Financial Operations

SAFE vs Convertible Note: A Founder's Decision Guide

Deciding between a SAFE vs convertible note? Our guide compares dilution, cap tables, legal risks, and accounting to help founders choose the right instrument.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··16 min readIn the first half of 2023, 65% of pre-seed rounds were structured as SAFEs or convertible notes, up from 38% in 2020, according to SPZ Legal's pre-seed funding analysis. That shift matters because your first fundraising instrument doesn't just get cash into the bank. It changes how you model dilution, how your balance sheet reads, how an auditor will ask questions, and how hard your next round feels.

Most founders approach safe vs convertible note as a legal form choice. That's too narrow. If you're running a SaaS company, agency, or services business with real revenue, you need to think like a finance lead. You're not just signing a document. You're setting terms that will flow into your cap table, your general ledger, and investor diligence.

Table of Contents

- Why Your First Funding Choice Matters More Than You Think

- SAFE vs Convertible Note At a Glance

- Understanding Founder and Investor Preferences

- How Each Instrument Impacts Your Cap Table and Dilution

- The Hidden Risks in Accounting Legal and Bankruptcy

- A Decision Framework for Choosing the Right Instrument

- Your Financial Action Plan Before You Raise

Why Your First Funding Choice Matters More Than You Think

The biggest mistake I see is founders treating early financing as temporary paperwork. It isn't temporary. A SAFE or a convertible note sits underneath your next institutional round, and if you don't model it correctly, it creates confusion around dilution, debt presentation, and conversion mechanics right when you're trying to look investor-ready.

That's why this choice carries more weight than the check size suggests. A simple instrument can still create messy outcomes if you stack multiple rounds, track them poorly, or ignore how they convert in a priced round. Founders usually focus on speed. Finance teams have to focus on what happens after the signature.

If you want a legal perspective before you negotiate, this legal guide to seed funding choices is a useful companion to the finance lens. And before you even discuss caps or discounts, make sure you understand how investors talk about post-money valuation, because that framing drives dilution conversations fast.

Why this decision shows up later

A poor choice usually surfaces in one of four places:

- During cap table cleanup when no one can explain how multiple instruments convert

- During lender or investor diligence when debt and equity-like instruments are recorded inconsistently

- During audit prep when supporting schedules don't match signed documents

- During the next round when founders realize accrued interest or cap terms create more dilution than expected

Practical rule: If you can't explain the conversion math and the balance sheet treatment before you sign, you're not ready to issue the instrument.

For most operating businesses in the $500K to $20M revenue range, the right answer isn't the one that sounds founder-friendly. It's the one you can document cleanly, forecast accurately, and defend in diligence.

