Financial Operations

Startup Company Valuation: Your 2026 Founder's Guide

Master 2026 startup company valuation. Learn DCF, Comps, SaaS metrics (LTV:CAC), and prepare financials for a defensible valuation. Get your founder's guide!

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··17 min readStartup valuation decides whether your round closes on terms you can live with.

Treat it like a fundraising tool, not a trophy number. Investors are tougher on weak assumptions, loose forecasting, and messy financials, especially in a first institutional round. If your price is hard to defend, the deal slows down, diligence gets painful, and your cap table pays for it later.

Ask a better question. What valuation can you support with operating data, investor logic, and a clear milestone plan for the next 12 to 18 months?

That is the number that matters.

For SaaS companies, that means showing credible growth, retention, gross margin, and efficient burn. For service firms, it means proving revenue quality, client concentration, delivery margins, and how much of the business depends on the founder. If your numbers are weak or inconsistent, fix the inputs before you pitch. Start with your reporting stack, your forecast, and a clean understanding of working capital. Founders who need to tighten the basics should review how to analyze a balance sheet before investor diligence.

A defensible valuation gets the deal done. It also gives you room to execute, hit your next milestones, and raise again without cleaning up avoidable mistakes.

Why Your Startup Valuation Is More Than Just a Number

Most founders start with the wrong mental model. They think valuation is an accounting output. It isn't.

For venture-backed companies, valuation is usually framed as pre-money or post-money value, and it's driven less by historical earnings and more by market dynamics, growth potential, and competition for the deal, as explained by Kruze Consulting's overview of startup valuations. Investors look at comparable rounds and exits, then ask a blunt question: if they invest at this price today, can they still hit their target return later?

That means your company can receive very different valuations at different times even if the business itself hasn't changed much. Funding environment matters. Sector momentum matters. Scarcity of capital matters.

What founders get wrong

A high valuation isn't automatically a win. If the number is inflated, you create problems immediately:

- You limit investor appetite: Many funds won't stretch beyond what their model supports.

- You compress future upside: If you can't grow into the valuation, your next round gets harder.

- You risk underfunding the business: You may raise too little because you're obsessed with dilution instead of milestones.

Practical rule: A defensible valuation beats a vanity valuation every time.

Founders in the $500K to $20M revenue range usually have enough operating history to tell a better story than a pre-seed startup, but not enough maturity to rely on pure finance theory. You need both narrative and numbers. Your financial package has to show traction, margin profile, customer quality, and cash discipline. If your reporting is sloppy, investors assume the business is sloppy too.

Many teams confuse bookkeeping with finance. Clean books won't set your valuation, but they will determine whether your valuation survives diligence. If your balance sheet doesn't tie, fix that before you pitch. A practical starting point is understanding how to analyze a balance sheet so your story matches your actual financial position.

What a defensible valuation really means

A defensible valuation has three parts:

- Comparable market logic

- Operational evidence

- A round structure that leaves enough cash to reach the next milestone

If one of those is weak, the whole thing breaks.

