Financial Operations

What Is a Tax Levy? a Founder's Guide to Frozen Accounts

What is a tax levy? It's a legal seizure of your business assets by the IRS. Learn the difference between a levy and a lien and the steps to resolve it fast.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··16 min readA tax levy is the legal seizure of your business assets by a tax authority to collect unpaid taxes. A lien is only a claim against property, but a levy is the moment the government reaches into your bank account, wages, or receivables and takes cash.

If you're reading this because payroll failed, your operating account shows a zero balance, or your bank called about a government hold, you're not dealing with a bookkeeping nuisance. You're in a cash crisis. The right response is not panic, and it's not delay. It's fast triage, clean records, and immediate contact with the taxing authority before more cash gets trapped.

For founders, bad habits become expensive. Ignored notices, messy books, late payroll filings, and optimistic cash assumptions all collide at once. You need to know what a tax levy is, what it can hit, and exactly how to stop the damage from spreading.

Your Bank Account Is Frozen Now What

It's Monday morning. You approve payroll in Gusto or your payroll platform, open your bank portal, and the balance you expected to use is unavailable. ACH payments are pending. Vendor debits are about to fail. Your controller thinks it's a fraud flag. It isn't.

It's often a tax levy, which means a tax authority has moved beyond asking for payment and started enforcing collection against your assets. In plain English, they're no longer waiting for you to pay voluntarily.

What this means operationally

The immediate problem isn't the legal definition. The immediate problem is that your company's circulation system just got cut off.

If your main operating account is frozen or drained, three things happen fast:

- Payroll risk spikes: Your team still expects to be paid on time.

- Vendor trust breaks: Failed payments trigger awkward calls and tighter terms.

- Collections get messy: If the levy reaches receivables, customer payments may not land where you expect.

Practical rule: Treat a levy like a liquidity emergency, not a tax paperwork issue.

Your first move

Stop trying to “wait for the bank to sort it out.” Banks don't reverse a levy because you're upset, and they don't negotiate your tax debt for you. Your first job is to confirm exactly what was served, by whom, and which accounts or payment streams are affected.

Pull these items immediately:

| What to confirm | Why it matters |

|---|---|

| Account affected | You need to know whether this is limited or enterprise-wide |

| Taxing authority | IRS, state, or local agencies follow different workflows |

| Date notice was served | Timing determines your next legal and operational step |

| Amount tied to the levy | You need a real cash survival plan for this week |

| Related notices received | Prior letters tell you whether you missed an appeal window |

While you're doing that, tighten up your cash visibility. If your books are behind, your next calls will be weak and unconvincing. Start with a clean transaction review and bank reconciliation process.

If your issue involves creditor access to cash accounts rather than an IRS matter alone, this guide to Utah bank account levies is useful context on how third-party levies work in practice.

The Critical Difference Between a Tax Lien and a Tax Levy

Founders confuse liens and levies all the time. That mistake costs time, and in a levy situation, time is cash.

A tax lien is a claim. A tax levy is enforcement. Under IRS guidance on what a levy is, the IRS may legally seize a taxpayer's property or rights to property to satisfy a tax debt under IRC §6331, including assets held by third parties like wages and bank accounts. That's why a levy is materially more destructive than a lien.

Tax Lien vs. Tax Levy at a Glance

| Attribute | Tax Lien | Tax Levy |

|---|---|---|

| What it is | A claim against your property | An active seizure of property or rights to property |

| Cash flow impact | Indirect and slower | Immediate and direct |

| Effect on bank account | Doesn't itself take cash | Can take cash from the account |

| Effect on receivables | Usually none by itself | Can redirect payments owed to you |

| Urgency level | Serious, but often manageable over time | Emergency |

| What founders often get wrong | They underestimate long-term financing damage | They underestimate same-week operating damage |

Why this distinction matters

A lien damages flexibility. A levy damages survival.

With a lien, you still control daily operations unless the broader credit consequences box you in. With a levy, you can lose access to the exact cash you need to make payroll, pay AWS, cover rent, or clear contractor invoices. That's why founders who say, “We got some IRS notice, but it's probably just a filing issue,” are often the ones scrambling later.

A levy is the point where the tax problem stops being administrative and starts dictating who gets paid this week.

There's another reason to get precise. Outside the IRS context, the word “levy” can mean different things in tax systems. In property tax policy, for example, a levy refers to the amount of tax revenue a government is authorized to collect, not a seizure action. The Lincoln Institute notes in its working paper on levy limits that the first documented state-imposed levy limit was enacted in 1852, and that levy limits restrict the amount of revenue raised or the growth in property-tax revenue.