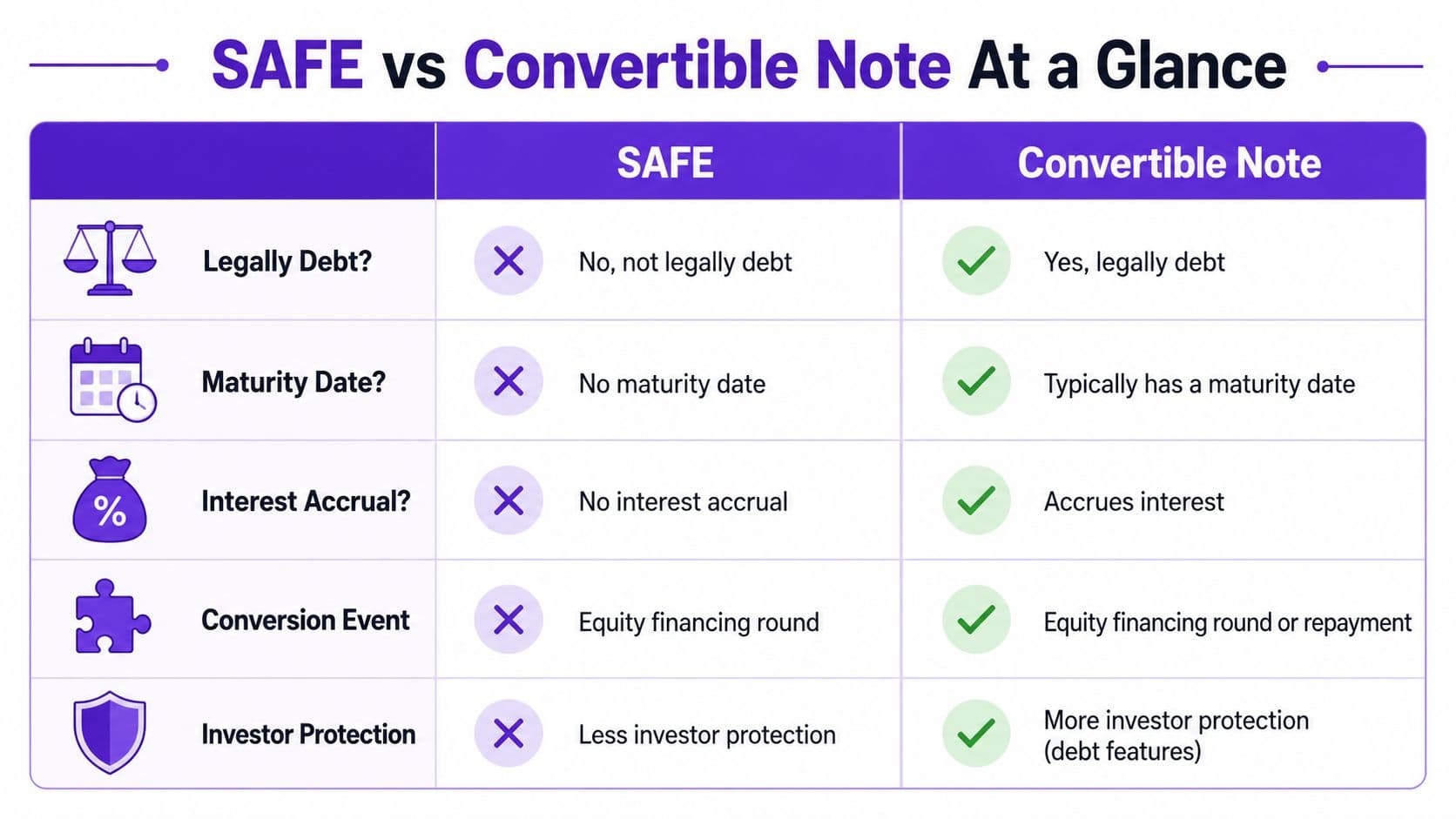

SAFE vs Convertible Note At a Glance

The core difference is simple. A SAFE is not debt. A convertible note is debt that later converts into equity. That one distinction drives everything else.

The fastest way to understand the difference

| Term | SAFE | Convertible Note |

|---|---|---|

| Legal structure | Not debt | Debt instrument |

| Interest | None | Typically accrues interest |

| Maturity date | None | Typically has a maturity date |

| Pressure if next round slips | Lower | Higher |

| Repayment possibility | Generally no repayment feature like debt | Can create repayment or renegotiation pressure |

| Investor protection | Lighter | Stronger because of debt features |

| Documentation style | Usually simpler | Often more customized |

| Cap table administration | Simpler to track | More moving parts because of accrued interest and debt terms |

A concise way to frame it comes from Mark Suster of Upfront Ventures: “A convertible note is debt that you hope becomes equity. A SAFE is not debt. It's a promise for future equity.”

For founders managing multiple investors, clean records matter as much as clean legal docs. Use actual capitalization table software, not a spreadsheet you hope still works at Series A.

A short walkthrough can help if your team is visual:

What the main terms mean in plain English

Here's the practical translation of the jargon:

- Valuation cap means the investor gets the benefit of a lower company value if your next round prices much higher.

- Discount means the investor buys into the next round at a lower price per share than the new money.

- Interest applies to notes, not SAFEs. That interest usually converts too, which increases the share count.

- Maturity date is the clock on a note. If you haven't raised a qualifying round by then, the note becomes a real negotiation problem.

A SAFE is cleaner because fewer terms interact. A note is more layered because you have principal, accrued interest, maturity, and conversion language all moving together.

Understanding Founder and Investor Preferences

The safe vs convertible note debate usually isn't about legal theory. It's a negotiation between your need for flexibility and the investor's need for protection.

Why founders usually want the SAFE

Founders tend to prefer SAFEs because they remove near-term financing stress. Industry guidance summarized by Allied Venture Partners notes that a SAFE has no maturity date and no interest, while a convertible note typically carries 5% to 8% annual interest and a 12 to 24 month maturity date. That difference matters when your roadmap slips or the fundraising market tightens.