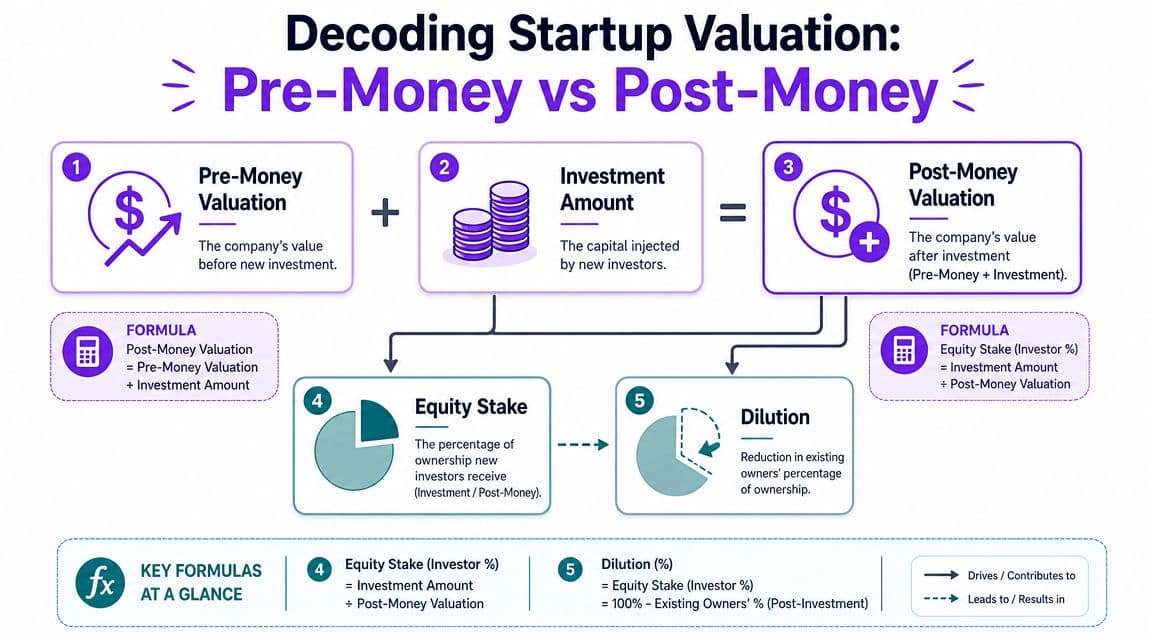

Pre-Money vs Post-Money Valuation Explained

You can't negotiate well if you don't understand the math. This part is simple, and you need to be able to explain it without notes.

For seed-stage startups, valuation usually comes from qualitative and early traction signals such as team quality, market size, initial traction, intellectual property, and comparable companies. But one mechanical rule always applies. Post-money valuation equals pre-money valuation plus the amount raised, and that directly determines investor ownership, as outlined by MicroVentures on startup valuations.

The core formulas

- Pre-money valuation = your company's value before new money comes in

- Post-money valuation = pre-money valuation + new investment

- Investor ownership = investment amount / post-money valuation

Worked example with real numbers

Say you raise $1,000,000 at a $4,000,000 pre-money valuation.

Your math looks like this:

| Item | Calculation | Result |

|---|---|---|

| Pre-money valuation | Given | $4,000,000 |

| New investment | Given | $1,000,000 |

| Post-money valuation | $4,000,000 + $1,000,000 | $5,000,000 |

| Investor ownership | $1,000,000 / $5,000,000 | 20% |

That means the new investor owns 20% of the company after the round closes.

Here's the second-order effect. Existing shareholders now own 80% collectively instead of 100%. That reduction is dilution.

Why this matters in negotiation

Founders often fixate on pre-money valuation because it sounds like the headline number. Investors care about post-money ownership because that's what determines their stake.

If you don't model dilution before the term sheet arrives, you're negotiating blind.

A useful next read is this breakdown of post-money valuation, especially if you're comparing multiple term sheet structures.

A short explainer can help if you're sharing this concept internally with co-founders or operators:

One more worked scenario

If you raise $2,000,000 instead at the same $4,000,000 pre-money valuation:

- Post-money = $6,000,000

- Investor ownership = $2,000,000 / $6,000,000

- Investor gets 33.33%

Same business. Different raise size. Very different cap table outcome.

That's why valuation discussions are never just about price. They're about ownership, control, and whether this round sets up the next one.

How Investors Calculate Startup Valuation Three Core Methods

Investors rarely use one method in isolation. They triangulate.

For later-stage or more financially complete technology companies, valuation shifts toward income-based and market-based approaches. Discounted cash flow becomes usable when future cash flows can be forecast with reasonable confidence, while EBITDA or revenue multiples dominate when comparable benchmarks exist. Smaller profitable tech firms often trade in EBITDA multiples of roughly 4.0x to 10.0x, according to Sofer Advisors' guide to technology company valuation methods. High-growth SaaS businesses are often valued on revenue multiples because profits may be suppressed by growth spend.

Method one: Comparable company analysis

This is the most common method for SaaS, agencies, and professional services firms in a live fundraising process.

Investors ask: what are similar companies worth right now?

Worked example

Assume your SaaS company has:

- $2,000,000 ARR

- A relevant market multiple of 5.0x revenue

Estimated valuation:

- $2,000,000 × 5.0 = $10,000,000

Now assume your growth is slowing, churn is high, or customer concentration is high. The investor may argue for a lower multiple. If they use 4.0x instead:

- $2,000,000 × 4.0 = $8,000,000

That's a major valuation gap created by operating quality, not just revenue.

Method two: EBITDA multiple

This matters more for agencies, consulting firms, and profitable software companies.

Worked example

Assume your business has:

- $1,000,000 EBITDA

- A multiple range of 4.0x to 10.0x

Valuation range:

- Low end: $1,000,000 × 4.0 = $4,000,000

- High end: $1,000,000 × 10.0 = $10,000,000

If you're a services firm with stable margins and low customer churn, this framework is often more useful than venture-style storytelling. If you're a SaaS company reinvesting heavily, investors may ignore EBITDA and go back to revenue multiples.

