Financial Operations

Post Money Valuation: A Founder's Guide to Equity & Dilution

Master post money valuation to secure fair terms. This guide explains formulas, cap tables, dilution, and how to model SAFEs and notes for your SaaS or agency.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··18 min readYou’ve got a term sheet in your inbox. The valuation looks great. You feel validated, and you should.

Then you need to slow down and ask the only question that matters: what will you own after this round closes?

That’s where founders get trapped. They fixate on the headline number and ignore the mechanics underneath it. Post money valuation is the number that decides investor ownership, founder dilution, and how much control you still have when the board starts making real demands.

If you run a SaaS company, digital agency, or professional services firm, this isn’t abstract venture math. It affects your hiring plan, your option pool, your next round, and your negotiating power in every discussion that follows.

Your Term Sheet Is In But What Does It Actually Mean

A founder I advise will often call with the same reaction: “We got the valuation we wanted.”

That’s usually the wrong starting point.

The better question is, “What does this deal do to my cap table?” If you raise capital without understanding post money valuation, you’re negotiating with half the information. You may think you sold one slice of the company, then discover you also gave up more through SAFE conversions, an expanded option pool, or poorly modeled dilution.

The headline number doesn't protect you

A big pre-money valuation feels like a win because it signals progress. Investors know that. They also know founders often pay less attention to how ownership gets calculated after the investment lands.

If you accept terms based on optics instead of ownership math, you can quickly lose influence. You’ll feel it when you need board approval, when you want to recruit executives, or when the next round forces you to explain why your ownership dropped faster than expected.

Practical rule: Don’t review a term sheet as a fundraising document. Review it as an ownership transfer document.

Control gets lost one clause at a time

Most founders don’t give up control in one dramatic move. They give it up in pieces.

That usually happens through:

- Unmodeled dilution: You focus on the round size and ignore what converts at closing.

- Option pool timing: You accept a pool increase that lands on your side of the ledger.

- Messy financials: Investors use uncertainty to push terms in their favor.

- Weak diligence prep: You react to investor questions instead of controlling the process.

If you’re still getting your finance stack organized, start with a solid financial due diligence checklist. You need your numbers clean before you negotiate valuation, not after.