If you're still refining product-market fit or your revenue base isn't yet consistent, a SAFE gives you breathing room. You don't have debt aging in the background. You don't have interest building up. You also don't have a maturity date forcing a conversation when your position isn't strong.

This broader Founder Connects funding guide is helpful if you want to understand how investors compare structures across stages. It's especially useful when you're preparing to explain your choice to angels who come from outside venture.

Why investors still ask for notes

Investors often prefer notes for exactly the reasons founders don't. Debt gives them additional protection if the company never reaches a priced financing. A note puts them in a stronger position in a downside scenario and gives them more advantage if timing drags.

That preference shows up most often with:

- Traditional angel investors who want familiar loan-style protections

- Bridge round participants who expect a defined timeline to the next round

- Investors outside the core startup ecosystem who understand debt better than equity contracts

If your team is still learning the fundraising vocabulary, it helps to get clear on what VC means in practice, because many misunderstandings here are really stage and investor-type mismatches.

Investors don't ask for a note because they dislike your company. They ask for a note because the debt structure gives them more tools if the company misses the next financing milestone.

The practical takeaway is direct. Founders optimize for speed and lower pressure. Investors optimize for protection and advantage. Your job is to decide which trade-off fits your actual business, not your ideal fundraising story.

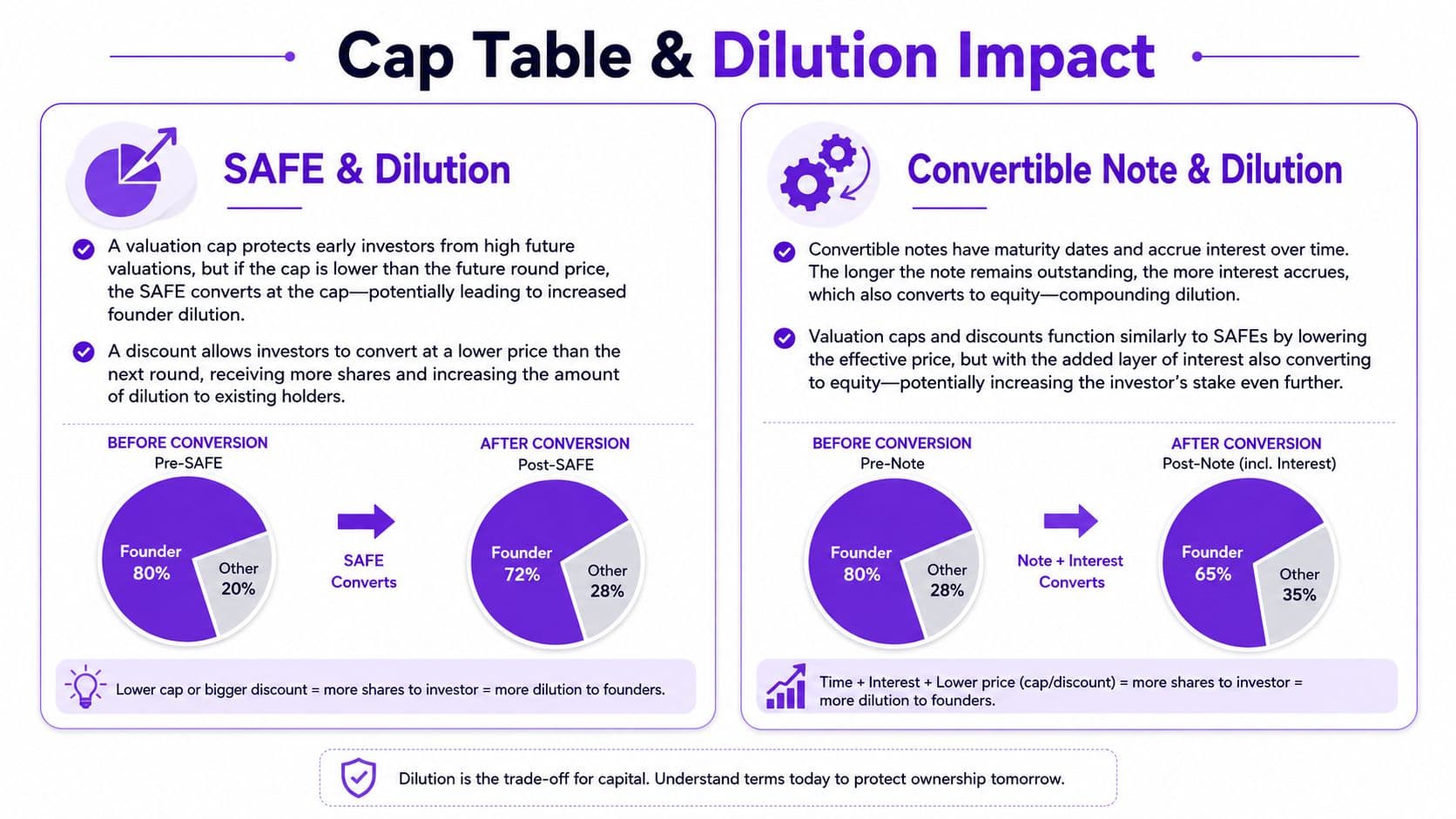

How Each Instrument Impacts Your Cap Table and Dilution

The practical implications of safe vs convertible note become apparent. If the documents have the same cap and discount, founders often assume dilution will be roughly the same. It won't be if the note accrues interest before conversion.

A worked example with real numbers

Use this scenario:

- Investment amount: $500,000

- Valuation cap: $5,000,000

- Discount: 20%

- Next round: Series A at $10,000,000 pre-money

- Series A price per share: $1.00

- Convertible note interest: 6% annual

- Time outstanding: 18 months

Now calculate conversion.

Step 1: Compare cap price vs discount price

- Under the discount, the conversion price is $1.00 × 80% = $0.80

- Under the cap, the conversion price is based on the cap relative to the priced round and results in $0.50

The investor gets the better deal, which is the lower price. So both the SAFE and the note convert at $0.50 in this example.

Step 2: SAFE conversion

The SAFE converts only on the invested amount.