That matters if you operate internationally or deal with real estate-heavy structures. Some jurisdictions use “levy” in ways that have nothing to do with an IRS bank seizure. If you're comparing cross-border tax concepts, this overview of Israel's betterment levy for investors shows how different the term can be in another context.

How a Tax Levy Destroys Business Operations

A levy doesn't just reduce cash. It breaks the mechanisms that keep a business moving.

The IRS states that a levy can take money from bank accounts and seize and sell vehicles, real estate, and other property. It can also hit the cash streams your business relies on to stay alive. The practical effect is simple. Your company can have profitable work, signed contracts, and customers who intend to pay, yet still fail because cash stops moving. That's laid out in IRS guidance on levy actions.

The three pressure points

A levy usually shows up in one of these operational choke points.

Bank levy

This is the one founders feel first. Cash in the operating account becomes unavailable. Payroll batches fail. Auto-debits bounce. Software subscriptions, ad spend, and rent payments get rejected.

Worked example:

You run a SaaS business with $2,000,000 in annual recurring revenue. That works out to roughly $166,667 per month in recurring revenue and about $38,462 per week before any upsells, services revenue, or timing differences.

Now assume your cash plan for this week looked like this:

| Weekly cash item | Amount |

|---|---|

| Beginning available cash | $80,000 |

| Payroll | $32,000 |

| Core software and infrastructure | $8,000 |

| Vendor payments | $15,000 |

| Rent and fixed overhead | $5,000 |

| Expected customer collections this week | $20,000 |

Without a levy, you stay functional. Starting cash plus expected collections gives you $100,000 to work with against $60,000 of outflows, leaving $40,000 in cushion.

Now assume a $50,000 bank levy hits before payroll clears.

Your usable cash falls from $80,000 to $30,000. Add $20,000 in expected collections and you have $50,000 available against $60,000 of near-term obligations. You're short $10,000 before any surprise expense, failed customer payment, or bank delay.

That is how an apparently “contained” tax issue turns into a payroll problem in a single day.

Wage levy

If the levy reaches wages, the damage shifts from company treasury to people. Founders often focus on the corporate tax problem and forget the emotional fallout when employee pay gets touched or payroll administration gets disrupted.

Even when the business itself isn't fully frozen, finance and HR teams suddenly become compliance operators. They field employee questions, handle garnishment processes, and absorb the morale damage.

Accounts receivable levy

This is the most misunderstood version, and for service firms it can be vicious.

If your clients owe you money and a levy reaches those receivables, the paying party may be told to send funds elsewhere. The invoice still reflects your revenue, but the cash never lands in your account. For an agency or professional services firm that lives on regular collections, that can shut down working capital fast.

If your business depends on a tight cash conversion cycle, a levy on receivables is an attack on timing, not just balance.

For founders who need to rebuild visibility after this kind of disruption, a disciplined small-business cash flow management process is essential. You can't negotiate well if you don't know exactly what cash is in, what's delayed, and what must be paid first.

The hidden damage founders miss

The seized amount is only part of the cost. The second-order damage usually hurts more:

- Failed payroll creates trust problems with employees.

- Rejected vendor payments trigger holds on software, media spend, or contract labor.

- Customers get confused if remittance instructions change or payments are intercepted.

- Leadership gets distracted from sales, delivery, and fundraising.

That's why “what is a tax levy” isn't really a dictionary question for a founder. It's a business continuity question.

