Financial Operations

What is S G and A? Founder's Guide to Operating Expenses

Confused by what is S G and A on your P&L? Learn its components, SaaS benchmarks, & how to cut costs without slowing growth.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··19 min readIf you think SG&A is just a boring expense line on your P&L, you're leaving money, margin, and valuation on the table.

For founders in the $500K to $20M revenue range, SG&A isn't accounting trivia. It's one of the clearest signals of whether your business can scale cleanly, close books fast, survive diligence, and turn growth into operating profit. If you're asking what is s g and a, the right answer isn't just a definition. It's this: SG&A is the key operational factor that shows whether your company is disciplined or sloppy.

Your Biggest Untracked Risk SG&A

Most founders watch revenue, runway, and headcount. They don't watch SG&A with the same intensity. That's a mistake.

According to Kruze Consulting's SG&A analysis, 98% of SaaS founders report SG&A as a top boardroom concern. The same analysis notes that early-stage SaaS companies often run at 40-60% SG&A as a percentage of revenue, while top-quartile firms sit at 25-35%. That gap is massive. It tells investors whether your cost structure is getting stronger as you scale, or whether every new dollar of revenue comes with too much overhead.

Why investors care more than founders think

A high SG&A ratio doesn't just reduce profit. It changes the story investors tell themselves about your business.

If your SG&A is bloated, they see weak operational efficiency. They assume your back office is messy, your sales efficiency is unclear, and your margin story won't improve without a painful reset. That's why smart founders treat SG&A as a strategic metric, not a bookkeeping category.

The common blind spot

Most content on what is s g and a stops at definitions. That doesn't help you run the company.

What matters is whether your SG&A supports growth or drags it down. Founders usually discover the problem too late, during a fundraise, an audit, or a cash squeeze. By then, you're defending numbers instead of controlling them.

A lot of leakage hides in software sprawl, manual approvals, duplicated vendors, and unmanaged small purchases. If you haven't reviewed your long tail of subscriptions and one-off spend, this guide on tail spend management is worth your time.

Practical rule: If you can't explain your SG&A line by owner, function, and return, you don't control it.

You also need a clean expense tracking process before you can optimize anything. Start with a simple operating discipline like the one outlined in this guide on how to track business expenses.

Decoding SG&A What It Is and What It Includes

SG&A means Selling, General, and Administrative expenses. These are the operating costs of winning customers and running the company after the product or service is delivered. They sit below gross profit on the income statement, and they shape operating margin, cash burn, and how credible your scale story looks in diligence.

For scaling companies, SG&A is not just an accounting label. It is an operating lever. If you manage it well, you get better margins without stalling growth. If you let it drift, revenue grows while efficiency gets worse.

The three buckets

Use this framework to clean up your chart of accounts and assign clear owners to spend.

| Category | What it covers | SaaS examples | Agency or services examples |

|---|---|---|---|

| Selling | Costs tied to generating revenue | sales salaries, commissions, paid acquisition, CRM tools | business development salaries, proposal software, referral fees, paid lead gen |

| General | Shared overhead required to keep the business running | rent, insurance, software subscriptions, office operations | office expense, shared software, admin overhead |

| Administrative | Leadership and support functions | HR, finance, legal, IT, executive salaries | payroll admin, bookkeeping, legal, founder support staff |

That breakdown matters because each bucket behaves differently as you scale. Selling spend should produce pipeline and revenue. General spend should stay controlled as a percentage of revenue. Administrative spend should add control, speed, and reporting quality, not bureaucracy.

Selling expenses

Selling expense covers the cost of acquiring customers.

In SaaS, this usually includes account executives, SDRs, commissions, ad spend, CRM systems, sales engagement tools, events, and the sales operations support tied to revenue generation. In a professional services firm, it includes business development payroll, proposal costs, referral fees, and marketing programs that create qualified pipeline.