- $500,000 ÷ $0.50 = 1,000,000 shares

Step 3: Convertible note conversion

The note converts on principal plus accrued interest.

Interest for 18 months at 6% annual on $500,000:

- Annual interest = $30,000

- 18 months interest = $45,000

Total amount converting:

- $500,000 + $45,000 = $545,000

Shares issued:

- $545,000 ÷ $0.50 = 1,090,000 shares

What this means for founder ownership

The economics are straightforward. Same cap. Same discount. Same priced round. The noteholder still receives more shares because interest also converts.

| Instrument | Amount converting | Conversion price | Shares issued |

|---|---|---|---|

| SAFE | $500,000 | $0.50 | 1,000,000 |

| Convertible note | $545,000 | $0.50 | 1,090,000 |

That extra 90,000 shares is dilution you need to model before you sign. Not after your lawyer sends the final documents. Not when the Series A lead asks for a fully diluted cap table. Before.

If you're building this model from scratch, use a structured startup valuation framework so your cap assumptions, share price assumptions, and round math stay connected.

Working rule: A note with the same headline economics as a SAFE usually costs more ownership if it sits outstanding long enough to accrue meaningful interest.

Red flags when you model conversion

Watch for these problems:

- You model only principal and forget that note interest converts into equity.

- You ignore timing and assume the next round closes quickly.

- You compare headline caps only without checking whether the lower of cap or discount drives the result.

- You let multiple instruments pile up with different terms and no unified conversion schedule.

- You don't reconcile legal docs to cap table software before investor diligence starts.

Founders don't usually get hurt by one SAFE or one note. They get hurt by unmodeled stacking.

The Hidden Risks in Accounting Legal and Bankruptcy

The legal form drives accounting consequences. That's the part most startup content skips, and it's where finance teams get dragged into cleanup work later.

How these instruments hit your books

A convertible note is debt. In practical accounting terms, that means you usually record the cash received as a liability and then track the note balance over time, including accrued interest. In QuickBooks or Xero, that often means setting up a dedicated long-term liability account, posting the initial funding entry there, and recording interest accrual through journal entries based on the signed terms.

A SAFE creates a different bookkeeping challenge. It isn't debt, but it also isn't ordinary operating revenue and it shouldn't land in some generic equity bucket with no support. Your controller needs a clear policy, consistent classification, and supporting schedules that tie each SAFE to executed agreements and cap table records.