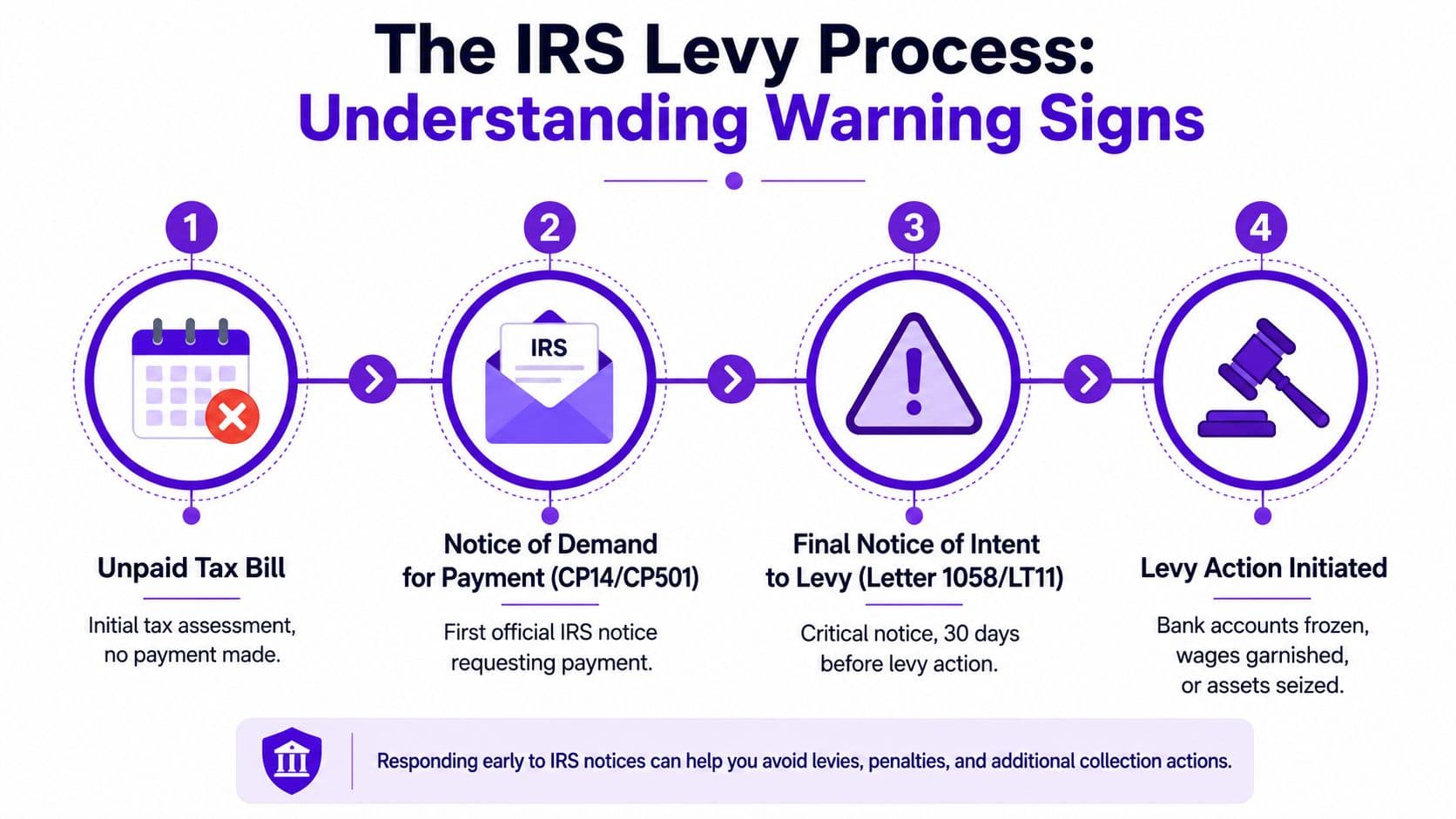

The IRS Levy Process and Warning Signs

A levy doesn't arrive out of nowhere. The IRS follows a sequence before it enforces collection. H&R Block's summary of the process explains that a levy occurs only after a tax assessment, a Notice and Demand for Payment, and a Final Notice of Intent to Levy that includes your right to a Collection Due Process hearing. It also notes that acting within the 30-day window can halt further levy action while the case is pending, which is why this IRS levy process overview matters.

The timeline that matters

Here's the practical sequence founders should watch for:

| Stage | What it means | What you should do |

|---|---|---|

| Tax assessment | The IRS says tax is due | Verify the liability and supporting filings |

| Notice and Demand for Payment | The IRS requests payment | Don't ignore it. Reconcile books and respond |

| Final Notice of Intent to Levy | Enforcement is approaching | Act inside the 30-day window |

| Levy action | Cash or property can be taken | Shift to damage control and immediate resolution |

The notice you can't ignore

The most important warning sign is the Final Notice of Intent to Levy. That's not routine mail. That's the last meaningful off-ramp before enforcement escalates.

If that notice is in your inbox, mail stack, or scanned documents folder right now, stop telling yourself you'll “deal with it after month-end.” You won't have a calm month-end if your cash gets trapped first.

Decision point: Once the final notice arrives, your response speed matters more than your explanation.

Red flags founders miss

Most levy situations aren't caused by one giant event. They build through a string of avoidable misses.

- Old notices went unopened: The mail looked boring, so nobody escalated it.

- Books weren't current: You couldn't tell whether the tax balance was real, duplicate, or already paid.

- Payroll tax deposits slipped: Founders treated trust-fund taxes like a temporary working capital source.

- You assumed it was a scam: Some notices are scams. Many are not. Verify first, dismiss later.

- No one owned compliance: The founder thought the bookkeeper had it. The bookkeeper thought the payroll company had it.