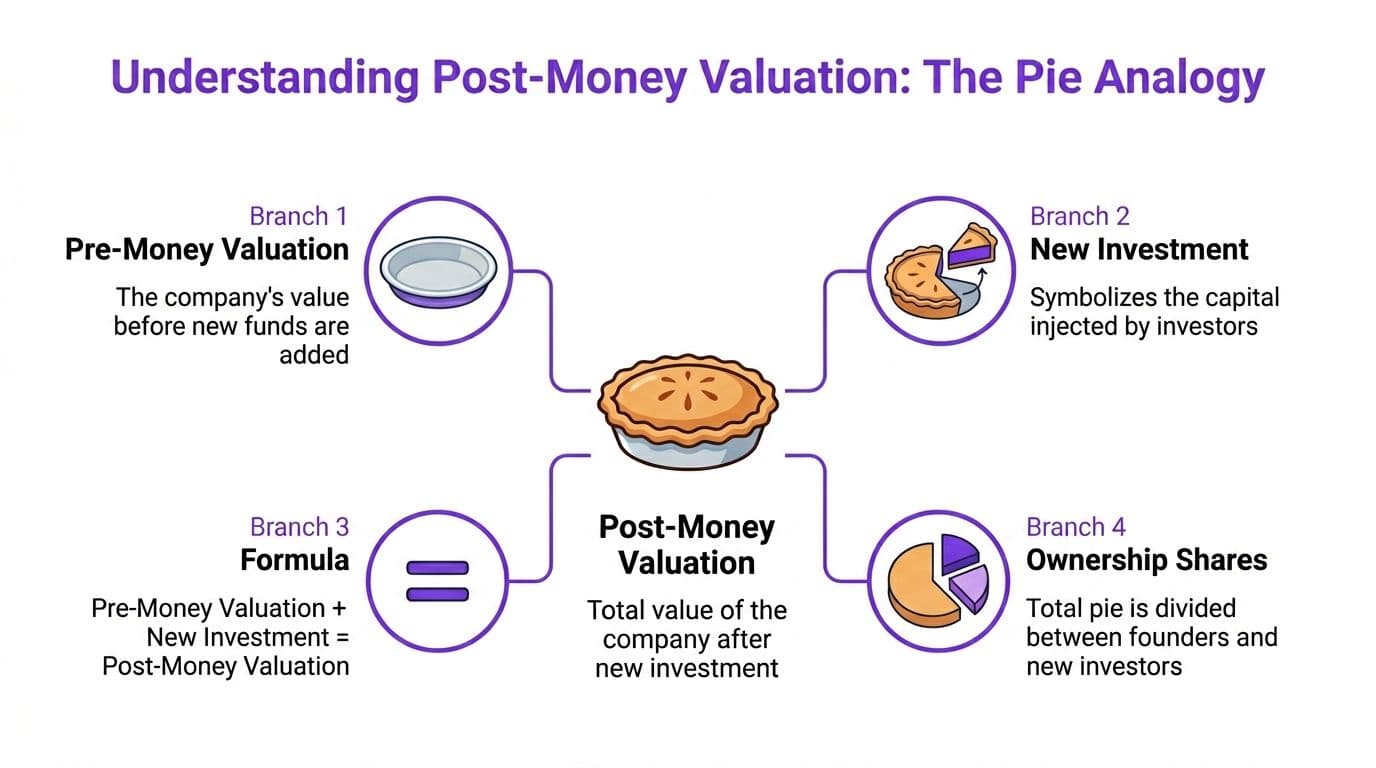

What Is Post-Money Valuation And Why It's Not Just a Number

Post money valuation is simple at the surface and dangerous in practice if you oversimplify it.

At its most basic, post money valuation = pre-money valuation + new investment. That tells you what the company is worth immediately after the investor’s cash goes in.

Think of your company like a pie. Before the round, the pie is your pre-money valuation. The investor adds capital, which makes the full pie larger. Then ownership gets divided based on that larger pie, not the old one.

The formula every founder must know

Here’s the foundational example from Wikipedia’s explanation of post-money valuation:

- Pre-money valuation: $100 million

- New investment: $25 million

- Post money valuation: $125 million

- Investor ownership: 20% because $25M / $125M = 20%

That’s clean and useful. It shows why the post money number matters more than the vanity of the pre-money number. Ownership is set against the post money figure.

Here’s another plain-English example for a smaller growth company:

| Item | Amount |

|---|---|

| Pre-money valuation | $25 million |

| New investment | $5 million |

| Post money valuation | $30 million |

| Investor ownership | 16.67% |

In that case, the investor owns 16.67% because $5M divided by $30M equals 16.67%.

Why investors care about post money first

Investors don’t look at valuation the way founders do. Founders often treat it as a signal. Investors treat it as a pricing mechanism for ownership.

“You know exactly how much of your company you are selling.”

That’s the practical advantage of a post-money framework. It forces clarity on what the check buys.

If you’re building your own framework for pricing and negotiation, a deeper look at the valuation of startup companies will help you tie valuation to fundamentals instead of wishful thinking.

The basic formula is not the whole story

The clean formula works for simple priced rounds. It stops being enough when your cap table includes:

- Convertible notes

- SAFEs

- Options

- Warrants

- Pool expansions

That’s why fully diluted post money valuation matters. Once all potential shares are counted, your true ownership often looks worse than the headline term sheet implied.

Wikipedia’s more complex example shows this clearly. In that scenario, shares issued from a new investment, loan conversion at a discount, and in-the-money options produce a fully diluted post-money valuation of $18,933,336, with 2,366,667 total shares at an $8 post-transaction price. That’s the version of reality you need to model, not the pretty version in the first draft of the term sheet.

Post-Money vs Pre-Money Valuation A Critical Distinction

Founders mix up pre-money and post money valuation all the time. Investors usually don’t.

That difference costs founders equity.

Pre-money valuation is the value of the business before the new capital goes in. Post money valuation is the value after the capital goes in. The distinction sounds minor until you realize it changes the ownership math and exposes what the investor is really buying.