This line deserves aggressive scrutiny because it directly affects payback, burn, and valuation. If sales spend rises faster than pipeline quality or closed revenue, your SG&A is buying activity instead of growth.

General expenses

General expenses are the shared costs of operating the business.

This bucket includes rent, utilities, insurance, basic software, and other overhead that supports the whole company. These costs rarely spike all at once. They creep. A few extra tools, overlapping vendors, and no approval discipline can add thousands per month without improving delivery or sales output.

SaaS companies often lose money here through software sprawl. Professional services firms lose it through fragmented ops processes and unused subscriptions spread across teams.

Administrative expenses

Administrative expense is your support infrastructure.

It includes finance, accounting, HR, legal, IT support, payroll processing, executive salaries, and back-office staff. Strong admin spend improves reporting speed, compliance, collections, and decision-making. Weak admin spend creates rework, slow closes, bad data, and founder bottlenecks. In such cases, outsourced finance gives scaling firms an edge. A full-time controller or finance lead can be expensive before the business needs one full-time. An outsourced controller or CFO setup gives you tighter reporting, approval controls, cleaner accruals, and better board-ready numbers at a lower fixed cost.

SG&A should have an owner, a purpose, and a measurable return. If it has none of the three, cut it or redesign it.

A simple worked example

Say your company has these monthly operating costs:

- Selling: $30,000 in sales payroll and commissions

- General: $12,000 in rent, insurance, and software

- Administrative: $18,000 in HR, finance, legal, and executive support

Your monthly SG&A is $60,000.

If monthly revenue is $150,000, SG&A is 40% of revenue.

That 40% is not just a bookkeeping output. It is a management signal. If you are a SaaS company with strong gross margins, you now need to know whether that spend is accelerating ARR efficiently or covering weak process discipline. If you run a professional services firm, you need to know whether admin and overhead are absorbing margin that should be dropping to EBITDA.

If your P&L does not break these categories out cleanly, fix the reporting first. Start with a tighter profit and loss management process so you can see which SG&A dollars are producing growth and which ones are dragging down profitability.