Good records matter here. If you can't produce returns, payment history, and supporting books quickly, your position weakens. This is exactly why consistent document retention matters, and this guide on how long to keep business records is worth applying before a crisis hits.

If you also operate in Australia or compare director liability frameworks across jurisdictions, this explanation on safeguarding assets from ATO is a useful example of how tax enforcement can escalate when directors wait too long.

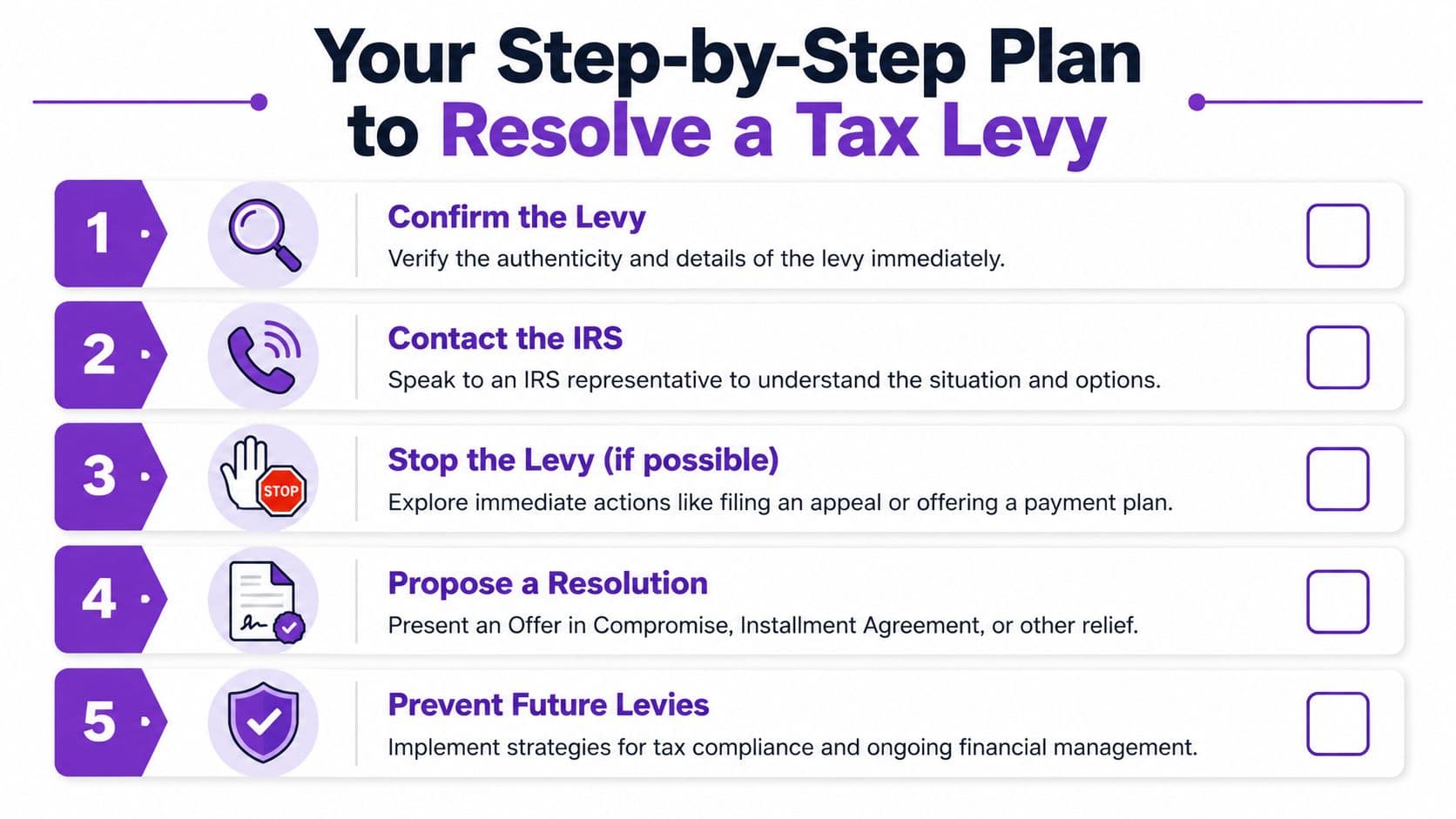

Your Step-by-Step Plan to Resolve a Tax Levy

You don't solve a levy with outrage. You solve it with sequence.

The core objective is straightforward. Confirm the facts, stop further enforcement if possible, present a credible resolution path, and keep the business alive while you do it.

Step 1. Confirm the levy and isolate the damage

Get the notice, bank communication, and account detail in one place. You need to know whether the levy is already active, whether it targets one account or multiple streams, and whether this is an IRS matter or another taxing authority.