Reverse-engineer the term sheet

Use the reverse formula when the term sheet leads with ownership instead of valuation:

Post money valuation = investment ÷ ownership percentage

According to AngelList’s guide to post-money valuation, if you raise $2 million for 10% equity, your post money valuation is $20 million. Your pre-money valuation is $18 million.

That one formula gives you immediate clarity. If the investor says, “We’re putting in $4 million for 10%,” you already know they’re implying a $40 million post money valuation. You don’t need to wait for them to define it for you.

Why the market shifted

This isn’t just academic finance language. It changed how early-stage deals get negotiated.

AngelList notes that 80% of US/EU VC deals use a post-money basis for priced rounds, and ties that shift to Y Combinator’s 2018 post-money SAFE update. The reason is simple. Post-money structures make ownership clearer at the moment of the deal.

That’s good for investors, and if you know what you’re doing, it’s also good for you. Ambiguity usually hurts the founder more than the fund.

A side-by-side comparison

| Issue | Pre-money valuation | Post money valuation |

|---|---|---|

| What it measures | Company value before investment | Company value after investment |

| What founders focus on | Headline valuation | Actual ownership after closing |

| What investors focus on | Entry price | Ownership purchased |

| Best use in negotiation | Starting point | Final reality |

What to say in the room

Don’t ask, “What valuation are you offering?”

Ask these instead:

- What ownership does this buy you on a fully diluted basis?

- Is the option pool included before or after the round?

- What converts at closing?

- What does the cap table look like immediately after the financing?

A founder who asks only for valuation gets a sales pitch. A founder who asks for the fully diluted cap table gets the truth.

If the investor can’t or won’t show post-closing ownership clearly, treat that as a warning sign.