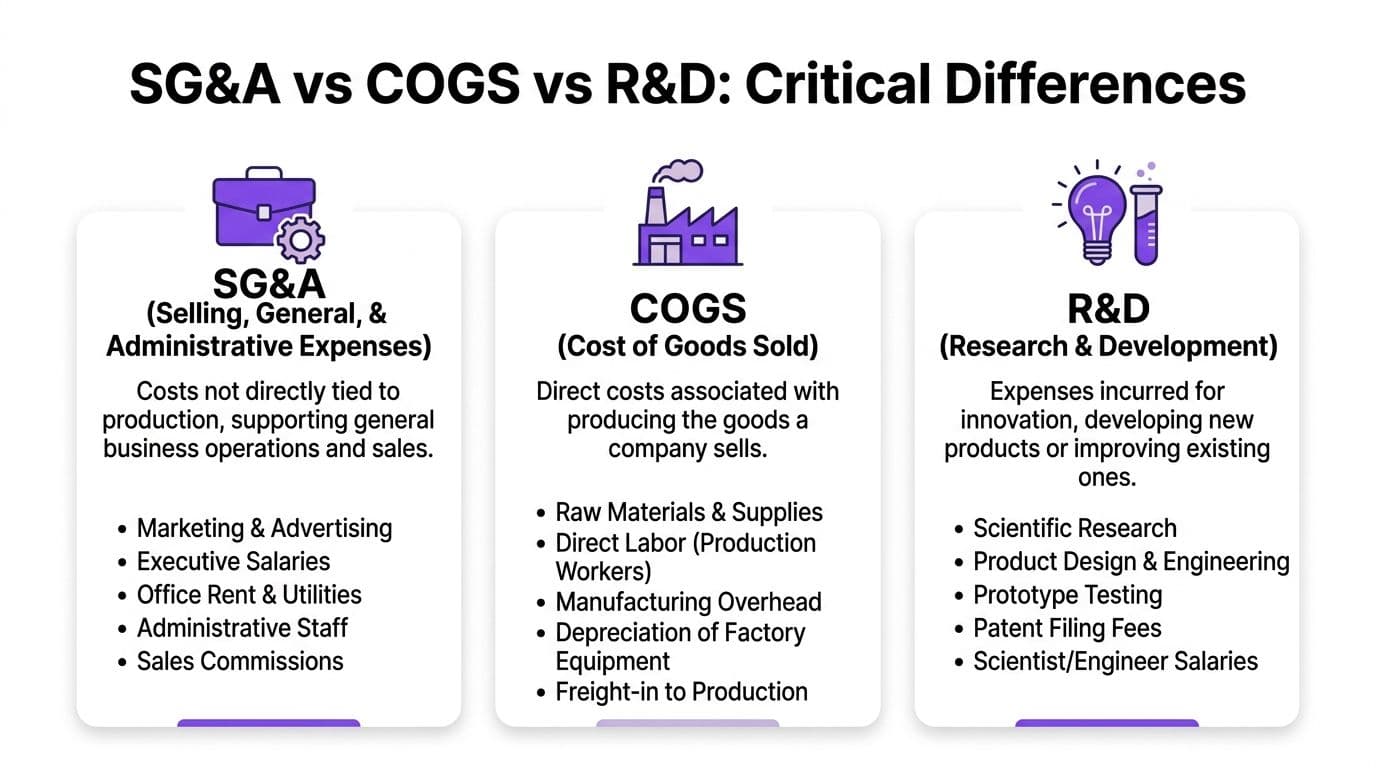

SG&A vs COGS vs R&D The Critical Differences

Founders get into trouble when they blur these categories.

Misclassification doesn't just create ugly books. It distorts gross margin, operating income, and the credibility of your reporting. During diligence, investors and lenders look for exactly this kind of sloppiness.

The bright-line difference

Here's the clean way to think about it.

| Expense type | Core question | Typical examples |

|---|---|---|

| COGS | Does this cost directly deliver the product or service you sold? | hosting tied to product delivery, delivery labor, project delivery staff |

| SG&A | Does this cost support selling or running the company? | sales payroll, admin salaries, rent, HR, legal |

| R&D | Does this cost fund innovation or product development work? | product development salaries, prototype work, testing for new features |

For SaaS, server hosting that supports the live product is generally part of delivery economics, not SG&A. Sales salaries are SG&A. Product development work belongs in R&D, not in selling and admin.

For an agency, client delivery labor belongs with delivery costs. Your office manager does not. A strategist working on a paid client engagement is different from a business development lead writing pitches.

Why this matters to gross margin

Verified guidance in the SG&A benchmark summary notes that misclassifying SG&A, such as putting R&D into COGS, inflates or distorts margin presentation and undermines EBIT accuracy. That's not a technical footnote. That's a diligence problem.

Here's a worked example using simple numbers.

Assume your annual revenue is $1,000,000.

Scenario A. Correct classification:

- Revenue: $1,000,000

- COGS: $300,000

- Gross profit: $700,000

- SG&A: $250,000

- R&D: $100,000

Gross margin is:

$700,000 / $1,000,000 = 70%

Now move a $100,000 expense from SG&A into COGS.

Scenario B. Misclassified expense:

- Revenue: $1,000,000

- COGS: $400,000

- Gross profit: $600,000

- SG&A: $150,000

- R&D: $100,000

Gross margin becomes:

$600,000 / $1,000,000 = 60%

You didn't change the business. You changed the presentation. But that presentation changes how investors judge your unit economics.

Common founder mistakes

- Putting delivery labor into SG&A: That makes gross margin look better than reality.

- Putting founder salary entirely into COGS: That's often wrong if the founder is acting as an executive, not delivering work.

