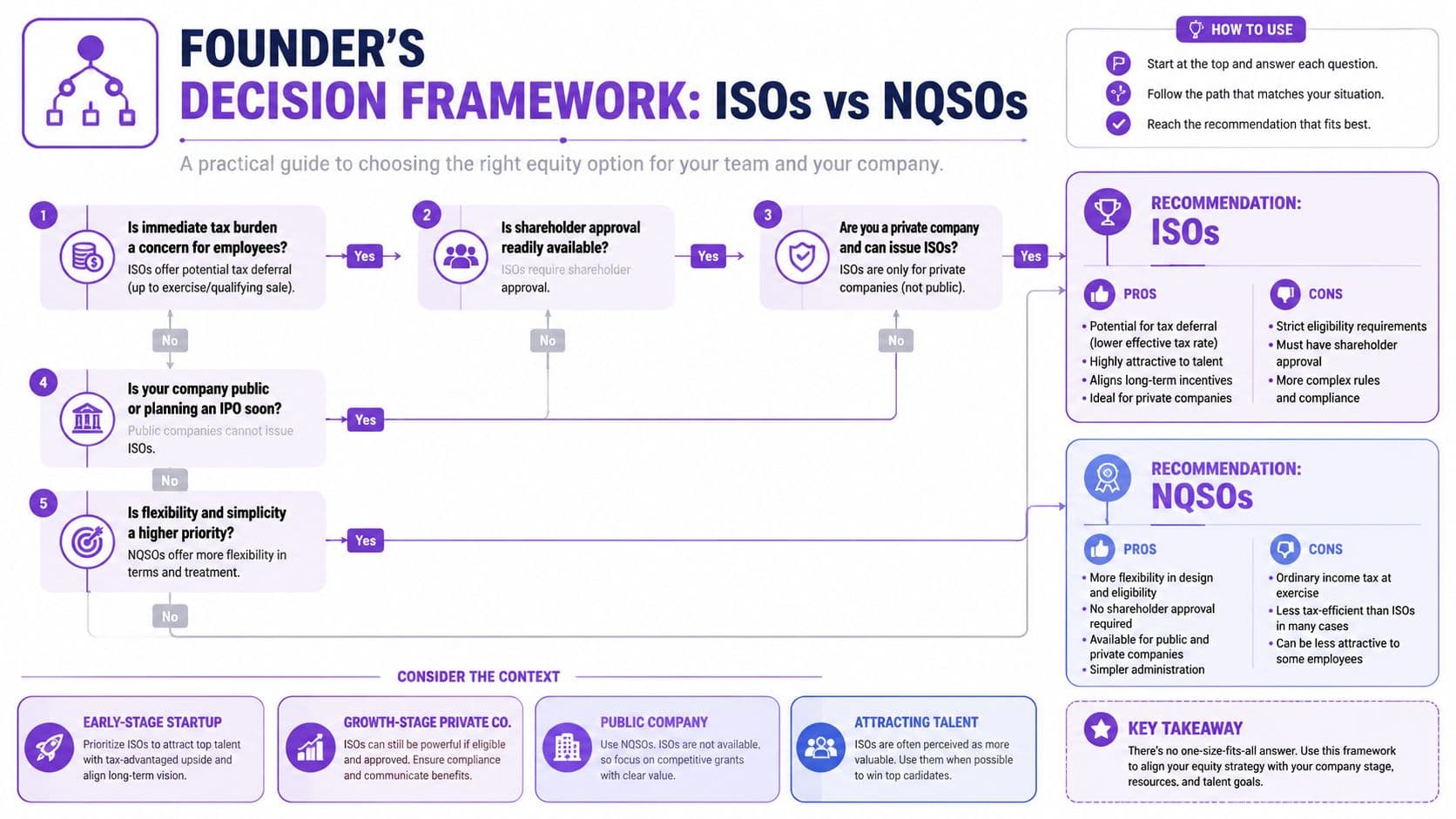

When to Grant ISOs vs NQSOs A Founder's Decision Framework

Founders usually overgrant ISOs. That decision creates more operational drag than recruiting value. Use ISOs for a tight group of U.S. employees where the tax benefit is real and your team can support the admin. Use NQSOs as the default everywhere else.

The founder question is not “Which option type sounds better to candidates?” Rather, the question is “Which option type can we grant, track, expense, exercise, and defend during diligence without creating cleanup work?” That is the right standard if you care about audit readiness, board reporting, and a financing process that does not stall over equity records.

My default recommendation by recipient type

| Recipient or situation | My recommendation | Why |

|---|---|---|

| Core U.S. employees with meaningful upside | ISO, selectively | Better employee tax treatment can be worth it if you can track eligibility, limits, and post-termination rules correctly |

| Early hires receiving standard grants | NQSO unless there is a clear reason for ISO | Lower admin burden and fewer qualification traps |

| Advisors | NQSO | ISOs are not available |

| Consultants and contractors | NQSO | ISOs are not available |

| Directors | NQSO | ISOs are not available |

| Large grants that may push past ISO limits | NQSO or split grant | Cleaner cap table administration and fewer reclassification problems |

| International team members | NQSO or local-country alternative | ISO rules do not solve cross-border payroll, tax, or compliance issues |

Orrick's startup FAQ on ISOs and NSOs lays out the hard boundaries. ISOs are limited to employees, and the annual exercisability cap forces you to monitor grant sizing by individual. That sounds manageable until you have promotions, refresh grants, early exercises, or a rushed hiring plan before a fundraise.