Method three: Discounted cash flow

DCF is useful when your future cash flow is predictable enough to forecast with confidence. Many early-stage startups are not there yet. Many $5M to $20M revenue businesses are.

Here's a simplified worked example using real numbers.

Assume projected annual cash flows are:

- Year 1: $300,000

- Year 2: $500,000

- Year 3: $700,000

Assume a discount rate of 10%.

Present value calculation:

| Year | Cash Flow | Discount Factor | Present Value |

|---|---|---|---|

| 1 | $300,000 | 1 / 1.10 | $272,727 |

| 2 | $500,000 | 1 / 1.10² | $413,223 |

| 3 | $700,000 | 1 / 1.10³ | $525,920 |

Estimated value from these three cash flows:

- $272,727 + $413,223 + $525,920 = $1,211,870

This is intentionally simplified. A real DCF would usually include a terminal value, scenario testing, and tighter assumptions. But the lesson is clear. DCF only helps when the forecast is credible.

DCF doesn't reward optimism. It punishes weak assumptions.

Comparison of Startup Valuation Methods

| Method | Best For | Key Pro | Key Con |

|---|---|---|---|

| Comparable company analysis | SaaS and growth-stage tech businesses | Fast, market-aligned, easy to explain | Depends on finding truly comparable companies |

| EBITDA multiple | Profitable tech firms, agencies, service businesses | Anchored in operating earnings | Understates value for companies investing hard in growth |

| Discounted cash flow | Mature businesses with forecast visibility | Ties value to future cash generation | Sensitive to assumptions and easy to challenge |

If you want a broader primer on business financial analysis, that resource is useful for framing how valuation connects to underlying company performance.

My advice as an outsourced CFO

Use comps as your primary fundraising language. Use EBITDA or DCF as support if your business is profitable or highly predictable.

Do not show up with one spreadsheet and one valuation conclusion. Show a range, explain the drivers, and make it obvious that you understand how investors think. That signals maturity fast.

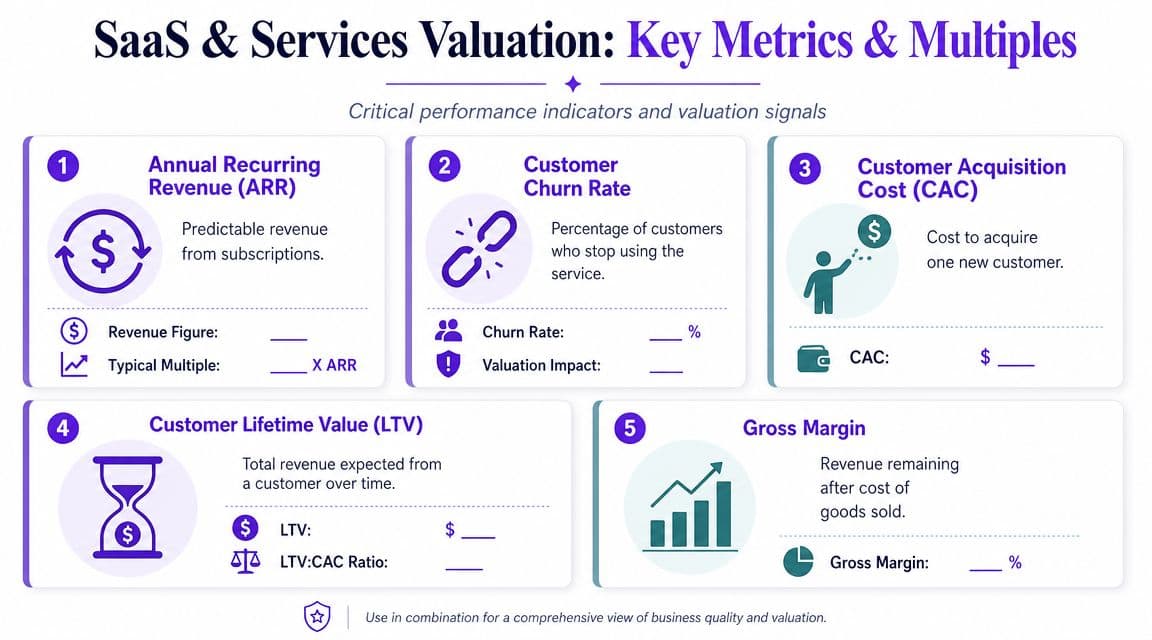

Valuation for SaaS and Service Firms Key Metrics and Multiples

SaaS and services businesses don't get valued for effort. They get valued for quality of revenue.