- Shoving product build costs into SG&A: That hides R&D and confuses your product investment story.

- Treating all software as overhead: Some tools support delivery, some support sales, some support administration.

Clean classification is one of the fastest ways to make your financials more credible without changing a single dollar of spend.

If your business has any mix of service delivery, inventory, or production-style workflows, this article on accounting for manufacturing is useful for understanding how cost classification logic works in practice.

A founder test

Ask one question for every expense: Would this cost still exist if I stopped selling and delivering this specific product or service today?

- If the answer is tied directly to delivery, it's closer to COGS.

- If the answer is tied to company operations or selling, it's SG&A.

- If the answer is about building or improving future product capability, it's R&D.

This isn't optional. If your categories are wrong, every management discussion built on those numbers gets weaker.

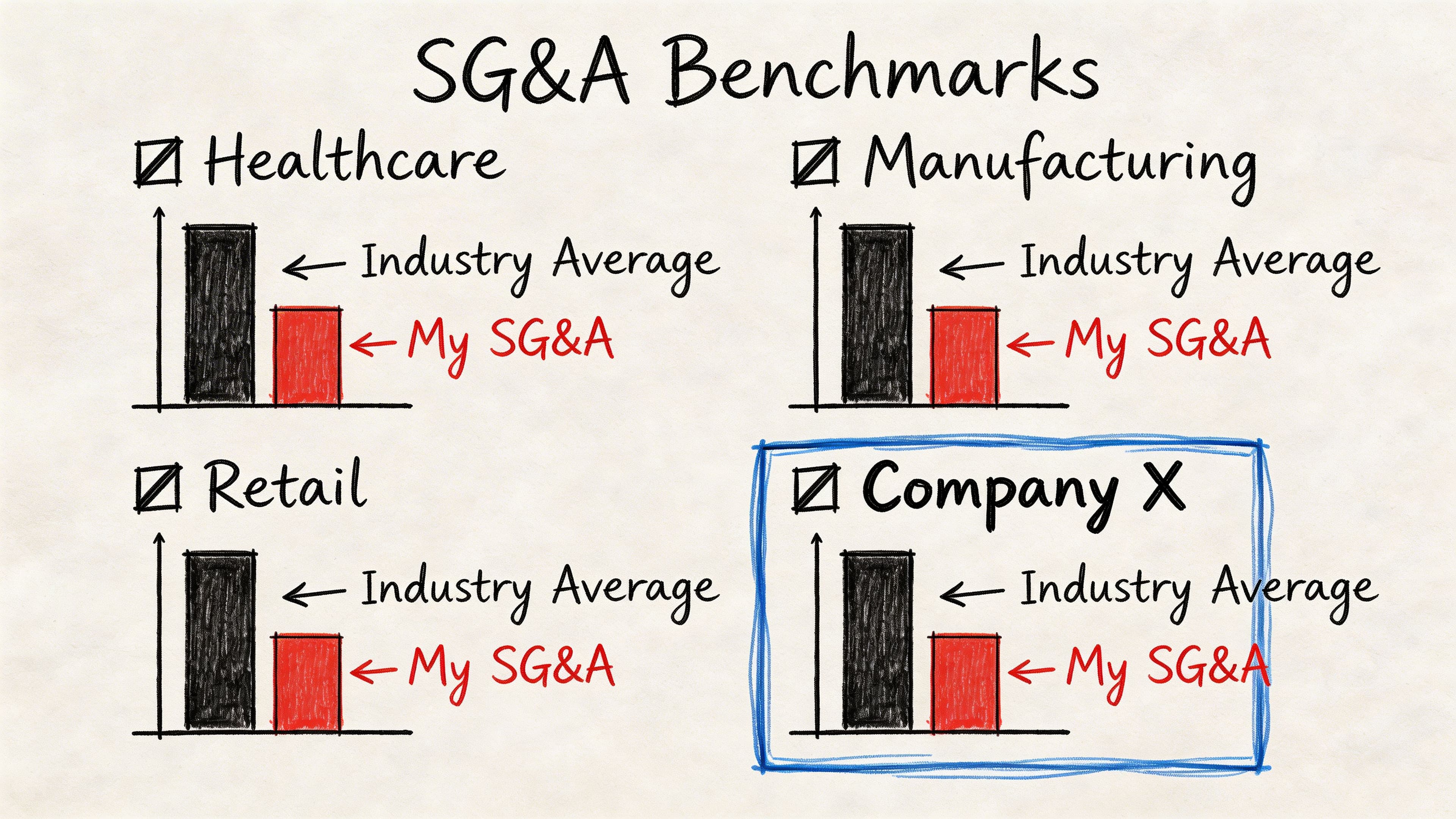

SG&A Benchmarks and Industry Examples

Benchmarks matter because they tell you whether your SG&A is aggressive, healthy, or bloated for your stage.

According to AccountingCoach's discussion of SG&A and benchmark ranges, startups often run at 40-60% SG&A as a percentage of revenue before profitability. The same verified benchmark summary notes that the ratio can drop to 25% after optimization, and that Wall Street Prep models SG&A declining with scale from 35% at $5M ARR to 20% at $20M. It also notes that ratios above 30% of revenue correlate with 15-20% lower valuations in fundraising.

A simple benchmark table

| Company stage | Revenue | SG&A | SG&A as % of revenue | Read on the number |

|---|---|---|---|---|

| Early-stage SaaS | $500,000 | $250,000 | 50% | common in early stage, but needs a path down |

| Growth SaaS | $5,000,000 | $2,000,000 | 40% | above the modeled 35% level for this scale |

| Scaled SaaS | $20,000,000 | $4,000,000 | 20% | aligned with stronger operational efficiency |

Worked example at $5M ARR

Take a SaaS company with $5,000,000 in ARR and $2,000,000 in SG&A.

The formula is straightforward:

$2,000,000 / $5,000,000 = 40%

At that size, 40% is not a flattering number if you're pitching operational efficiency. The benchmark summary tied to AccountingCoach says modeled SG&A trends down to 35% at $5M ARR, and stronger operators get lower as they scale. That means this company needs a clear explanation.

Maybe sales and marketing is still intentionally heavy because CAC payback is strong. Maybe the admin layer is carrying duplicate systems and unnecessary management cost. The number itself doesn't convict you. But it absolutely invites scrutiny.

What investors hear when they see the ratio

Founders tend to explain SG&A as a temporary growth investment. Investors want evidence that the investment improves efficiency.

If your ratio is above 30%, the verified benchmark summary says it correlates with 15-20% lower valuations in fundraising. That's not because investors hate spending. It's because they want proof that spending becomes more efficient as revenue grows.

A high SG&A ratio without a clear operating plan reads like overhead. A high ratio with clean reporting, category ownership, and a declining trend reads like strategy.

What to do with the benchmark

Use benchmark ranges as a diagnostic tool, not a vanity metric.

- If you're early and high: show the path from customer acquisition spend to operating efficiency.

- If you're mid-scale and stuck: audit general and administrative layers first. They usually hide the easiest wins.

- If you're lower than peers: make sure you aren't underinvesting in sales capacity or compliance infrastructure.

Also pay attention to process efficiency. The verified benchmark summary notes that automation can reduce AP and AR cycle times by 50%, improve DSO by 15 days, and create 5-7% SG&A savings when payroll and HR systems such as Gusto and BambooHR are integrated properly.

Red Flags How Bloated SG&A Kills Profitability

Bloated SG&A rarely shows up as one giant obvious mistake. It shows up as friction.

Your close takes too long. Your software stack keeps expanding. Sales spend rises faster than pipeline quality. Nobody can explain which administrative costs are necessary and which ones are leftovers from decisions you made six months ago.