Governance matters too. If your board approvals, plan documents, and delegation rules are loose, option type is not your first problem. Fix authority first. A practical primer on a business operating agreement is useful if you are tightening approval rights and ownership rules before financing or expanding grants beyond the founding team.

Choose ISOs only when the company can carry the weight

Grant ISOs when all four conditions are true:

- The recipient is a U.S. employee and likely to stay long enough for the grant to matter

- You can monitor ISO eligibility, the annual limit, and termination-driven status changes

- Finance can support Form 3921 reporting and maintain clean exercise records

- You are willing to educate employees on AMT risk and holding period rules

If any one of those breaks, the company pays for it later. You get exceptions, manual workarounds, confused employees, and diligence questions that land on finance instead of legal.

Choose NQSOs when operational clarity matters more

NQSOs are the better plan design in these situations:

- You grant equity across employees, advisors, directors, and contractors

- You expect frequent custom grants, refresh grants, or off-cycle approvals

- Your finance team is small and your monthly close still depends on manual reconciliations

- You want fewer plan-level exceptions flowing into ASC 718 schedules, payroll coordination, and audit support

This is the part founders miss. The employee tax story gets attention. The company workflow determines whether the plan holds up. NQSO exercises push income into payroll and withholding, which is administratively clearer. ISO programs avoid some employee tax at exercise, but they add qualification rules, disqualifying disposition tracking, and more opportunities for your records to drift from reality.

My operating rule

For companies between seed and late growth, a hybrid plan is usually the right answer. Keep ISOs limited to employees you are deliberately trying to retain, and standardize NQSOs for everyone else. That approach reduces cap table sprawl, keeps ASC 718 assumptions cleaner, and makes board-approved grant administration easier to defend.

Use a system built for equity administration, not a spreadsheet with custom tabs and old formulas. Good capitalization table software gives finance one source of truth for grants, exercises, cancellations, and modifications. That matters more than the theoretical tax edge of an ISO grant you cannot administer cleanly.

My recommendation is simple. Pick the plan your company can operate accurately every month, not the plan that looks best in an offer letter.

Equity Plan Red Flags Common Mistakes to Avoid

A weak option plan usually doesn't fail all at once. It fails during diligence, during an audit, or when a departing employee asks a question nobody can answer.

Red flags in plan design

The first red flag is a strike price that isn't tied to a defensible fair market value process. If your board minutes, valuation support, and grant paperwork don't align, you're inviting tax and accounting issues.

The second is pretending everything can be an ISO. It can't. Eligibility rules and statutory limits are hard boundaries. If you grant without mapping recipient type and exercisability, you'll end up with grants that don't match your intent.

Another red flag is overengineering the plan before your team can administer it. Multiple custom vesting schedules, side letters, extended windows, and ad hoc advisor grants all sound manageable. Then your controller tries to close the books and discovers three conflicting data sources.

A plan isn't sophisticated because it has edge cases. It's sophisticated when your company can administer it cleanly.

Red flags in administration

Operational mistakes create just as much damage as legal mistakes.

- Missing exercise tracking: If finance, payroll, and legal don't reconcile exercise activity, your records won't support tax reporting or ASC 718 entries.

- No ISO reporting calendar: Form 3921 requirements are easy to miss when option administration is fragmented.

- Poor employee communication: Employees who don't understand exercise consequences make bad timing decisions and escalate avoidable frustration to leadership.

- Cap table drift: If your cap table system and general ledger don't tie, every financing and audit gets harder.

- Manual dependency on one person: If only one operator understands the plan, you don't have a process. You have key-person risk.

The corrective action is boring and effective. Centralize approvals, maintain one source of truth for grants and exercises, and review equity admin during every monthly close. Founders skip that because it feels administrative. Investors and auditors don't.

Your Audit-Ready Equity Plan Checklist

An audit-ready equity plan is not a legal binder on a shelf. It's a repeatable operating process.

What to lock down now

Use this checklist and assign an owner to each item.

- Maintain one authoritative cap table: Carta, Pulley, Shareworks, or your chosen platform should match board approvals and finance records.

- Store complete grant files: Board consent, grant notice, vesting terms, exercise records, and any modifications belong in one controlled repository.

- Run monthly stock comp accounting: Don't defer ASC 718 entries until quarter-end.

- Create a tax event calendar: Exercises, withholding steps, and ISO reporting deadlines should live on the same compliance calendar as payroll and sales tax.

- Train employees before exercise: A short exercise memo beats a long apology later.

What to hand your controller this month

Give your finance lead a simple action list:

| Task | Why it matters |

|---|---|

| Reconcile cap table to GL | Prevent diligence disputes |

| Review open grants and vesting | Catch errors before close |

| Confirm exercise activity by type | Support tax reporting and journal entries |

| Check documentation for modified awards | Avoid accounting surprises |

| Prepare an audit folder | Save time when diligence starts |

If you're preparing for diligence, align this work with your broader audit preparation process. Equity records are one of the first places outside reviewers test whether your finance function is disciplined or improvised.

The bottom line on iso vs nq stock options is clear. Choose ISOs when you have a specific employee retention objective and the infrastructure to support them. Choose NQSOs when flexibility, cleaner administration, and broader eligibility matter more. Most growing companies need both, but they need them administered like a system, not handed out like favors.

If your equity plan is creating questions around ASC 718, cap table accuracy, exercise reporting, or fundraising readiness, Jumpstart Partners can help you clean up the process, tighten the books, and get your finance function ready for diligence.