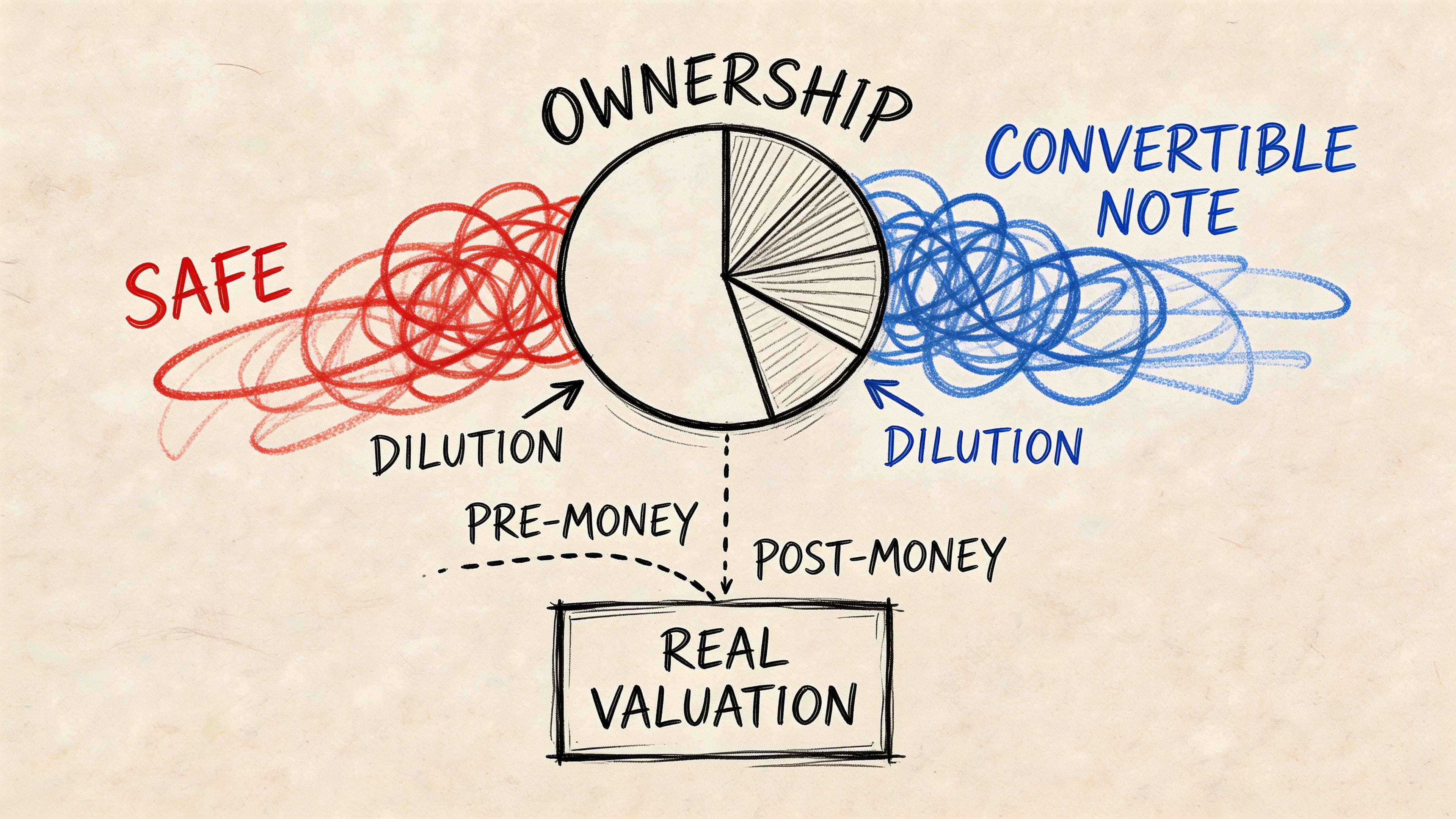

How Fundraising Instruments Impact Your Real Valuation

The term sheet headline is almost never the full economic story.

The complete story sits in the instruments around the round. SAFEs, convertible notes, option pools, and conversion mechanics decide whether your post money valuation holds up or turns into a dilution problem.

Fully diluted is the only version that matters

If your investor says they’re taking a certain percentage, your next question should be: “On what share count?”

If the answer isn’t “fully diluted,” stop there and make them clarify.

Fully diluted means you count all shares that exist now and all shares that can reasonably come into existence through conversion or exercise. That includes options that are in the money and convertible instruments that trigger at the round.

Here’s the trap. You think you’re selling one stake to a new investor. In reality, you may be diluting yourself through three channels at once:

- The new money itself

- Prior SAFEs or notes converting

- An employee pool expansion

Convertible notes and discounts change the share count

A discounted note conversion can materially change ownership if you don’t model it before signing.

For instance, a note with a discount can convert into a substantial number of shares, contributing to the fully diluted post-money valuation in that scenario. The lesson is straightforward. The note isn’t background noise. It changes the denominator, which changes everyone’s ownership.

Option pools are dilution, even before they're granted

Founders often treat the option pool like a future HR issue. It’s not. It’s a current financing issue.

If investors ask for a larger pool to be created before the round closes, that dilution usually hits existing holders first. That means you and your current investors absorb it before the new money even starts owning shares. Legal and investor education also matters here. If you’re navigating the broader mechanics and risks of investing in private placements, it helps to understand how these structures can look simple on paper but shift economics materially once all terms are enforced.

Early angels get hit first if nobody models the future rounds

The uglier version of dilution shows up over multiple rounds.

According to Angel Investors Network’s first-time angel investor guide, a 0.5% seed stake from a $25,000 investment at a $5 million valuation can shrink to less than 0.2% after Series A and B rounds. That pushes the required exit from $50 million to $250 million to deliver the same return.

That’s not just an angel problem. It tells you what repeated fundraising does to every early holder who doesn’t maintain ownership.

Here’s the operating lesson for founders:

| Instrument | What founders often assume | What actually happens | |---|---| | SAFE | “We’ll deal with it later” | Ownership impact shows up at the priced round | | Convertible note | “It’s small debt” | It converts into equity and dilutes at closing | | Option pool | “It’s for future hires” | It can dilute founders before the round | | New round | “It’s only this investor” | Every round resets control and ownership dynamics |

A useful explainer before you finalize terms:

What to do before you sign

Don’t accept summary math from counsel or investors. Build the actual cap table model.

