Financial Operations

What Does VC Mean? Your Guide to Venture Capital

What does VC mean for founders? Understand venture capital, what VCs seek, term sheets, dilution, and how to prep your financials for funding success.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··17 min readIn business, VC usually means venture capital: equity funding for startups and early-stage companies, where investors put in capital for ownership and often take a minority stake of 50% or less while aiming for an acquisition or IPO rather than loan repayment. If you searched “what does VC mean,” that's the answer that matters for your company, not voice chat, video call, or vice chancellor.

The popular advice is wrong. Too many founders treat VC like a trophy instead of a financing tool. That mindset wrecks good businesses. Venture capital is useful when you're building a company that needs outside capital to scale fast, accepts dilution, and can live with investor oversight, board pressure, and exit expectations. If that's not your model, VC isn't validation. It's a bad fit.

Table of Contents

- Is Venture Capital the Right Fuel for Your Business

- Venture Capital vs Other Funding Options

- The Venture Capital Funding Stages

- What VCs Look For Before They Invest

- Decoding the Term Sheet and Founder Dilution

- How VC Funding Transforms Your Financial Operations

- Your Action Plan to Become VC-Ready

Is Venture Capital the Right Fuel for Your Business

Most founders ask the wrong question. They ask, “What does VC mean?” when they should ask, “Should I take VC at all?”

Yes, VC can mean voice chat or video call in everyday digital use, and that matters for search intent, gaming, and education contexts, as noted in this VC full form explainer. But if you run a SaaS company, agency, or services firm, the business meaning is venture capital. That's the only meaning that changes your cap table, your board meetings, and your finance stack.

Ask the harder question first

Venture capital is not “money to grow.” It's equity financing built for high-growth companies that can justify rapid expansion and a future exit. If you want to build a durable, profitable company that you control for the long term, VC often creates more problems than it solves.

Here's the clean test:

- Take VC if your market is large, speed matters, and winning requires aggressive hiring, product investment, or market capture.

- Avoid VC if your business grows from cash flow, your margins are solid, and you value control more than speed.

- Pause fundraising if you don't yet have clean financials, credible unit economics, or a clear use of proceeds.

Practical rule: If outside capital won't materially change your strategic position, don't sell equity.

What taking VC really commits you to

Founders routinely underestimate the operational consequences of a venture round. Once you take VC, you're no longer just running a business. You're managing toward investor expectations.

That means:

| Decision area | Before VC | After VC |

|---|---|---|

| Growth pace | You choose it | Investors expect acceleration |

| Reporting | Basic monthly financials may be enough | Board-ready reporting becomes mandatory |

| Control | Founder-led | Shared with investors and often the board |

| Exit path | Flexible | Acquisition or IPO becomes the default outcome |

VC is the right fuel for a narrow set of companies. If your business needs rocket fuel, use it. If it needs discipline, focus, and cash generation, don't pour jet fuel into the engine.

Venture Capital vs Other Funding Options

Venture capital is private equity financing for startups and early-stage companies with high growth potential. Investors provide capital in exchange for equity and may take a minority stake of 50% or less, with the goal of making money through an acquisition or IPO rather than fixed repayment like a bank loan, according to SVB's explanation of venture capital.

That's why I tell founders to stop treating VC like general-purpose fuel. It's rocket fuel. Useful for escape velocity. Terrible for a business that just needs reliable operating capital.

Startup Funding Comparison

| Funding Type | Source | What You Give Up | Best For |

|---|---|---|---|

| Venture capital | Institutional investors and VC funds | Equity, some control, often board influence | Companies pursuing fast scale and a future exit |

| Bootstrapping | Your own profits and founder cash | Speed | Businesses with strong cash generation and control-focused founders |

| Bank loan | Lender | Repayment obligation and loan covenants | Predictable businesses that can service debt |

| Angel investors | Individual investors | Equity, usually with less structure than a VC round | Early-stage companies needing initial outside capital |

The real trade-off isn't cash

The trade-off is expectation. VC doesn't just fund growth. It changes the kind of company you're expected to build.

A bootstrapped firm can optimize for margin, retention, and founder control. A venture-backed company is expected to pursue scale, often before the business feels operationally comfortable. That's why founders should use a clear framework for founder decisions before they ever start a raise.

“Unit economics are the truth serum for SaaS businesses,” says Jason Lemkin, founder of SaaStr. “You can have beautiful growth charts and impressive MRR, but if you're spending $15,000 to acquire customers who only generate $12,000 in lifetime value, you're building a Ponzi scheme that collapses the moment you can't raise the next round.” This quote comes from Lemkin's piece on unit economics.