For IP-heavy businesses, the conversation is also shifting beyond current revenue. A 2024 McKinsey analysis found that generative AI could add $2.6T to $4.4T annually across industries, which is changing how investors view optionality and strategic value, as summarized by MassChallenge's discussion of valuing startups with no revenue. If your company uses AI, proprietary workflows, or unique data assets, you need to prove defensibility, not just mention the technology.

The metrics investors actually care about

Investors usually focus on a handful of drivers when they evaluate startup company valuation for SaaS and recurring-service businesses:

- ARR quality: Not just the number. They want to know contract length, concentration, and expansion behavior.

- Churn: High churn kills valuation because it weakens future cash flow.

- CAC efficiency: If you spend too much to acquire customers, growth becomes expensive.

- LTV: Strong lifetime value supports premium pricing and better payback.

- Gross margin: Higher margin means more room to scale efficiently.

If your team needs a practical framework for maximizing customer lifetime value, that's one of the few operational levers that directly influences how investors interpret retention and payback quality.

A worked SaaS example

Assume your SaaS business has:

- $3,000,000 ARR

- Gross margin of 70%

- Annual logo churn of 8%

- CAC of $12,000

- LTV of $72,000

Your LTV:CAC ratio is:

- $72,000 / $12,000 = 6.0x

That's strong on paper. But if churn worsens and LTV falls to $48,000, then:

- $48,000 / $12,000 = 4.0x

Same sales engine. Lower customer value. Investors will lower your multiple because retention quality dropped.

What this means for service firms

Digital agencies and professional services firms don't usually get pure SaaS-style multiples, but the same logic applies. Investors and buyers reward:

| Metric | Why it matters |

|---|---|

| Recurring retainer revenue | More predictable than project work |

| Client concentration | Heavy dependence on one account increases risk |

| Gross margin by service line | Shows whether revenue is scalable or labor-bound |

| Sales efficiency | Tells buyers whether growth is repeatable |

| Delivery capacity | Signals whether growth will break the team |

Operator note: If your reporting can't separate recurring revenue from one-time revenue, your valuation conversation will get messy fast.

For SaaS companies especially, clean metric definitions matter. If finance and sales disagree on ARR, your investor deck is already compromised. Consequently, disciplined accounting for SaaS becomes part of valuation prep, not back-office cleanup.

Common Valuation Red Flags That Kill Investor Deals

Investors don't walk because your valuation is ambitious. They walk because your valuation is unserious.

For seed and early-stage companies, investors usually triangulate using a market approach and qualitative risk scoring, then test the number against funding needs and target dilution. If your pre-money ask is too high for your stage, you may not be able to raise enough to hit the next milestone. That's a practical issue highlighted in SVB's discussion of determining seed startup valuation.

Red flags investors notice immediately

You picked a number backward

Some founders start with dilution tolerance, then force a valuation that makes the cap table feel better. That's vanity math.

Investors work backward from runway, milestones, and ownership. You should too. If you need more capital than your target dilution allows, your round design is broken.

Your financial model isn't defendable

A model full of smooth growth curves and vague assumptions signals inexperience. Investors will ask where pipeline conversion comes from, why margin expands, and how churn behaves by cohort.

If your answers sound like sales copy, the valuation falls apart.

Revenue quality is unclear

This kills a lot of service and SaaS deals. If you can't cleanly distinguish:

- Recurring vs one-time revenue

- Booked revenue vs recognized revenue

- Contracted revenue vs likely renewals

then investors won't trust your numbers.

That's why revenue policy matters. If your finance function still handles recognition casually, fix that now. Start with a plain-English grasp of ASC 606 revenue recognition before diligence exposes the issue for you.

Founder misconceptions that need to die

| Misconception | Reality |

|---|---|

| “A higher valuation is always better” | Not if it prevents enough capital from being raised |

| “Revenue alone determines price” | Investors care about revenue quality, margin, and risk |

| “A big TAM slide supports a premium valuation” | TAM without proof of execution doesn't close rounds |

| “We'll clean up the model after the term sheet” | Sloppy numbers kill trust before legal docs matter |

Most failed valuation conversations are credibility failures, not math failures.

My blunt recommendation

Before you talk valuation, pressure-test your own story like an investor would. Ask:

- Does this number leave enough runway?

- Can I explain every major assumption in the forecast?

- Do my metrics hold up under diligence?