Build a same-day list:

- Affected accounts: Operating, payroll, reserve, merchant, and savings accounts

- Affected cash inflows: Client payments, processor deposits, recurring ACH collections

- Critical obligations this week: Payroll, rent, software, debt service, tax deposits

- Decision owners: Founder, controller, CPA, tax resolution counsel if needed

If your books are messy, clean that up immediately. A fast QuickBooks cleanup service or equivalent internal cleanup effort can materially improve your ability to present facts instead of guesses.

Step 2. Contact the IRS and stop being passive

Call. Don't wait for a better mood, a perfect spreadsheet, or your next board meeting.

You need to understand what period is at issue, what notices were sent, whether there's an active appeal window, and what the IRS will require to consider release or a collection alternative.

"The single biggest mistake founders make when facing a tax issue is silence. The IRS is far more willing to negotiate with taxpayers who are communicative and have a clear financial picture than with those who ignore notices. A credible set of books and a proactive plan are your most powerful tools for resolution." - [Insert Expert Name, Title, Company]

That quote is exactly right. Silence makes you look disorganized or evasive. Neither helps.

A short explainer can help your team get oriented before the deeper work starts:

Step 3. Prepare the financial package before you negotiate

The IRS doesn't care that your business is “usually fine.” It cares whether your records show current ability to pay, hardship, and compliance going forward.

Gather these documents:

| Document | Why you need it |

|---|---|

| Filed tax returns | Confirms filing status and periods at issue |

| Profit and loss statement | Shows operating performance |

| Balance sheet | Shows available assets and liabilities |

| Bank statements | Proves current liquidity |

| Payroll reports | Critical if payroll taxes are involved |

| Accounts receivable aging | Shows expected incoming cash |

| Accounts payable aging | Shows immediate obligations |

Step 4. Pick the right path, not the most emotionally satisfying one

Founders often want to “fight the whole thing” before they understand it. That's not always the best move.

Your realistic options usually fall into these buckets:

Pay in full

If the amount is manageable and the business can survive it, this is the fastest path. It's painful, but clean. Don't starve the company to make a heroic gesture, though. Preserve operating continuity first.

Request a hearing or appeal

If you're still within the response window tied to the final notice, this can stop enforcement while the matter is pending. Use it when timing is still on your side and there's a legitimate issue to review.

Installment agreement

This is often the practical answer for operating businesses with healthy revenue but strained liquidity. If the IRS sees a business that can pay over time and stay current, structured payments are far better than continued enforcement.

Offer in compromise

This is more specialized. It makes sense when the business has a proven inability to pay the full amount and the facts support a reduced settlement. Don't default to this just because you'd prefer to pay less.

Step 5. Protect operations while resolution is in motion

Negotiating the tax issue isn't enough. You also need a short-term cash protection plan.

Use a triage list:

- Payroll first: Know the exact payroll date, amount, and account path.

- Revenue collection second: Confirm where customer cash is landing.

- Critical vendors third: Prioritize systems that keep delivery and billing running.

- Everything else after that: Defer nonessential spend immediately.

Keep the business breathing while the tax problem gets solved. A perfect legal strategy is useless if payroll collapses first.

Preventing Tax Levies with Proactive Financial Management

The cheapest levy is the one you never face.

Most founders don't get hit because they're reckless. They get hit because finance stayed too informal for too long. Returns were filed late. Payroll tax obligations blended into general cash management. Reconciliations lagged. Nobody had a clean weekly picture of tax exposure versus available cash.

What prevention actually looks like

Prevention is boring. That's why it works.

- Close your books on time: If your bank accounts, payroll liabilities, and tax balances aren't current, you'll miss problems while they're still fixable.

- Separate tax cash mentally and operationally: Don't treat payroll taxes like a short-term loan from the government.

- Forecast cash weekly: A rolling forecast exposes tax pressure before it becomes an enforcement problem. This guide to cash flow forecasting best practices is a good place to tighten that discipline.

- Escalate notices fast: Mail from tax authorities should never sit in a founder's glove compartment or a generic inbox.

When DIY finance stops being enough

If your business is growing and the accounting function still depends on a founder, an office manager, or a part-time bookkeeper stitching together QuickBooks and spreadsheets, you have a control problem. That may feel efficient until a notice gets missed or a liability account is wrong for months.

Mature finance operations earn their keep not by making prettier reports, but by reducing the odds that a tax issue turns into a frozen-account emergency.

If you want help building that kind of visibility and control, Jumpstart Partners works with growing businesses that need stronger bookkeeping, controller support, and cash flow discipline before problems become crises.