That example is blunt for a reason. If your revenue model only works when new investor cash fills the hole, you don't have a scalable business. You have financing dependency.

My recommendation by business type

- SaaS with real product pull: VC can fit if capital speeds product development, hiring, and go-to-market in a meaningful way.

- Digital agencies: VC usually doesn't fit. Services revenue is often people-constrained, not software-scalable.

- Professional services firms: Debt or self-funding is usually cleaner because ownership matters and growth is steadier.

- Hybrid SaaS plus services businesses: Raise only after you know which engine is driving enterprise value.

If you can reach your goals without selling equity, start there. Equity is the most expensive capital you'll ever use.

The Venture Capital Funding Stages

A venture round is never just “we raised money.” It's a sequence. Each round carries a different promise to investors, and each promise creates new pressure on your team.

Seed Round

Seed money is for proving the business should exist. You're validating the problem, building the product, and showing early market pull. At this point, investors care more about founder insight and early signals than polished scale.

Use of funds usually centers on:

- Product build-out: shipping the first version customers will use

- Initial hiring: a small team that can ship and learn fast

- Early go-to-market: testing channels, messaging, and ICP fit

Series A and Series B

Series A is where the conversation shifts from possibility to repeatability. Investors want evidence that customers buy, stay, and expand. Your job is to show that growth can become a system.

Series B is different again. Now you're scaling what already works. That usually means building management layers, tightening forecasting, and proving the company can grow without financial chaos. If you want a deeper look at that stage, read this guide on what Series B funding means for scaling companies.

This short overview is useful if you want a visual walkthrough of how rounds tend to stack up over time.

Growth rounds

Later rounds are about expansion and optionality. New markets, bigger teams, international growth, acquisitions, and preparing for an IPO or strategic sale all become possible. But the finance burden rises fast too. At that point, weak reporting becomes a fundraising problem, not just an accounting problem.

A practical way to think about stages:

| Stage | Company condition | Investor expectation | Main finance need |

|---|---|---|---|

| Seed | Early validation | Convincing story plus early traction | Basic model and cash discipline |

| Series A | Signs of repeatability | Product-market fit and go-to-market logic | KPI reporting and forecast quality |

| Series B | Scaling engine | Operational efficiency and predictability | Board reporting and tighter controls |

| Growth | Expansion | Durable performance at scale | Advanced finance infrastructure |

If you can't clearly say what milestone this round will buy, you're not ready to raise that round.