- Would I invest in this at this price if it were my money?

If the answer to any of those is no, fix the business case before you fix the deck.

Your Investor-Ready Valuation Checklist

A valuation only holds up if you can defend it under diligence. Founders are at a disadvantage when the number in the deck is ahead of the evidence in the data room.

If you want a deal to close, prepare the files investors will ask for before the first meeting. That matters even more when buyers of risk are selective and every assumption gets tested. Your job is to show why this business deserves the range you are asking for, using clean reporting, clear milestones, and metrics that match your model.

What your data room must include

You do not need 200 files. You need the right files, organized well, with numbers that tie out.

- Historical financials: Monthly P&L, balance sheet, and cash flow statement. They should reconcile and match bank activity.

- Forecast model: A driver-based model tied to headcount, pipeline, pricing, delivery capacity, and margin assumptions. If you need a starting point, build a financial forecasting process for startups that investors can test.

- Revenue detail: Customer-level revenue by month, contract terms, renewal dates, churn, expansions, and any non-recurring items flagged clearly.

- Cap table: Fully diluted, current, and consistent with SAFEs, notes, options, and board approvals.

- KPI reporting: SaaS companies should have ARR, MRR, net revenue retention, gross margin, CAC payback, and cohort retention. Service firms should show utilization, gross margin by team or project type, client concentration, and revenue by delivery model.

- Legal and IP records: Formation documents, option grants, assignment agreements, trademarks, patents, and major customer contracts.

- Risk and compliance materials: If security or enterprise diligence will come up, include the status of policies and controls. A practical guide to SOC 2 for startups helps you prepare what investors and larger customers expect to see.

What good preparation looks like

| Area | Investor expectation | Your standard |

|---|---|---|

| Financial statements | Current, accurate, and reconcilable | Monthly close completed on time |

| Forecast | Assumption-driven and testable | Linked to hiring, sales capacity, pricing, and margin |

| SaaS or service KPIs | Consistent definitions over time | One reporting logic across finance, sales, and ops |

| Cap table | Complete and error-free | Updated after every issuance or conversion |

| Valuation case | Supported by evidence | Range backed by metrics, risk, and milestone plan |

The checklist I'd hand a founder before a fundraise

- Reconcile cash, payroll, debt, and revenue accounts

- Clean up the cap table and confirm every security matches legal docs

- Lock KPI definitions so finance, sales, and leadership report the same numbers

- Build a base case, downside case, and use-of-funds model

- Show what drives valuation in your business type

- SaaS: retention, growth efficiency, gross margin, and expansion

- Services: utilization, delivery margin, client concentration, and revenue visibility

- Document churn risk, concentration risk, and any one-time revenue distortions

- Set a valuation range you can defend, then prepare the support for the midpoint

- Assemble every file before outreach starts

One more rule. Do not pitch off a partial data room.

Clean reporting shortens diligence and gives you room to negotiate. Gaps force you into explanations, rework, and price cuts.

If you need outside help assembling this package, Jumpstart Partners provides outsourced controller and bookkeeping support for growing companies and helps produce investor-ready reporting, KPI tracking, and forecast support.

From Valuation to Investment Get Your Financials Right

A strong startup company valuation is the result of disciplined operations. It isn't a clever spreadsheet trick.

If your books are behind, your revenue recognition is inconsistent, or your KPI reporting changes every month, investors will discount your story. They should. A valuation only holds if the business underneath it is measurable, repeatable, and explainable.

What to do next

Your next move should be operational, not cosmetic:

- Tighten monthly reporting: You need fast, accurate closes and decision-ready KPI packs.

- Build a forecast investors can test: Your assumptions should connect to headcount, pipeline, pricing, and retention.

- Fix compliance gaps early: If enterprise buyers or investors care about controls, a practical guide to SOC 2 for startups can help you prepare the right way.

- Model the round before you pitch it: Don't guess at dilution, runway, or milestone timing.

- Create one source of truth: Finance, ops, and go-to-market teams need the same numbers.

Your valuation discussion gets easier when your reporting is already clean. Your fundraising process gets faster when your data room is already built. And your negotiating position gets stronger when you can show exactly how new capital turns into measurable progress.

If you haven't built that system yet, start with a solid process for financial forecasting for startups. That's the bridge between ambition and a valuation investors are prepared to fund.

If you're preparing for a raise and need investor-ready financials, cleaner reporting, or a forecast you can defend in diligence, talk to Jumpstart Partners. They work with growing SaaS, agency, and services businesses to build the financial foundation behind a credible valuation.