Include:

- Current issued shares

- All SAFEs and notes

- Discounts or valuation caps

- Existing option pool

- Any proposed pool increase

- The new investment

- Post-close ownership by stakeholder

Investor-ready advice: If you can’t explain your post-close cap table in one page, you’re not ready to sign a financing document.

Calculating Post-Money Valuation Worked Examples

You don’t need more theory. You need to see the math work.

These examples use the verified numbers available and show how a founder should think about post money valuation in a live financing process.

SaaS Series A example

Start with the clean version.

A SaaS company raises $5 million on a $25 million pre-money valuation. According to LTSE’s discussion of post-money valuation, that produces a $30 million post money valuation and gives the investor 16.67% ownership.

Now add the complication that founders often ignore. The company also needs a 15% ESOP post-round.

If you only focus on the investor’s 16.67%, you miss the second source of dilution. The option pool increases total dilution to founders beyond the headline investor stake.

Step-by-step cap table logic

Assume the company starts with founder ownership only. For illustration, use a simple share count of 1,000,000 pre-round founder shares so the percentages are easier to see.

| Stakeholder | Pre-Round Shares | Pre-Round % | Post-Round Shares | Post-Round % |

|---|---|---|---|---|

| Founders | 1,000,000 | 100% | 1,000,000 | 68.33% |

| New Series A Investor | 0 | 0% | 243,902 | 16.67% |

| ESOP Pool | 0 | 0% | 219,512 | 15.00% |

| Total | 1,000,000 | 100% | 1,463,414 | 100% |

How did we get there?

- Investor must own 16.67% post-round.

- ESOP must equal 15% post-round.

- Founders keep the residual, which is 68.33%.

So total post-round shares must be whatever number makes 1,000,000 founder shares equal 68.33% of the company. That total is 1,463,414 shares in this illustration. Once you have that total:

- Investor shares = 16.67% of total = 243,902

- ESOP shares = 15% of total = 219,512

That shows the full cap table effect. Your dilution didn’t stop at the financing.

If you’re building this in Excel, QuickBooks-linked planning files, or NetSuite exports, use a dedicated financial modeling for startups workflow instead of a one-tab spreadsheet with circular assumptions hidden in the background.

What founders should take from this

Benchmarking matters too. LTSE notes that 8-12x ARR multiples are a useful reference point for SaaS firms in the $5-20M revenue range. If your business fundamentals don’t support the implied valuation, a headline number can set you up for a painful next round.

Strategic investment example for a services firm

Service businesses often get less help on valuation mechanics, but the math is the same.

Suppose you run a professional services firm and an investor offers $2 million for 10% equity. Using the reverse formula from the earlier section, that implies a $20 million post money valuation and an $18 million pre-money valuation.

Now compare that with a more founder-unfriendly version of the same conversation.

If another investor offers $2 million for 15%, your implied post money valuation drops to $13.33 million using the formula investment ÷ ownership percentage, based on the verified example from Wall Street Prep. The cash amount is identical. The ownership cost is not.

Side-by-side comparison

| Offer | Investment | Equity Sold | Implied Post Money Valuation |

|---|---|---|---|

| Offer A | $2 million | 10% | $20 million |

| Offer B | $2 million | 15% | $13.33 million |

This is why founders should stop saying, “We’re raising two million,” as if the amount itself defines the deal quality. Price matters. Ownership matters more.

If two term sheets bring in the same cash, the better deal is the one that preserves more of your company without setting up the next round to fail.

The worked-example takeaway

Use these examples as a checklist:

- Run the round on both a headline and fully diluted basis

- Model the option pool before agreeing to it

- Convert every ownership ask back into an implied valuation

- Stress-test the next round, not just this one

If you can’t show your board or co-founders exactly how ownership changes after close, you’re still negotiating blind.