The symptom checker

If several of these are true, your SG&A probably needs attention.

- Your books lag reality: You close late, then make decisions off stale numbers.

- Your tools overlap: You pay for multiple systems that handle approvals, reporting, CRM, payroll, or expense management in slightly different ways.

- Your admin headcount grows before controls improve: More people are patching process gaps instead of fixing them.

- Your leaders own budget, but not outcomes: Spend gets approved without a hard link to margin, efficiency, or customer acquisition performance.

- Your founder still approves everything: That creates bottlenecks and usually hides the fact that no durable process exists.

The hidden cost of manual finance

Manual SG&A isn't just inefficient. It weakens operating discipline.

When AP, reconciliations, payroll reviews, and revenue workflows live in spreadsheets and inboxes, finance spends time chasing transactions instead of analyzing them. You end up with reporting that explains the past poorly and does nothing to improve the future.

Why this gets expensive fast

Excess SG&A lowers operating income directly. It also drains management attention.

A founder who spends hours resolving invoice disputes, cleaning up payroll classifications, or reviewing overlapping software contracts is doing administrative work instead of driving revenue, retention, and delivery quality. That tradeoff doesn't show up neatly in a ledger, but it absolutely hits profitability.

If your team can't tell the difference between necessary support cost and avoidable overhead, SG&A will keep growing faster than discipline.

Common misconceptions

| Misconception | Reality |

|---|---|

| "We'll clean this up after the raise." | Investors often spot SG&A issues before you get the raise. |

| "More overhead means we're maturing." | Mature companies build systems, not just layers of cost. |

| "It's only a few subscriptions." | Small recurring charges and fragmented workflows stack into real margin loss. |

| "Our controller can fix it later." | Cleanup gets harder after misclassification and process debt pile up. |

The founders who manage SG&A well don't obsess over every dollar. They insist that every recurring dollar has an owner, a purpose, and a place in the reporting structure.

How to Actively Manage and Reduce Your SG&A Costs

Companies rarely get into trouble because one expense is too high. They get into trouble because no one is actively managing the overhead layer as revenue scales.

SG&A is an operating lever. Treat it that way. For SaaS and professional services firms, the goal is simple: keep support costs from growing faster than gross profit. If you do that well, you improve EBITDA, extend runway, and walk into fundraising with a cleaner story.

Start where cost grows faster than discipline

Founders often attack SG&A in the wrong order. They question headcount before fixing workflows. That is backwards.

Start with the costs that scale badly when process is weak:

- Administrative workflow drag Clean up AP approvals, expense coding, payroll sync, collections follow-up, and reconciliations. These costs multiply because they live across departments, systems, and inboxes.

- Tool and vendor sprawl Cut duplicate software, overlapping agencies, unused seats, and month-to-month services no one owns. In SaaS companies, this usually sits inside finance, sales ops, marketing ops, and customer success. In professional services firms, it usually shows up in staffing tools, project systems, payroll add-ons, and subcontractor admin.

- Selling expense efficiency Review sales and marketing spend only after you have clean attribution and payback visibility. Cutting demand generation blindly can hurt growth. Cutting waste in process and management layers improves margin without slowing pipeline.

Use a simple operating test

Every SG&A line should answer three questions:

- Who owns it?

- What business outcome does it support?

- Does it scale efficiently with revenue?

If you cannot answer all three within a few minutes, that cost is already a candidate for review.

A worked example with real numbers

Assume your company carries $2,000,000 in annual SG&A.

A focused 10% reduction produces:

$2,000,000 × 10% = $200,000

That is not a bookkeeping win. That is capital.

For a SaaS company, $200,000 can cover a senior AE, customer success capacity, or product work tied directly to retention. For a professional services firm, it can fund delivery hires, improve utilization, or protect cash during slow collections periods.