From a reporting standpoint, the practical difference is clear:

| Issue | SAFE | Convertible Note |

|---|---|---|

| Balance sheet posture | Often treated outside standard debt presentation | Recorded as liability until conversion |

| Ongoing accruals | No interest accrual | Interest accrual must be tracked |

| Reconciliation burden | Agreement tracking and cap table alignment | Agreement tracking, amortization or accrual schedules, and cap table alignment |

| Lender optics | Generally cleaner than debt | Can complicate leverage discussions |

I'm deliberately avoiding one-size-fits-all technical conclusions under ASC 480 or ASC 470, because classification depends on the actual language in the instrument. Your auditor will read the terms, not the label.

What breaks during audit and diligence

Audit pain usually comes from process failure, not theory.

Common problems include:

- Unsigned or inconsistent documents across investors

- Interest schedules that don't tie out to the ledger

- Cap table files that conflict with legal records

- No memo explaining classification for a SAFE or note

- Repayment or conversion clauses that no one flagged before diligence

Before a financing, acquisition, or audit, use a disciplined financial due diligence checklist so the instrument terms, accounting entries, and board records match.

Downside scenarios founders ignore

If the business fails before a priced round, a convertible note holder is generally in a stronger position than a SAFE holder because the note is debt. That difference is not theoretical. It affects who stands in line first when assets are limited.

Global structuring can complicate this further. A legal analysis summarized by JD Supra's discussion of ASAs, SAFEs, and convertible loan notes notes that in the UK, founders often use convertible loan notes and need to avoid redemption rights that would invalidate SEIS/EIS tax-advantaged treatment. If you have cross-border investors, don't assume a U.S.-style SAFE is automatically the clean answer.

The fastest way to create diligence friction is to use a simple instrument casually. Simple legal forms still need disciplined accounting.