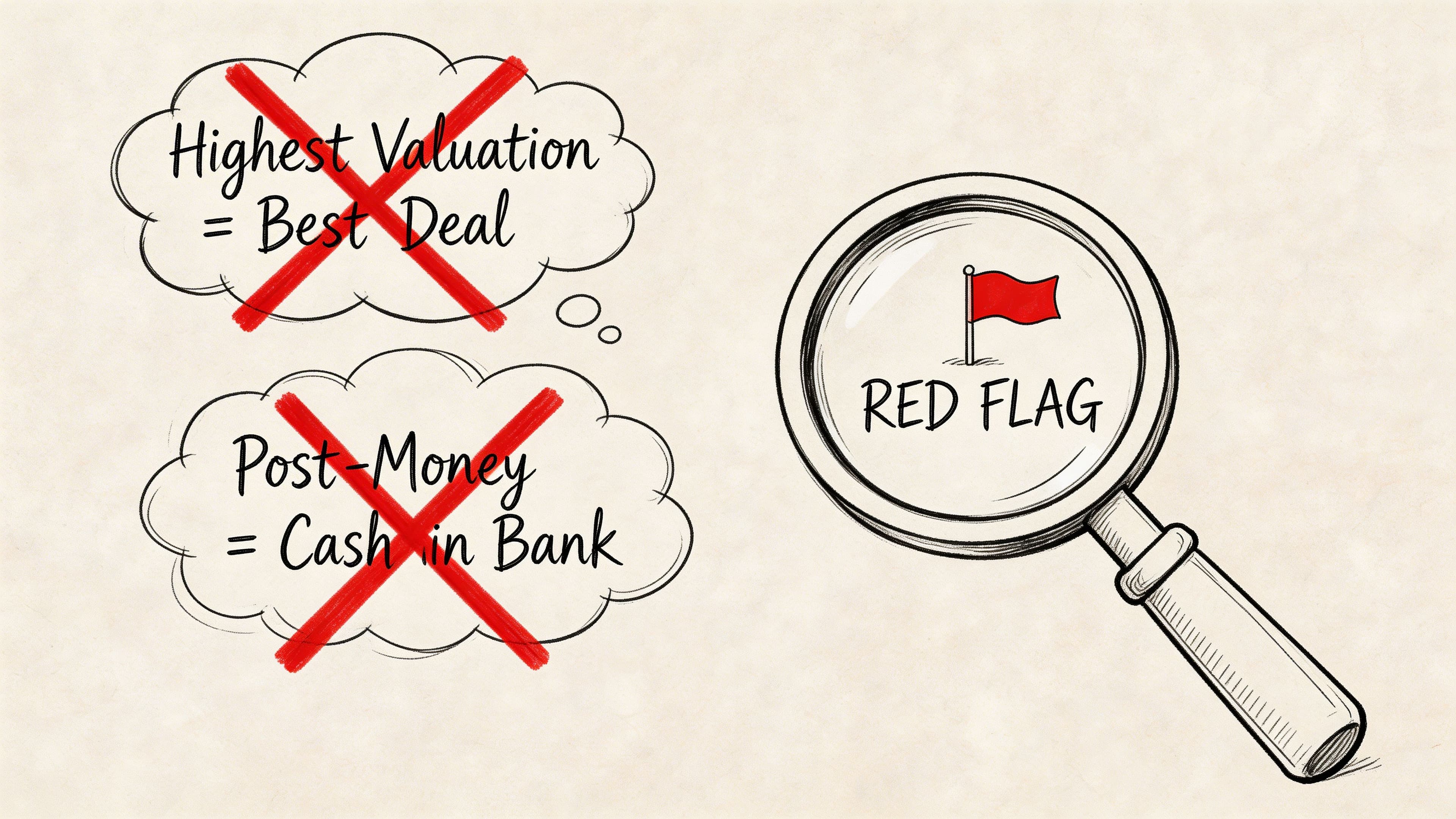

Valuation Red Flags Common Founder Misconceptions

Founders repeat the same bad assumptions in fundraising. Investors benefit when you keep repeating them.

Higher valuation is always better

No. A higher valuation with weak support creates pressure, not protection.

If your current metrics, revenue quality, retention, or margin profile don’t justify the price, the next round becomes harder. You end up defending a number instead of telling a growth story.