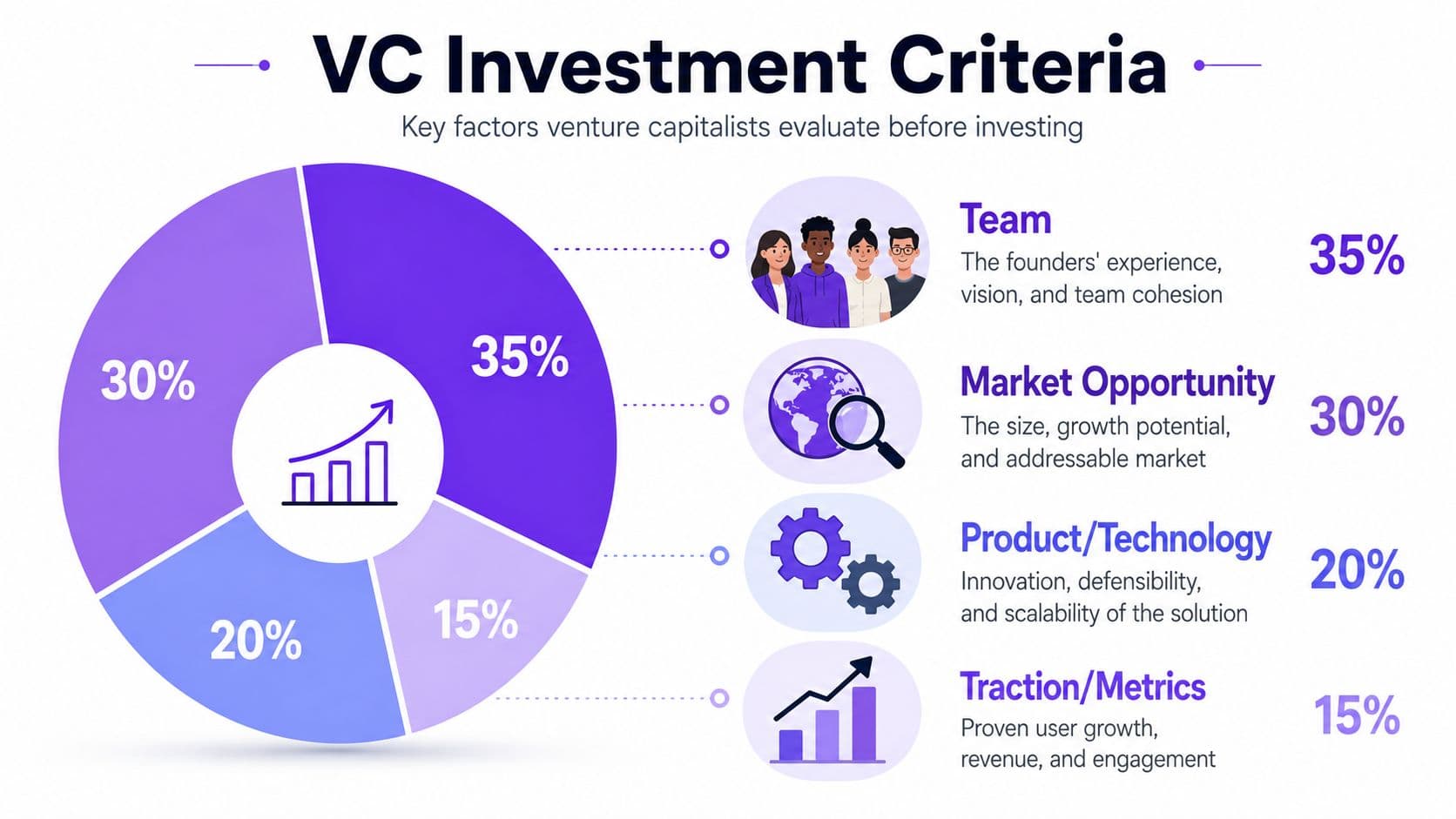

What VCs Look For Before They Invest

Venture investors are filtering hard. In Q1 2025, global venture investment reached $126.3 billion, the highest level in ten quarters, while deal count fell to 7,551. The United States captured over 70% of global funding, according to these venture capital market statistics. Bigger market, fewer deals, concentrated capital. That means you're not competing for attention in a casual environment. You're competing in a market that rewards clear outliers.

The story has to be investable

A good pitch isn't a deck full of adjectives. It's a sharp claim about why your company should exist and why your team is the one to win.

VCs look for:

- Founder-market fit: You understand the customer problem at an unfair level.

- A market worth the effort: The opportunity has to support a large outcome, not just a nice business.

- Defensibility: Your product, distribution, or insight must get stronger as you grow.

- A credible path to speed: Investors need to believe capital will accelerate a business that already has momentum.

The numbers have to support the story

Many founders fall apart; they know the vision, but they can't defend the model. For SaaS and recurring revenue businesses, you need clean visibility into revenue quality, gross margin, retention behavior, CAC, and payback logic. If your definitions change every month, your pitch won't survive diligence.

A simple worked example makes the point:

| Metric | Example number |

|---|---|

| Monthly recurring revenue | $120,000 |

| Gross margin | 80% |

| Monthly churned revenue | $6,000 |

| New monthly recurring revenue | $18,000 |

From those inputs, a VC will immediately infer a few things. Your net MRR movement is positive because new recurring revenue exceeds churned revenue. Your gross profit on that MRR base is $96,000 per month. If you can't reconcile those numbers back to billing and accounting records, investors will assume the rest of the model is loose too.

Investors fund companies that know their numbers cold. Everyone else gets a polite pass.

If you need to tighten how you define and track these metrics, this guide on unit economics for growing companies is worth reviewing before your next investor conversation.

What gets you screened out fast

- Messy financials: revenue doesn't tie to the books

- Weak unit economics: customer growth masks a broken acquisition model

- No clear use of funds: you want money, but not for a precise milestone

- Founder vagueness: you can't answer detailed questions without hand-waving

VCs invest in narratives backed by evidence. If the evidence is weak, the story doesn't matter.