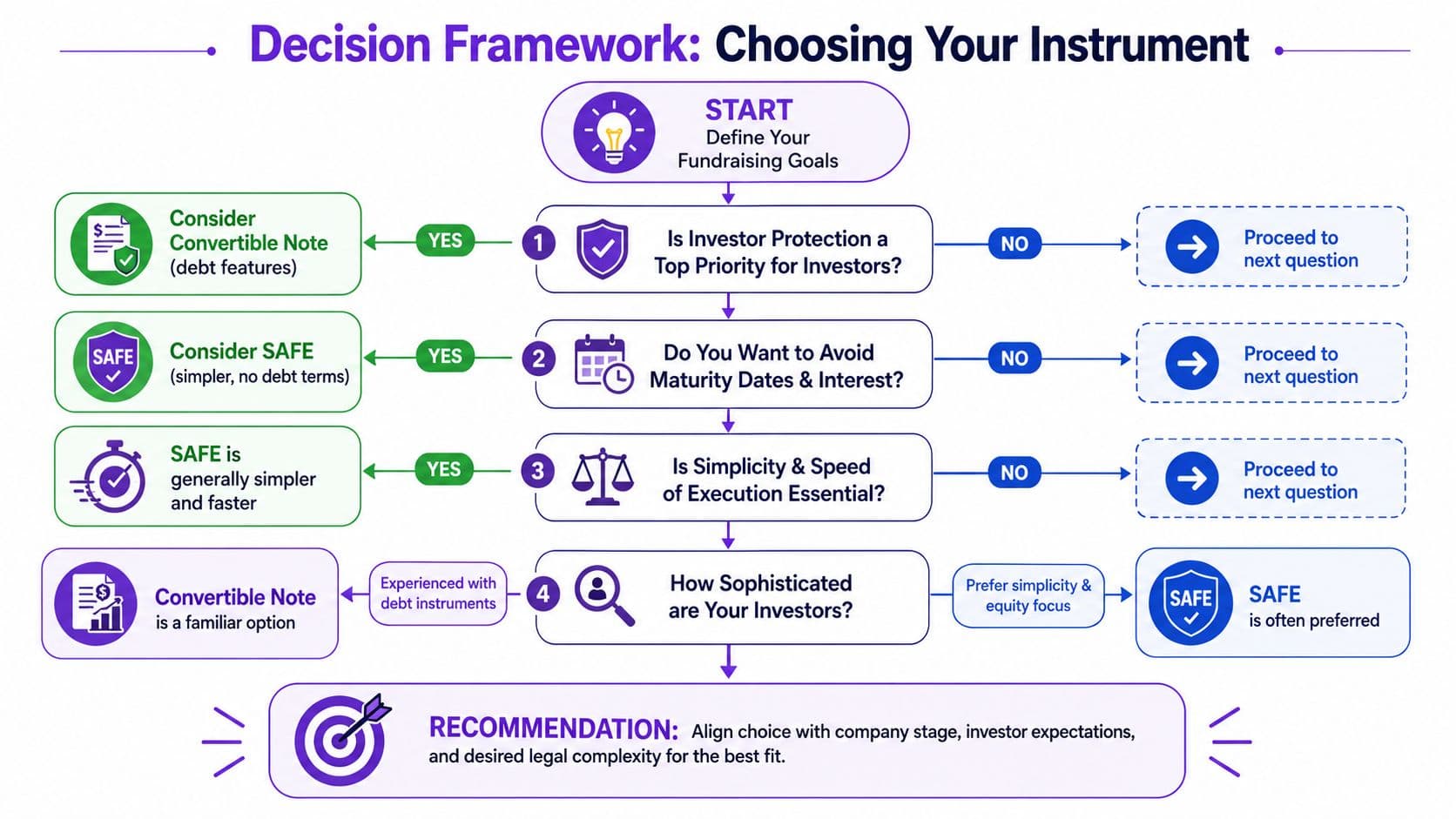

A Decision Framework for Choosing the Right Instrument

Most founders don't need more theory. They need a decision they can defend.

Mark Suster's framing is still the cleanest lens: “A convertible note is debt that you hope becomes equity. A SAFE is not debt. It's a promise for future equity.” That distinction should drive your choice.

When a SAFE is the better answer

Choose a SAFE when you care most about speed, cleaner administration, and removing maturity pressure.

That usually fits companies that:

- are raising their first meaningful outside capital

- don't want interest building while they refine growth

- expect investor demand for a standard, simple instrument

- want fewer accounting moving parts before the next round

A SAFE is often the cleaner answer when your business needs flexibility more than structure.

When a convertible note is the better answer

Choose a note when investor protection is a real part of the deal and the parties want debt-style discipline.

That usually fits situations where:

- existing or incoming investors insist on debt features

- you're bridging to a more defined next financing event

- the investor base is more traditional or internationally debt-oriented

- the company can handle tighter documentation and accrual tracking

A note makes sense when the extra complexity serves a real commercial purpose.

A short decision table you can use with your board

| Situation | Better fit | Why |

|---|---|---|

| First outside round with angel-style investors | SAFE | Fewer moving parts and less financing pressure |

| Bridge capital with a defined next round | Convertible note | Debt structure aligns with timeline pressure |

| You want the simplest cap table administration | SAFE | No interest accrual and no maturity tracking |

| Investors want more downside protection | Convertible note | Debt features provide that protection |

| Cross-border or tax-sensitive structuring | Case by case | Local legal and tax rules can override simplicity |

If you want one sentence to guide the decision, use this: choose the instrument your business can support operationally, not the one that sounds easiest in a pitch meeting.

Your Financial Action Plan Before You Raise

Once you've picked the instrument, finance work starts immediately.

What to do in QuickBooks or Xero

- Create the right account structure: Set up a dedicated liability account for a note, or a clearly labeled equity-related account structure for a SAFE based on your accounting policy.

- Post the cash correctly: Don't run financing proceeds through revenue. Ever.

- Build a support schedule: Track investor name, execution date, amount, cap, discount, maturity, and for notes, interest terms.

- Calendar recurring entries: If you issue a note, schedule the interest accrual entries so you don't backfill them months later.

What to hand your lawyer tax team and investors

- A current cap table: Use Carta, Pulley, or another serious tool. Don't rely on a founder spreadsheet.

- A conversion model: Show what happens under the cap, discount, and note interest assumptions.

- A board-ready memo: Summarize why you chose the instrument and how it affects dilution and reporting.

- A diligence folder: Signed agreements, board approvals, ledger entries, and reconciliation files should all live in one place.

If this sounds heavier than you expected, that's normal. Early fundraising documents look simple. The downstream accounting rarely is.

If you want help recording a SAFE or convertible note correctly, cleaning up your cap table support, or getting investor-ready financials before a raise, talk to Jumpstart Partners. Their team helps growing companies put the accounting, reporting, and close process in order before financing complexity turns into diligence risk.