A defensible round beats an inflated round.

The SAFE cap is my valuation

No. It’s a conversion mechanism, not a clean statement of enterprise value.

Founders often wave around a SAFE cap as if it proves what the company is worth today. That’s sloppy. A cap affects future conversion economics. It does not eliminate the need to model dilution, especially if multiple instruments stack before a priced round.

Option pool expansion is just admin

Also wrong. The timing of the pool creation matters.

If the investor requires the pool to be created before their money lands, existing holders absorb the dilution first. If you ignore that detail, you’ll tell yourself you sold one stake while your founder ownership drops further.

Red flags to stop on immediately

- Investor avoids fully diluted ownership math

- Counsel sends documents before the cap table model is agreed

- SAFE and note conversions are described as minor

- Pool increase is presented as routine and left unquantified

- Revenue quality issues are glossed over during diligence

If your revenue, deferred revenue, or margin presentation is loose, clean that up before you talk valuation. A proper quality of earnings review will surface issues that experienced investors will find anyway.

Bad financing terms rarely arrive labeled as bad terms. They arrive packaged as speed, simplicity, and market standard language.

Achieving Investor Readiness Beyond the Valuation Number

Valuation doesn’t start with the term sheet. It starts with the quality of your financials.

If your accounting is weak, your valuation argument is weak. If your revenue recognition is sloppy, your pre-money number will get pushed down by investors who know they’re taking diligence risk.

ASC 606 is a valuation issue, not just an accounting issue

For SaaS firms, this matters more than most founders realize.

According to Carta’s overview of pre-money vs. post-money valuations, ASC 606 revenue recognition can artificially lower current revenue by 20-40% because revenue is deferred, and 65% of SaaS audits flag valuation mismatches tied to this issue. If you don’t explain deferred revenue and contract value properly, investors can anchor to a lower pre-money valuation than your operating reality supports.

That’s not a bookkeeping nuisance. That’s dilution.

What investor-ready actually looks like

Investors will trust your valuation argument when your finance operation is coherent.

That means:

- Revenue is recognized correctly: Especially for annual and multi-year SaaS contracts.

- Deferred revenue is explained clearly: Not buried in a footnote.

- KPIs are tied to the general ledger: MRR, ARR, CAC, and retention should reconcile to the books.

- Forecasts connect to cash: Growth plans without cash logic don’t survive diligence.

A strong narrative matters too. If you’re refining your fundraising story, this guide on how to pitch to investors is useful because it pushes you to match story, traction, and financial evidence.

What to clean up before the process starts

Use this short operating checklist:

| Area | What investors want to see |

|---|---|

| Revenue recognition | Clear ASC 606 treatment |

| Cap table | Current and fully diluted versions |

| Metrics | MRR, ARR, churn, CAC tied to books |

| Forecast | Assumptions tied to actual performance |

| Close process | Consistent monthly reporting |

Operating standard: If your books can’t support your pitch deck, your valuation won’t hold up in diligence.

The founders who negotiate best aren’t always the best storytellers. They’re the ones whose numbers survive scrutiny.

Get Your Financials Investor-Ready with Jumpstart Partners

You don’t win a funding round by sounding confident. You win it by showing clean numbers, clear ownership math, and a cap table that doesn’t fall apart under diligence.

That’s where most growing companies struggle. They have traction, but their reporting is late. Their revenue recognition needs work. Their financial model doesn’t fully account for dilution. Then the investor starts asking sharper questions, and the founder loses control of the conversation.

Jumpstart Partners helps fix that. Their team supports SaaS, agency, and service businesses with investor-ready financials, controller-level oversight, and the reporting discipline founders need before a raise. If you need a stronger finance function before the next term sheet arrives, review their approach to CFO services for startups.

You should go into a raise knowing exactly how the round changes your ownership, not guessing after legal documents start moving.

If you’re preparing for a funding round and want your cap table, forecasts, and financials tight before investor diligence starts, talk to Jumpstart Partners. They help founders turn messy books and vague dilution math into clear, investor-ready numbers you can negotiate from with confidence.