Now isolate just the administrative layer. If $300,000 of SG&A sits in finance and back-office overhead, and process improvements cut that by 20% to 30%, the savings are:

- $300,000 × 20% = $60,000

- $300,000 × 30% = $90,000

That is often enough to pay for better systems and outsourced finance support while still producing a strong net gain.

What to implement in the next 90 days

| Priority | Action | Why it matters |

|---|---|---|

| Immediate | assign an owner to every recurring SG&A line | spend without ownership keeps renewing and keeps growing |

| Immediate | split the P&L into selling, general, and administrative categories | blended overhead hides the actual problem areas |

| Near term | connect your accounting system and billing stack | cleaner revenue, collections, and reconciliation workflows reduce finance drag |

| Near term | connect payroll and HR systems | fewer manual entries, better classifications, and less month-end cleanup |

| Near term | require zero-based review for overhead categories | recurring cost should be re-earned, not inherited |

| Ongoing | run monthly budget-to-actual reviews by category owner | variance review catches bloat before it becomes permanent |

If your AP process still runs through email approvals, PDFs, and manual entry, start with Accounts Payable Automation Best Practices.

Build a management cadence, not a one-time cleanup

A budget alone will not control SG&A. Operating cadence will.

Review SG&A monthly by owner, by department, and as a percentage of revenue. For SaaS, compare spend against ARR growth, net retention, and sales efficiency. For professional services, compare it against utilization, gross margin by service line, and cash conversion speed. That is how you decide whether overhead is supporting scale or choking it.

You also need faster reporting. If month-end close takes too long, the numbers become history instead of management tools. An outsourced controller or CFO partner can fix that by tightening classifications, shortening close, and giving founders a usable view of where margin is slipping.

For a broader framework on connecting overhead control to earnings, read this guide on how to improve profit margins.

This short video gives a practical lens on tightening spend without choking growth.

As noted earlier, SG&A misclassification distorts operating performance. If selling expense, admin overhead, COGS, and R&D are not mapped correctly, your margins look better or worse than they really are. That leads to bad hiring decisions, bad pricing decisions, and messy diligence when investors start asking questions.

Optimize Your SG&A with an Outsourced Controller

If your SG&A is unclear, your decision-making is slower than it should be.

An outsourced controller brings order to the exact areas where founders usually struggle. Expense classification. Close process. reconciliations. Payroll mapping. Revenue recognition workflows. Budget-to-actual review. The goal isn't prettier reports. The goal is better operating control.

What good controller support changes

A strong outsourced controller helps you:

- Clean up classification: so SG&A, COGS, and R&D tell the truth

- Shorten the close: so you can act on current numbers

- Build investor-ready reporting: so diligence doesn't become a cleanup project

- Integrate the stack: so QuickBooks, Xero, Stripe, Gusto, and other systems feed clean data instead of manual work

- Track leakage: so you can see where administrative drag is hurting margin and cash flow

Why this matters at your stage

At $500K to $20M in revenue, most companies aren't big enough for a fully built finance department. But they're too complex for DIY bookkeeping and reactive cleanup.

That's the gap an outsourced controller fills. You get financial discipline without adding unnecessary fixed overhead. More important, you get someone whose job is to make SG&A visible, explainable, and controllable.

Founders don't need more accounting activity. They need tighter numbers, faster closes, and a finance partner who can tell them where margin is leaking.

If you're evaluating that route, review what outsourced controller services should include before you hire.

SG&A is one of the clearest operational tools in your business. Treat it that way. Define it correctly. Benchmark it accurately. Fix the leaks. Then use the savings to improve profit, cash flow, and fundraising credibility.

If you want a clear read on your SG&A, Jumpstart Partners helps founders and finance leaders clean up classifications, tighten month-end close, and build investor-ready reporting that demonstrates true operational efficiency. If your numbers are slow, messy, or hard to defend, book a consultation and get a practical assessment of where SG&A is helping your growth and where it's dragging it down.