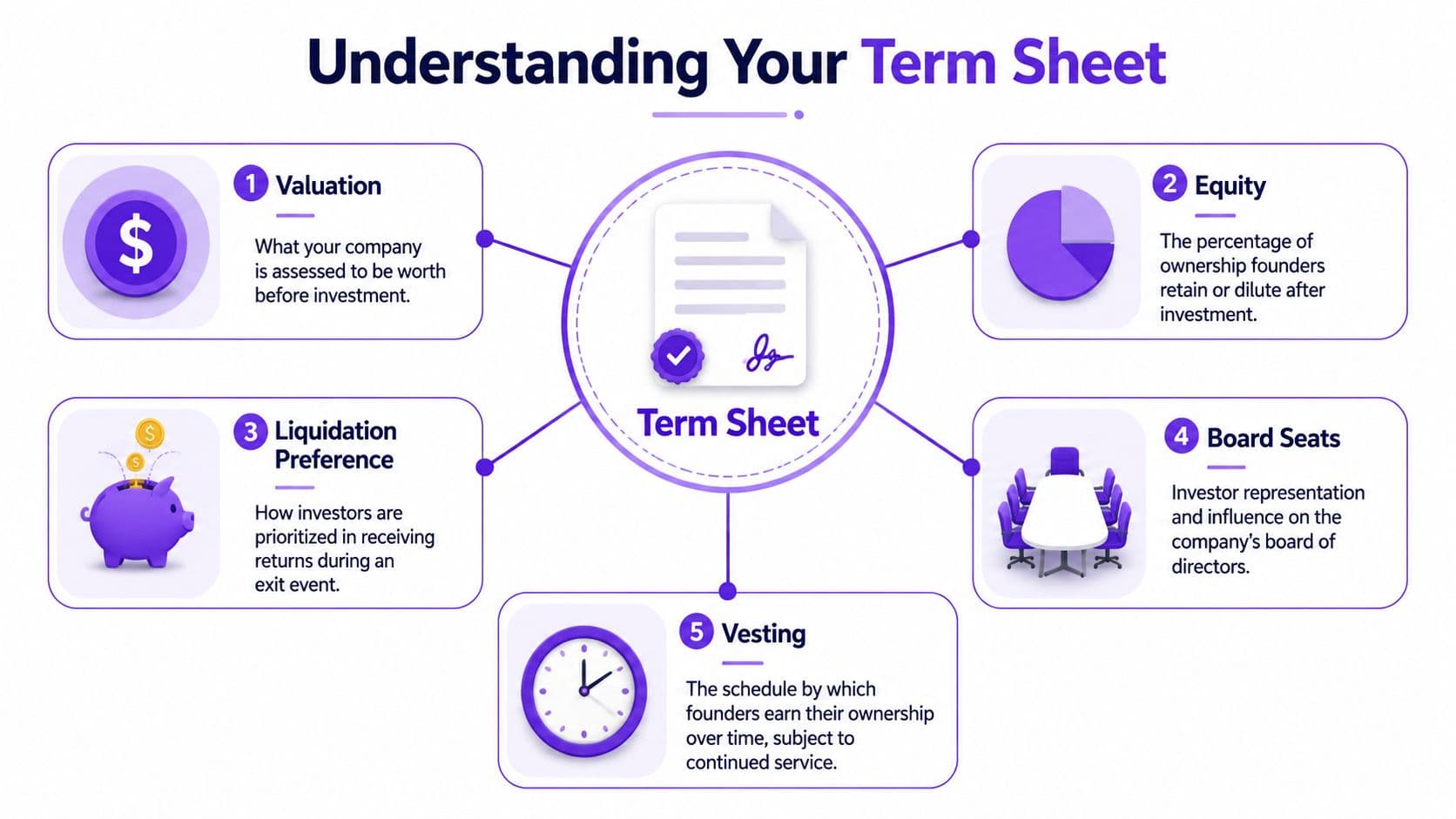

Decoding the Term Sheet and Founder Dilution

The term sheet is where enthusiasm turns into math. Founders love the headline valuation and ignore the mechanics that determine control and payout. That's backwards.

Start with valuation math

Use this basic example:

| Item | Amount |

|---|---|

| Pre-money valuation | $8,000,000 |

| New investment | $2,000,000 |

| Post-money valuation | $10,000,000 |

| Investor ownership | 20% |

The calculation is straightforward. Post-money valuation equals pre-money valuation plus new investment. Investor ownership equals new investment divided by post-money valuation. In this example, $2,000,000 divided by $10,000,000 equals 20%.

Now apply that to founders. If the founders owned the whole company before the round, they collectively own 80% after the round.

Dilution compounds over rounds

Here's the part founders underestimate. Dilution doesn't happen once. It stacks.

Assume you own 80% after the first round. Later, the company raises another round and sells 25% of the company post-money to new investors. Your 80% doesn't drop by 25 percentage points. It gets multiplied by the remaining ownership pool.

Worked example:

| Step | Calculation | Founder ownership |

|---|---|---|

| After first round | 100% less 20% sold | 80% |

| After second round | 80% × 75% remaining | 60% |

That's how you go from controlling the whole company to holding a much smaller stake than you expected.

If you need a cleaner primer on the math, review this article on post-money valuation and ownership.

Terms that matter as much as price

Valuation matters. It isn't the only thing that matters.

Pay attention to:

- Liquidation preference: This governs who gets paid first in an exit.

- Board seats: This affects who controls major decisions.

- Pro-rata rights: Existing investors may preserve their ownership in future rounds.

- Founder vesting: Your ownership may continue vesting over time, even after founding the company.

For founders dealing with private offerings and investor disclosure documents, this private placement memorandum guide is a useful legal-context reference.

Warning sign: A “great valuation” with harsh control terms is often worse than a lower valuation with cleaner economics.

Red flags

- You only negotiated price: You ignored governance and downside economics.

- You don't understand liquidation preference: Then you don't understand your payout in an exit.

- You gave up board control too early: That decision is hard to reverse.

- You're optimizing for announcement value: Press doesn't protect founder equity.

A term sheet isn't a trophy. It's a long-term operating agreement with economic consequences.

How VC Funding Transforms Your Financial Operations

Once you take venture money, bookkeeping stops being enough. Investors don't want vibes. They want a finance function.

Your reporting standard changes overnight

Before VC, many companies get away with cash-basis habits, messy revenue mapping, and founder-built spreadsheets. After VC, that approach breaks. You need monthly close discipline, board reporting, budget versus actual analysis, and reliable cash visibility.

For SaaS companies, revenue recognition also gets more technical. Deferred revenue, annual contracts, implementation fees, discounts, and contract modifications all create accounting complexity. If your reporting lags or your numbers change after the board packet goes out, trust erodes fast.

Board meetings expose weak finance teams

A venture-backed board will ask direct questions:

- Cash runway: How many months do you have at current burn?

- Plan variance: Why did hiring, margin, or revenue differ from budget?

- Sales efficiency: Are you buying growth profitably?

- Forecast confidence: Which assumptions are proven, and which are guesses?

If your controller function is weak, the CEO ends up answering from instinct. That's dangerous. Finance should provide the operating truth, not post-hoc explanations.

One practical resource is this guide to financial operations management for growing companies. If you need outside support, firms such as Jumpstart Partners provide outsourced controller and bookkeeping services designed for investor-ready reporting, KPI tracking, and cleaner close processes.

What you need in place

| Function | Minimum standard after VC |

|---|---|

| Monthly close | Consistent and documented |

| Revenue reporting | GAAP-aligned and reconcilable |

| Forecasting | Driver-based, not guess-based |

| Board package | Clear KPIs, cash view, and variance commentary |

VC doesn't just fund growth. It forces operational maturity. If your finance stack can't keep up, fundraising success becomes operational stress.

Your Action Plan to Become VC-Ready

Venture capital is equity financing for high-growth startups, typically exchanged for ownership and often board influence, and the key question is when it's appropriate versus slower, less dilutive funding paths, as summarized in this venture capital overview. That's the decision founders need to make before they ever start drafting an investor list.

Step 1 Validate whether VC fits your company

Don't raise because other founders raised. Raise because your model demands speed and your market rewards scale.

Use this filter:

- Choose VC if capital will help you reach a defensible position faster than operating cash can.

- Choose a slower path if you already have profitable growth and don't need institutional oversight.

- Wait if you still can't explain how this round changes the business in concrete terms.

Step 2 Get your financial house in order

Most fundraises weaken more than they should. Investors will forgive rough edges in a product. They won't forgive numbers that don't tie.

Your minimum checklist:

- Clean books: monthly close completed consistently

- Revenue clarity: recurring, non-recurring, deferred, and one-time items clearly separated

- KPI definitions: one agreed version of MRR, gross margin, CAC, churn, and runway

- Forecast model: a driver-based model that management uses

If your model is still built on assumptions nobody revisits, fix that first. A solid financial forecasting process for startups will do more for fundraising readiness than another pitch deck revision.

Step 3 Build a serious data room

Don't assemble diligence materials reactively. Build the package before meetings start.

Include:

- Historical financials with clean P&L, balance sheet, and cash flow statements.

- Current cap table that matches legal records.

- KPI reporting with definitions that reconcile to accounting data.

- Contracts and customer concentration view so investors can assess revenue quality.

Step 4 Run targeted outreach

Make a list of firms that invest in your stage, model, and geography. Generic outreach wastes time. Warm introductions help, but precision matters more. The right investor for a vertical SaaS company isn't automatically the right investor for an agency-tech hybrid.

Raise after you've built credibility, not while you're still inventing it.

If you're preparing for a fundraise and need investor-ready financials, a tighter close process, or a forecasting model your board will trust, talk to Jumpstart Partners. They work with growing SaaS, agency, and service businesses that need controller-level finance support before and after a venture round.